Going into the Q2 earnings for Centurylink (CTL), the market was showing mixed signs. AT&T grew its business revenue by 2% sequentially while Verizon’s was down 2.6%. Frontier, the troubled rural consumer telecom threw in the towel on its expected revenue synergies in its latest turnaround plan, in what looks like a suspiciously pessimistic report prior to a major debt restructuring play (that’s a whole different on-going distressed story that’s fascinating to watch).

When CTL did report their Q2 results last week, the top line was down sequentially 1.2%, with business down 1.1% and consumer down 1.7% (after disappointing subscriber growth above 20Mbps). The shares took a hit although they have traded strongly since. To put the results in context, CTL has lost $620 million in revenue for H1 2019 over H1 2018, a fall of 5.3%. The fact that EBITDA grew by $80 million half year to half year is a testament to CTL’s management team and their proven ability to execute on synergies and their cost transformation programme. Notwithstanding this ability, top-line cannot decline at 5% forever without EBITDA getting hit at some point, and that’s the bear case in a nutshell. With a current leverage multiple of 3.8, once EBITDA starts to fall, the path is a well-known one for leveraged telecoms, with Frontier being just the latest example in a long line.

So why am I sanguine about CTL? Firstly, CTL is primarily a business wireline telecom and the announcement that they completed an upgrade of their US intercity network with 3.5 million fiber miles of the latest Corning fiber technology in June using their extensive empty conduit network (Level 3 built 12 conduits and other integrated networks from Quest, Wiltel and Broadwing had 3 to 4) was a major positive surprise that reinforces its competitive strength. They will complete their European upgrade with another 1.2 million fiber miles by early 2021. What impressed me is that they obviously have dark fiber clients lined up for this new ultra-low-loss fiber network build, as inferred in the Q2 conference call with references to prior build consultations with clients, and yet, despite the pressures on CTL over the past 12 months, they kept it quiet until now.

Secondly, as outlined in the Q2 presentation and the press release this week, with further detail from CTO Andrew Dugan at the Cowen conference talk on Tuesday, they are making significant investments in 100 edge computing locations with capability for 5 milliseconds of latency uses. From these events, it also looks likely that they have a major 2,000 location transportation and logistics client lined up for this capacity (some have speculated it could be Fedex).

Both investments highlighted above are within their capex budget announced at the beginning of the year and show management’s discipline and focus in investing in capacities for future networking demands.

Thirdly, and most importantly, they followed through on restating their previous guidance that the enterprise and global units, which make up nearly 60% of business revenue, would show revenue growth in H2 over H1 whilst maintaining their overall 2019 financial guidance. After following this management team for several years now, and given the discipline they have shown recently, they would not make these claims lightly. The CFO Neel Dev stated that “the driver for enterprise growth is sales and installs” which infers a high level of insight into Q3 and Q4 trends.

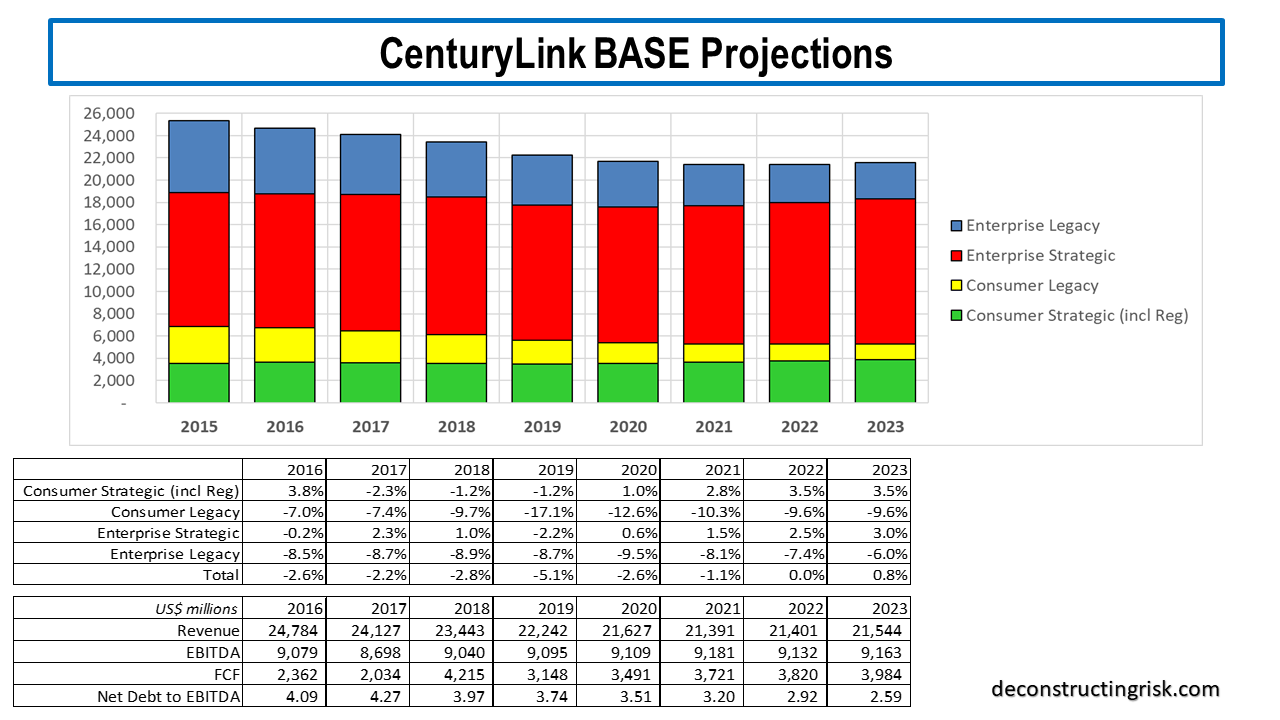

So, taking these latest data-points into account, I have again sharpened my pencil for my base and pessimistic projections, as per the exhibits below.

click to enlarge

click to enlarge

As before, the pessimistic scenario assumes the dividend is scrapped altogether in 2020 so that the (top of the) debt reduction range can be met by year end 2021. In the base scenario, overall revenue doesn’t bottom out until 2022 whilst its not until 2024 under the pessimistic scenario (both have been pushed out another year from my previous post). All other assumptions are as per my previous analysis.

My DCF valuation for CTL in the base and pessimistic scenarios is now $25 and $9 per share respectively (down from $28 and $10 per share respectively in my previous post). Despite my heightened concerns about the current macro environment, I have picked up some shares recently (my average is $13 per share now) as a reflection of my cautious optimism about H2. I hope I wouldn’t regret it in the coming months!