Wow, what a December this has been in the equity markets! Not a buyer in sight as we (effectively given the Christmas break) end the year at the S&P500 close today of 2,417. This really is a market to stay well away from. I suspect Q1 2019 will again be volatile until we get into earnings season and get a taste of the sector 2019 EPS projections (a minor relief rally from institutional funds allocating capital followed by more programme selling is my guess).

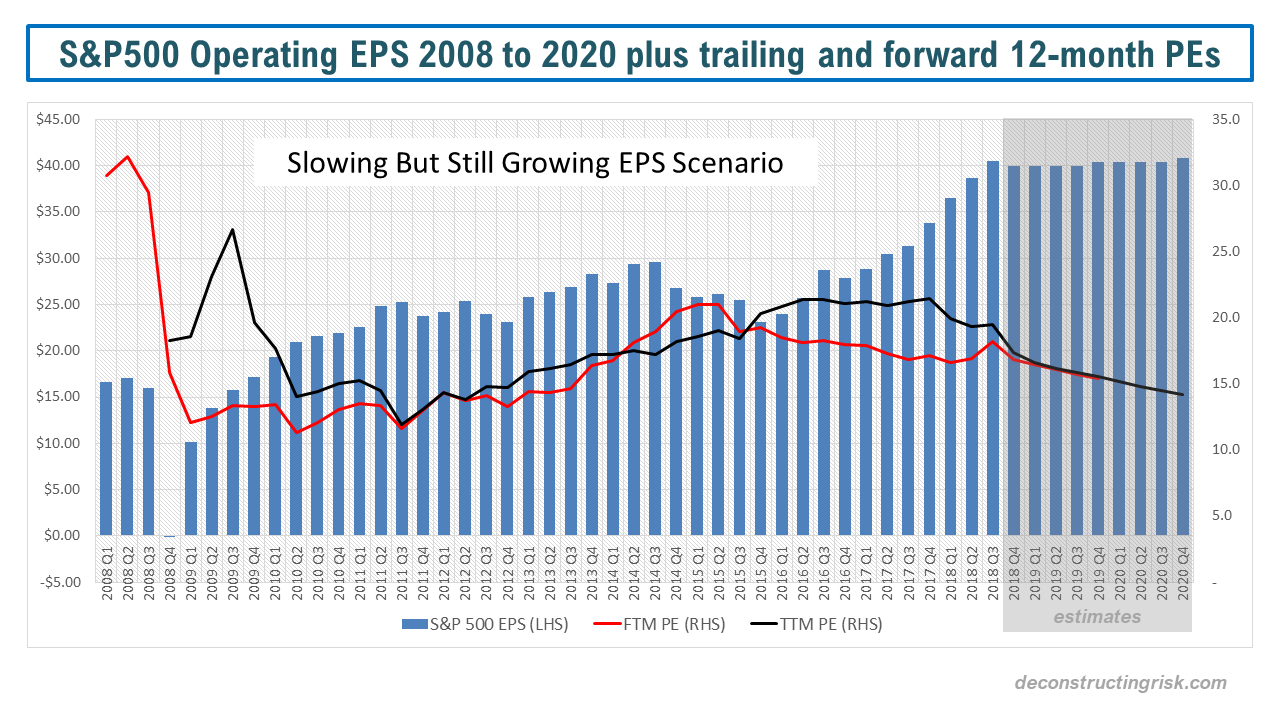

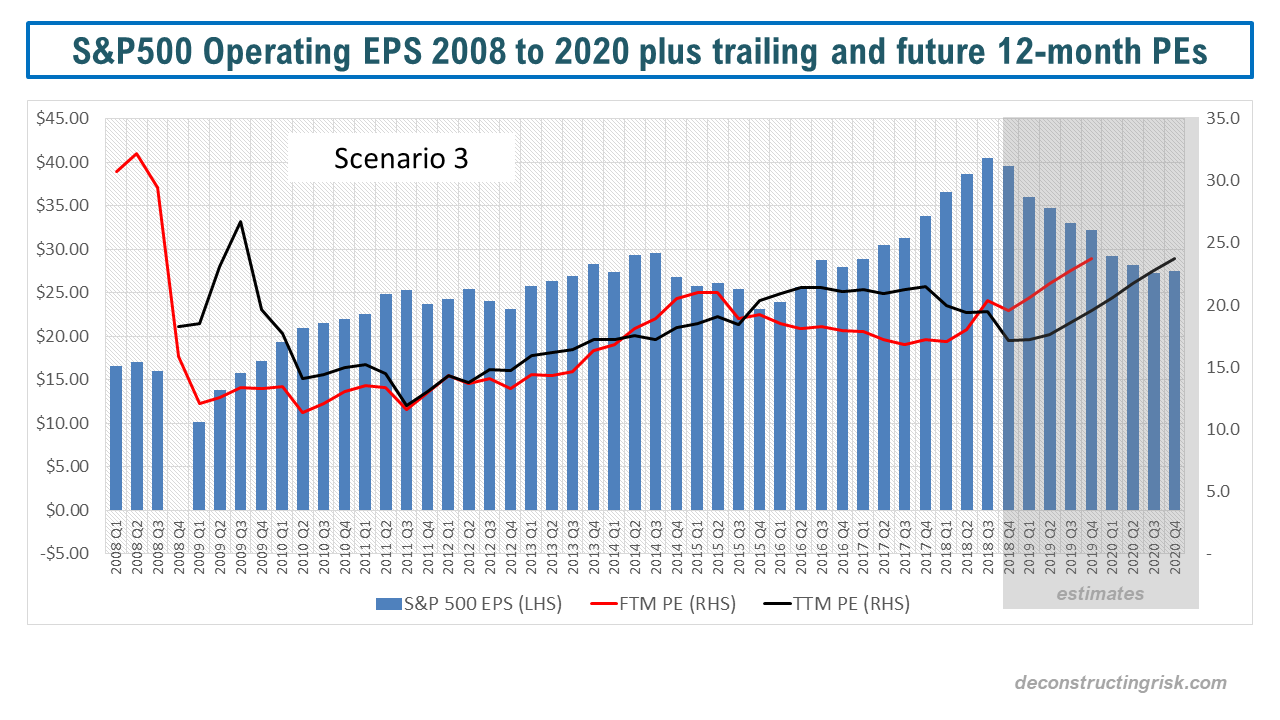

This recent post postulated that with small single digit EPS growth for 2019 and 2020, a slowing but non-recession scenario, a range of 2,500 to 2,300 on the S&P500. Well, we’re bang in that range now!! And the consensus is for more downside with the probability of a recession beginning next year raising by the day. Not even dovish statements today from John Williams of the New York Fed could tempt the buyers out of hibernation. The prospect of the demise of the Fed put has freaked the market out this week. My crude calculations estimate that a slow drop in operating EPS over 2019 of 6%, likely in a mild recession scenario, could result in the S&P500 testing 2,000.

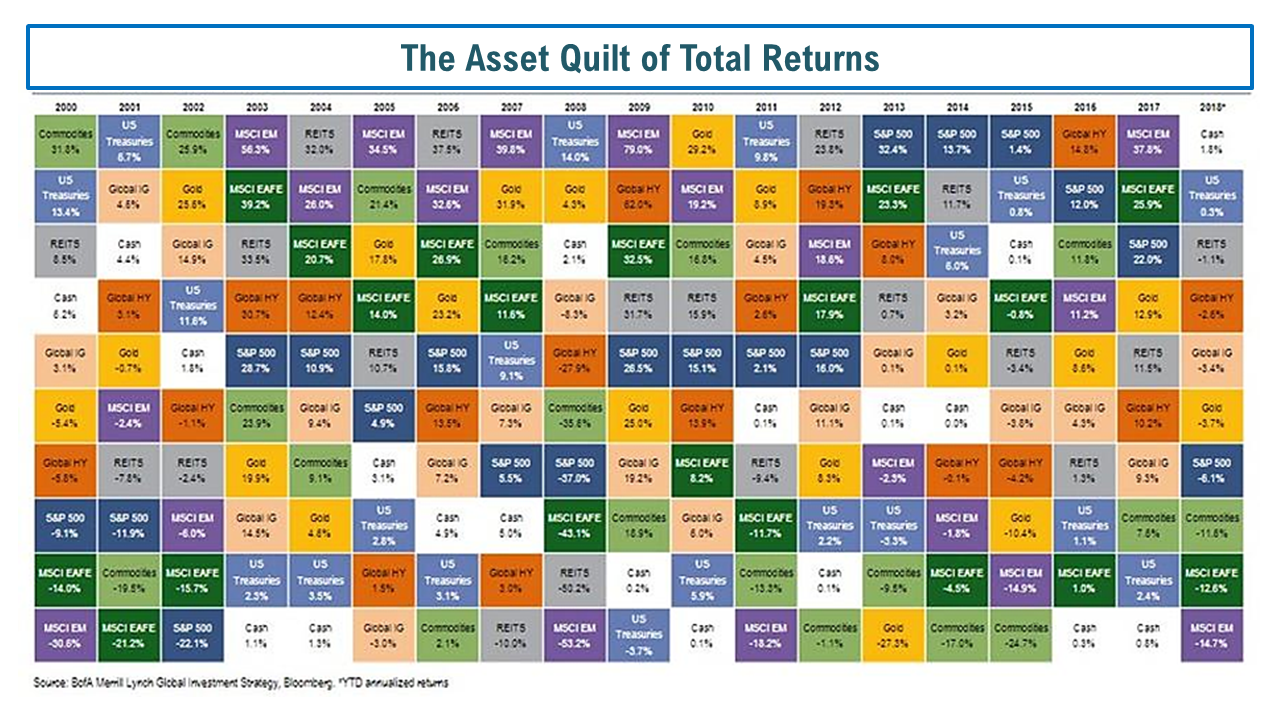

I have been bearish on this market for several years (here, here and here are just recent examples) and although the majority of my assets have been in cash throughout 2018, the graph below from BoA Merrill Lynch, sends a shiver down my spine. As with most people, my equity positions have been hammered. According to BoA ML, the last time there was positive cash and negative equity, credit, and government returns in the same year was 1969. To plagiarize the old investing adage, it would take some monkey to call a bottom on this equity market any time soon.

Click to Enlarge

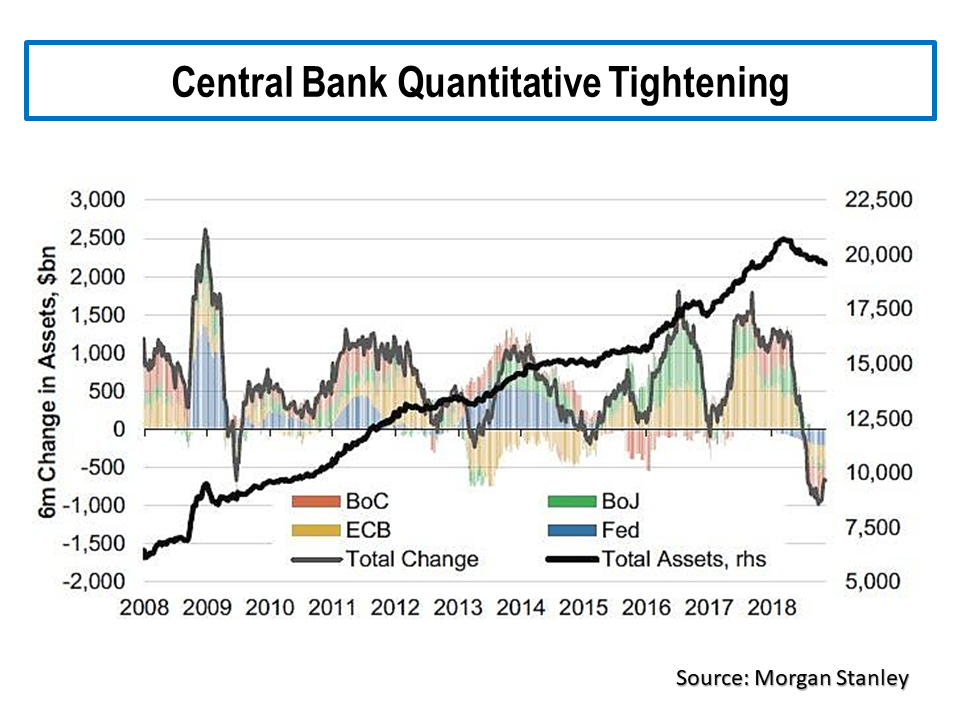

The outlook for 2019 is highly uncertain at the current point in time, nobody really knows how it will pan out and I’ll leave the musing over that topic to future posts. As this post in January highlighted, I do think quantitative tightening and the great unwinding of Central Bank easing experimentation is having some nasty unintended consequences.

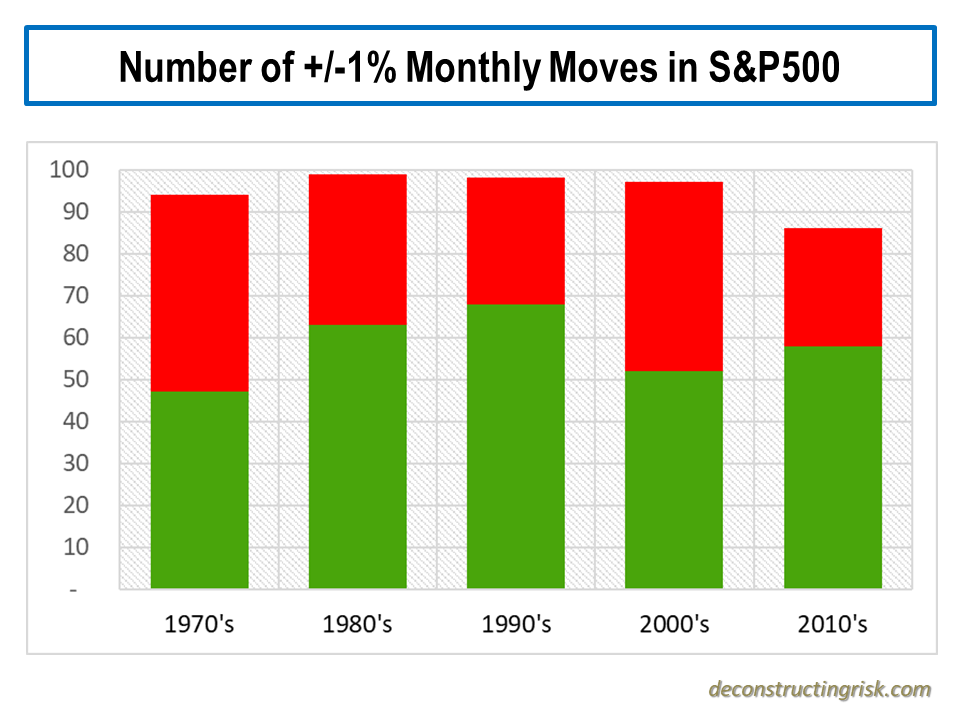

At this time, I do find it insightful to look at recent movements in a historical context. If you look at the number of months with moves greater than or equal to +/-1% in the S&P500, the comparison between the decades is as below. The number of such moves are surprisingly consistent across the decades.

Click to Enlarge

If we assume that the 1970s and the 2000’s were extraordinary decades with the oil and financial crises respectively, then there could be more up months than down months due in the remainder of this decade for it to look more like the 1980s or the 1990s. A pretty flimsy analysis admittedly!

Continuing the theme of trying to end the year on a positive note, if we look at the historical months with moves of +/-5%, as below, it could be argued that the recent volatility is healthy as extended periods of reduced volatility prior to the dotcom bubble and the financial crisis didn’t end well!!

Click to Enlarge

That’s a happier note to end on (albeit rather pangloss).

A very happy and healthy Christmas to all who have spent any time reading my musings this year.