As my previous post illustrated, I got caught up with the notion that the fall in the equity market of late was an opportunity to buy into some names in the expectation that we’d go higher into year end. It’s clear that the classic “buy the dip” strategy that has worked so well in recent years, well, doesn’t work anymore. The graph below, from a report by equity strategist Michael Wilson of Morgan Stanley, has been widely cited to illustrate the failure of the strategy in 2018.

click to enlarge

Wilson commented that “such market behaviour is rare and in the past has coincided with official bear markets (20 percent declines), recessions, or both.” There is much discussion amongst commentators about whether we are entering, or indeed have entered, a bear market. I like the simplicity of the argument by Peter Oppenheimer, another equity strategist this time at Goldman Sachs. Oppenheimer argues that a decline in corporate profits in 2019 implies a recession in the US and as a recession is unlikely in 2019, he expects corporate profits to continue to grow, albeit at a much-reduced pace.

As pointed out by Wilson, we will not know the answer about where corporate profits are going until firms report Q4 and guide for 2019. He did also say that equity analysts are always slow off the mark as they wait for firms to reluctantly report on bad news. The after the fact downgrades on NVDA are testament to that! With some commentators calling the bottom around 2,550 to 2,600 on the S&P500, it looks unlikely that there will be any major upside in the market until there is more clarity on Fed policy and the trade issues with China.

If the market moving up depends upon Fed Chairman Powell indicating a policy change to “one and wait” or for a breakthrough at the G20 on trade, then I think we’ll go down further or, at best, sideways. If there is some modest indicator that the pace of interest rate rises in 2019 will be data dependent from Powell and the G20 meeting results in a short-term cease-fire between the US and China, then markets could find a bottom and stabilize. Whatever about the likelihood of the Fed rescuing the market (unlikely in my opinion), I fear that any meaningful relaxation in US-China tensions is against the play-book of the Orange One in the White House. The rhetoric from side-kick Pence at the weekend with language indicating China was leading other Asian countries into debt bondage does not bode well for next week’s G20 summit.

On China, I really like Ray Dalio’s explanation of the fundamental difference between the Chinese and US system (here is just one example of his latest thoughts), being a top down versus a bottom up approach. As Dalio explained it, the Chinese place an importance on family and paternal direction as opposed to the US adoration of the individual above all else. Unfortunately, I doubt that the current US leadership has the intellect to nuance a workable resolution between these two philosophies.

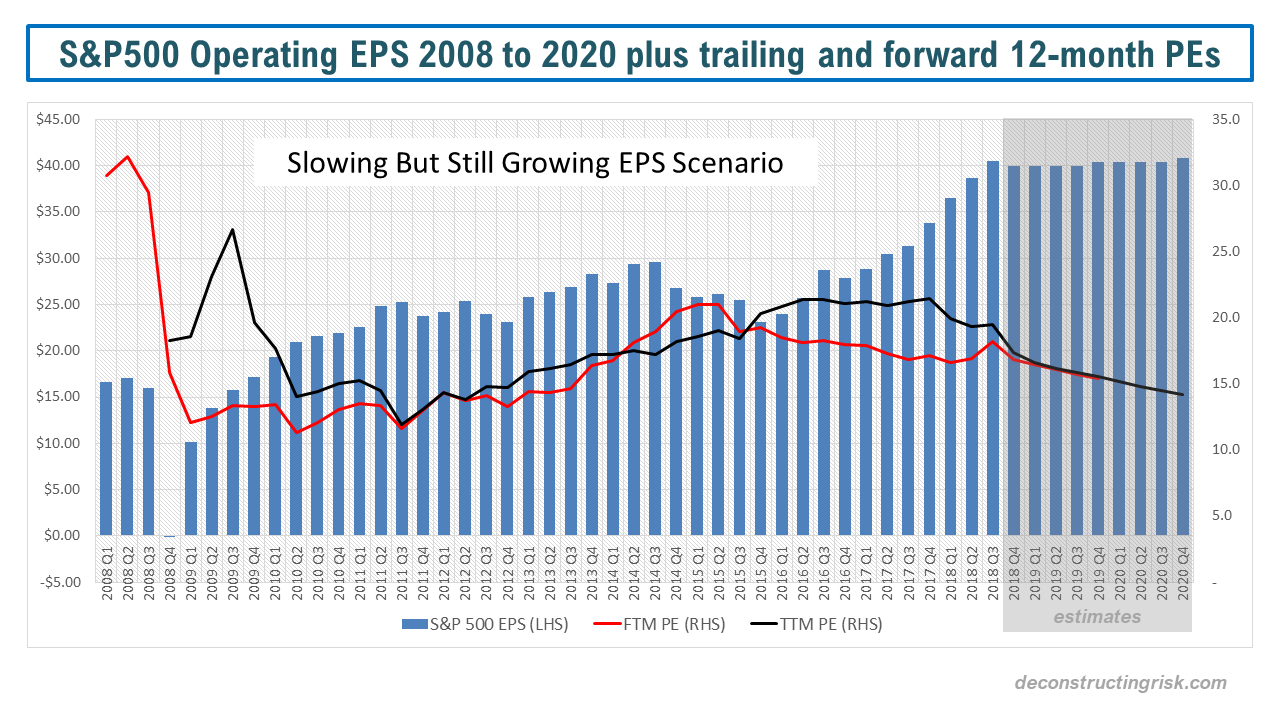

Following on from the analysis in this post on peak quarterly earnings, the current market narrative is that the EPS estimates for 2019 and 2020 will come down over the coming months. Currently S&P is showing a 11% projected increase for 2019 operating EPS for the S&P500 (13% on a reported EPS basis). The current market jitters indicate the market view those figures as unrealistic. Oppenheimer indicated that Goldman Sachs is currently thinking about a 6% and a 4% growth in EPS for 2019 and 2020 respectively is more realistic. Wilson indicted Morgan Stanley are projecting EPS growth for 2019 in the low single digits.

Given that estimates usually increase over time in the good years and decease in the bad years, I am going to assume a 3% and 1% increase in operating EPS for 2019 and 2020 respectively in this no recession but slowing growth scenario. Given that forward multiples would also decline in such a slowing environment (I have assumed to a modest 14), I estimate year-end targets for the S&P500 for 2019 and 2020 of 2,500 and 2,300 respectively, a decline of 6% and 13% respectively over the S&P500 today! The graph below shows the scenario as described.

click to enlarge

Economies generally don’t have slow gentle soft landings, it’s nearly always turbulent. Just look at the chart above to see how improbable the gentle scenario is compared to history. We need a major boast, such as a comprehensive resolution of the US-China trade issue, to maintain the bull market. Otherwise, I suspect the great EPS growth party is over.

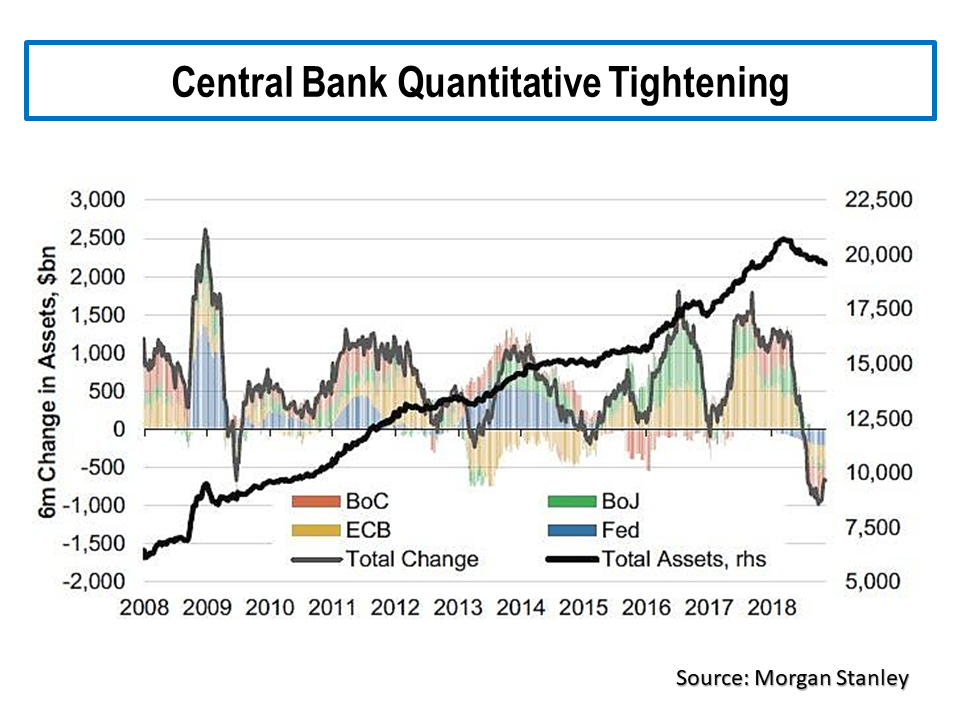

Interestingly, Morgan Stanley also highlighted the headwind of quantitative tightening, as per the graph below, on the current market fall. I last discussed this issue in this post in January.

click to enlarge

No more buy the dip for a while yet I fear…….

There might be one heck of a dip to buy, but probably 2 to 3 years down the road. But then I have been thinking along those lines for quite a while and sound like a broken record…

Eddie

i hear you Eddie, I have been agonizing about whether to buy a load more AAPL…

Thought the reaction to Powell wa funny. To my mind, saying you are a long way from the neutral rate when you were at 2% and the average neutral rate was assumed to be 3% is exactly the same as saying your are just below the range of 2.5 to 3.5 of the neutral rate when you are at 2.25. But hey, the market sees what it wants to see….

M

Depends on how speculative inclined you are I would say ;). The Oracle has been buying hand over fist, so an alternative would be to buy BRK instead to get some AAPL exposure (50bn of that market cap should be AAPL iirc) plus a lorry full of cash plus some nice optionality.

Imho this was Central Banker Jujutsu. Having said that he can go back to His Orangeness and say “I didn’t raise rates more. If the economy falls off a cliff in 2019 it’s not my fault.” If you want to learn more check out John Hussman’s latest comment (https://www.hussmanfunds.com/comment/mc181128/). Pure alpha if you ask me.

Eddie

Too true, I would if I could on Berkshire although they down more than AAPL today. Decided to wait on AAPL until I see what the numbers look like this qtr.

Fascinating market today, this is what our machine future looks like!!