In this time of uncertainty, we can only search for insights as we await actual Q2 figures and see how businesses fare as lock-downs are slowly relaxed. Many businesses, particularly SMEs, may hobble on for a while as demand slowly picks up and governmental support becomes due for withdrawal. Some, like hairdressers, will re-establish their businesses due to the nature of their service or product and with the support of a loyal customer base. Some may even thrive as their businesses adapt to the new normal. Many may not. Services dependent upon crowds such as the leisure and hospitality sectors look particularly exposed. The digital transformation of many businesses will take a leap forward and the creative destruction of capitalism will take its course. Many of the old ways of doing businesses will be consigned to history in one fell swoop.

The FED this week issued their financial stability report with the following view on the current level of vulnerabilities:

1) Asset valuations. Asset prices remain vulnerable to significant price declines should the pandemic take an unexpected course, the economic fallout prove more adverse or financial system strains re-emerge.

2) Borrowing by businesses and households. Debt owed by businesses had been historically high relative to gross domestic product (GDP) through the beginning of 2020, with the most rapid increases concentrated among the riskiest firms amid weak credit standards. The general decline in revenues associated with the severe reduction in economic activity has weakened the ability of businesses to repay these (and other) obligations. While household debt was at a moderate level relative to income before the shock, a deterioration in the ability of some households to repay obligations may result in material losses to lenders.

3) Leverage in the financial sector. Before the pandemic, the largest U.S. banks were strongly capitalized, and leverage at broker-dealers was low; by contrast, measures of leverage at life insurance companies and hedge funds were at the higher ends of their ranges over the past decade. To date, banks have been able to meet surging demand for draws on credit lines while also building loan loss reserves to absorb higher expected defaults. Broker dealers struggled to provide intermediation services during the acute period of financial stress. At least some hedge funds appear to have been severely affected by the large asset price declines and increased volatility in February and March, reportedly contributing to market dislocations. All told, the prospect for losses at financial institutions to create pressures over the medium term appears elevated.

4) Funding risk. In the face of the COVID-19 outbreak and associated financial market turmoil, funding markets proved less fragile than during the 2007–09 financial crisis. Nonetheless, significant strains emerged, and emergency Federal Reserve actions were required to stabilize short-term funding markets.

The point about household debt is an important one and points to the likelihood that this will be a recession with characteristics more akin to those before the 2008 financial crisis, as per the graph below.

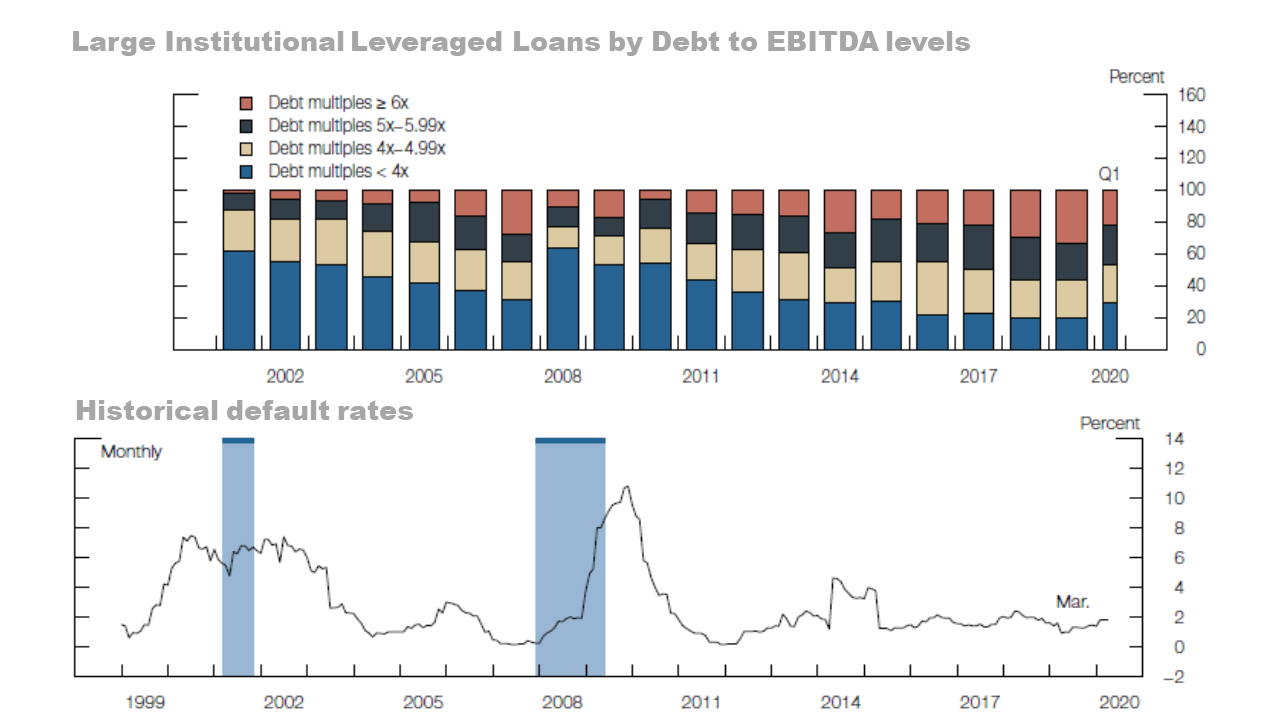

The oft highlighted concerns about leveraged loans in recent times has again been highlighted by the Fed as a worry in this crisis, as below, with default rates likely to turn sharply upwards.

However, it was the commentary in the report from the Fed’s market outreach that I thought captured succinctly the current market fears for the future:

Many contacts expressed concern that a U.S. recession brought about by the pandemic could expose highly leveraged sectors of the economy. Contacts noted that corporate default rates were likely to increase sharply, with acute stress in the energy sector. Even before the outbreak spread to the United States, concerns related to nonfinancial corporate debt were cited frequently, with a focus on the growth in leveraged loans, private credit, and triple-B-rated bonds. More recently, surveyed respondents noted that a period of renewed outflows from credit-oriented mutual funds could lead to limits on redemptions and that stressed global insurers could become large sellers of U.S. corporate bonds.

A number of contacts also raised concerns over household balance sheets, especially in low-income segments, highlighting increases in credit card, student loan, and auto loan delinquencies as well as concerns over spillovers from nonpayments of rent and mortgages. Against the backdrop of corporate, consumer, and real estate stress, several respondents noted that bank asset quality could come under severe pressure. Smaller banks with high concentrations of lower-rated consumers, small and medium-sized businesses, and commercial real estate were viewed as especially vulnerable.

Several policy-related risks were also identified, including the risk that funding designated to support small businesses would be either insufficient to address the scale of the need or not timely enough to avert a wave of layoffs and bankruptcies. Finally, a few contacts noted the prospect that state and local governments would face large budgetary gaps, with spillovers to the municipal bond market and local economies. In the euro area, some respondents noted that the absence of more expansive fiscal resource sharing or debt mutualization could underpin a return of redenomination risk in some of the monetary union’s most indebted sovereigns.

A few respondents noted that novel investment strategies and market structures could prove vulnerable in a sustained market downturn. Specifically mentioned were the growth of short-volatility strategies, the expansion of leveraged ETFs, and the reliance in some markets on sources of liquidity that could withdraw in a shock.

Finally, geopolitical tensions were cited frequently as a medium- to long-term risk. A few contacts noted that the COVID-19 outbreak could amplify tensions and accelerate a shift away from multilateralism. Respondents also highlighted the risk of heightened trade tensions and the possibility that the virus and its fallout could accelerate global leadership changes and amplify political uncertainty.