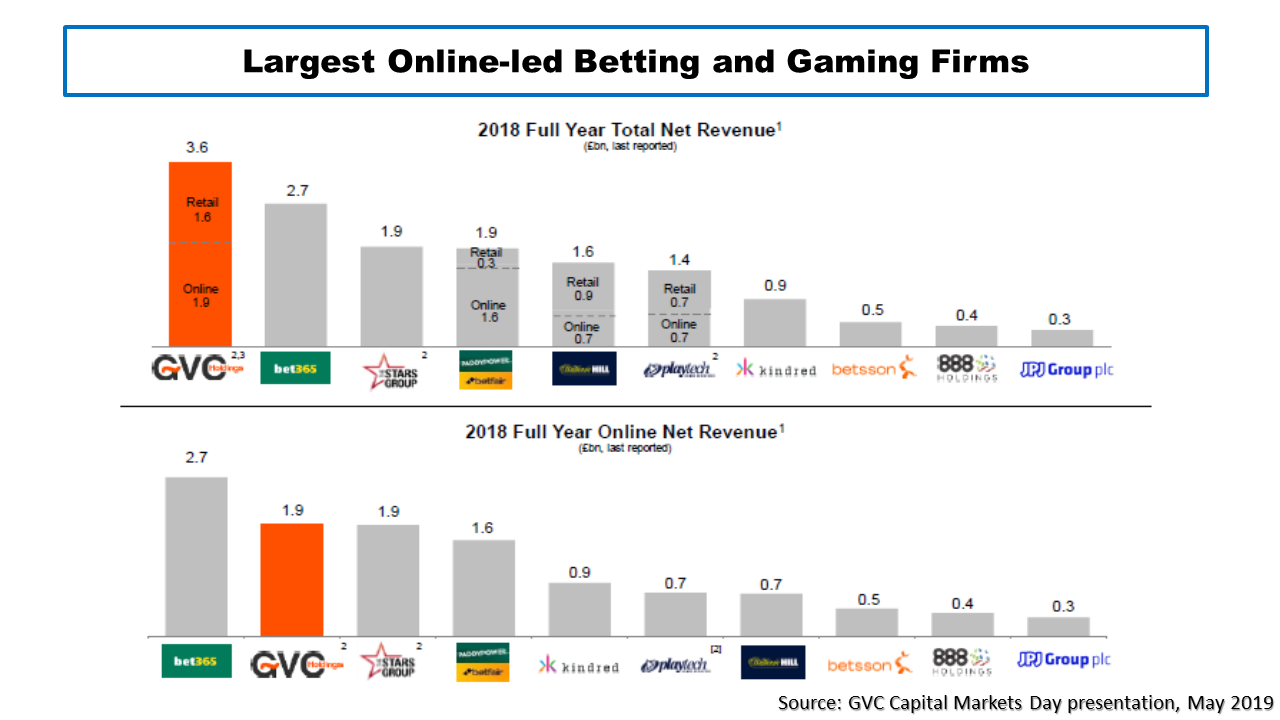

The sports betting and online gaming sector is going through transformative times. Firms like William Hill (WMH.L), GVC (GVC.L) and Flutter (FLTR.L), the new name for Paddy Power Betfair, are grappling with greater regulatory restrictions, more taxes, and the need to be seen to take the issue of problem gambling seriously (some of which are outlined in this previous post). Many of these issues are having a direct impact on revenues and margins. At the same time, they are trying to build a presence in the newly opened US gambling market. The exhibit below, from a recent GVC presentation, shows the players by revenues, both in the physical and the online market.

click to enlarge

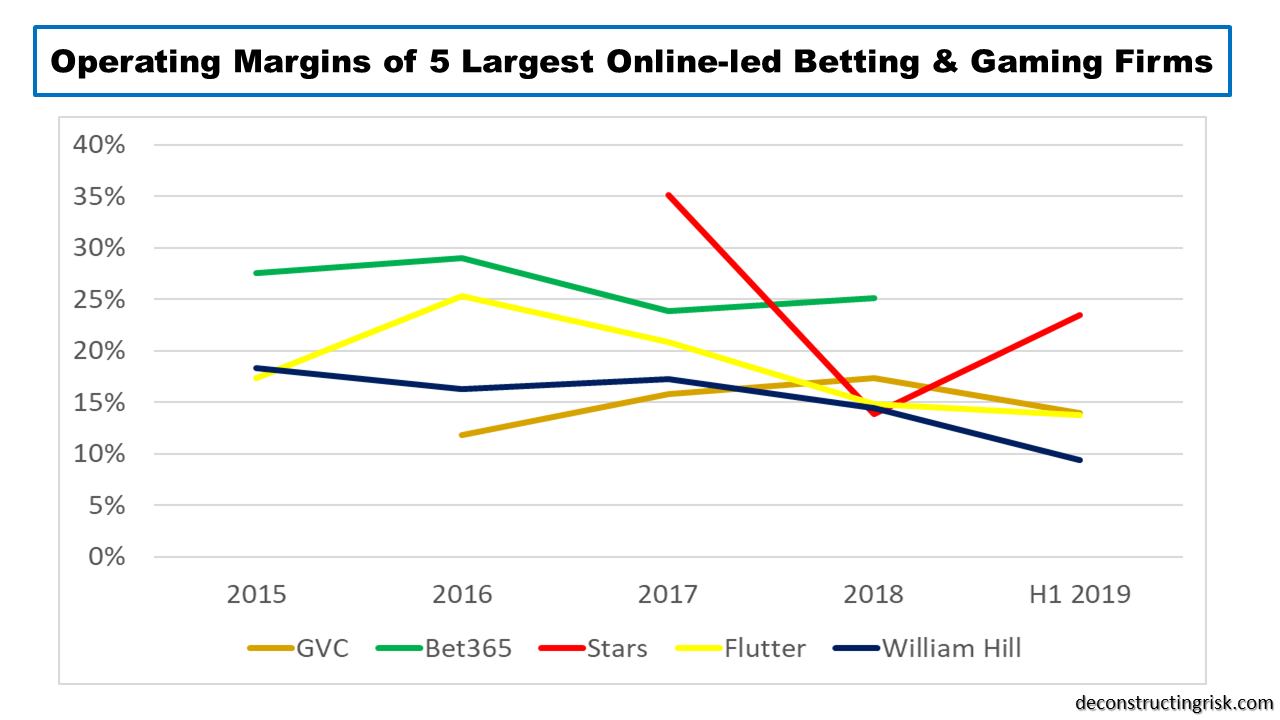

A look at the operating margins of these firms show the impact on profits for the largest firms, with the pure online players Bet365 and The Stars looking the most lucrative (although it will be interesting to see the results for Bet365 to March 2019 when they are released in November).

click to enlarge

The future size of the US market is impossible to forecast, although all the firms are highlighting the potential. As per this post (when I had time to do proper research for my posts!!), its unlikely that the US market when it matures will be as profitable as the European or Australian markets. As Flutter/Paddy Power Betfair is the best public firm in the sector (Bet365 is private) and the one I am most familiar with, and have posted on many times (here, here and here for example), I had a shot at estimating the results to 2020 and came up with an EPS of £3.54 for 2020 compared to just over £3.00 for 2019, as below. These estimates are very rough and ready, based primarily upon a doubling of US revenues and a reduction of EBITDA losses in the US to £20 million in 2020 from £55 million in 2019.

click to enlarge

Based upon today’s price, I estimate a PE ratio for Flutter (hate the name by the way) for 2019 and 2020 of 22 and 18.8 based upon the EPS estimates above. Given the risks in these business models and the uncertainties over the development of the US market (plus my negative macro outlook), that’s still too rich for my liking. For others, given there was takeover rumours a few months ago in this ever-changing sector, it may be worth the gamble.