Staff from IOSCO issued a report in April on the global corporate bond market. Although there was nothing earth shattering in the report, there was some interesting insights. The report highlighted 4 themes as below:

- Corporate bond markets have become bigger, more important for the real economy, and increasingly global in nature.

- Corporate bond markets have begun to fill an emerging gap in bank lending and long-term financing and are showing potential for servicing SME financing needs.

- A search for yield is driving investment in corporate bond markets. A changing interest rate environment will create winners and losers.

- Secondary markets are also transforming to adapt to a new economic and regulatory environment. Understanding the nature and reasons for this transformation is key in identifying future potential systemic risk issues and opportunities for market development.

The report also highlights the uncertainty that remains on secondary markets in the event of a interest rate shock and the $11 trillion worth of corporate debt (out of $50 trillion) due to mature in the next seven years.

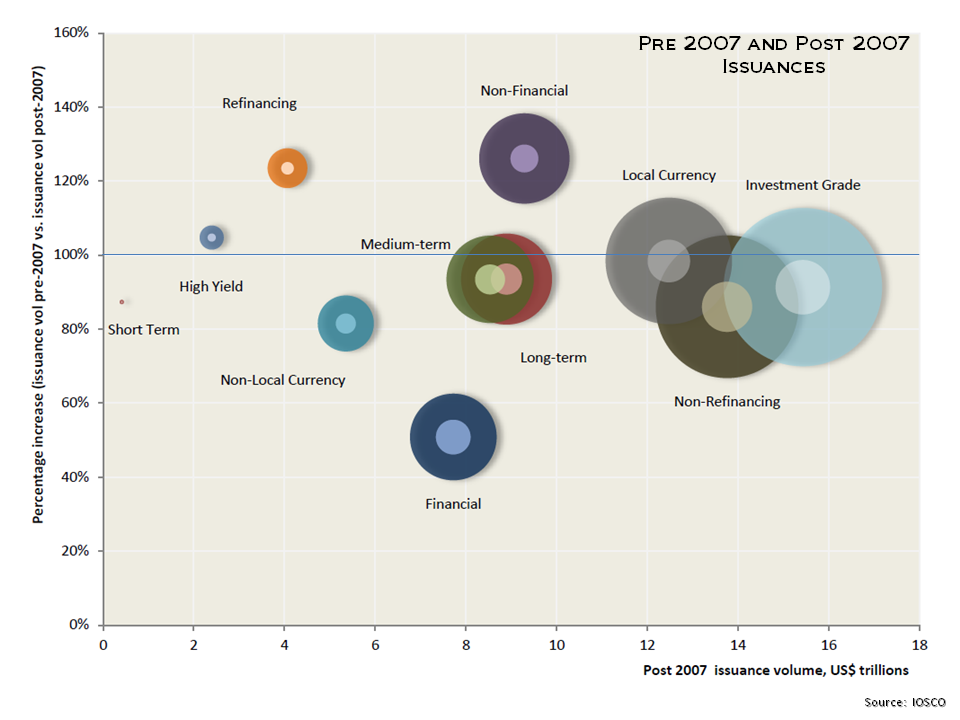

Some interesting graphs in the report include the one below on the different characteristics of issuances pre- and post- 2007.

click to enlarge

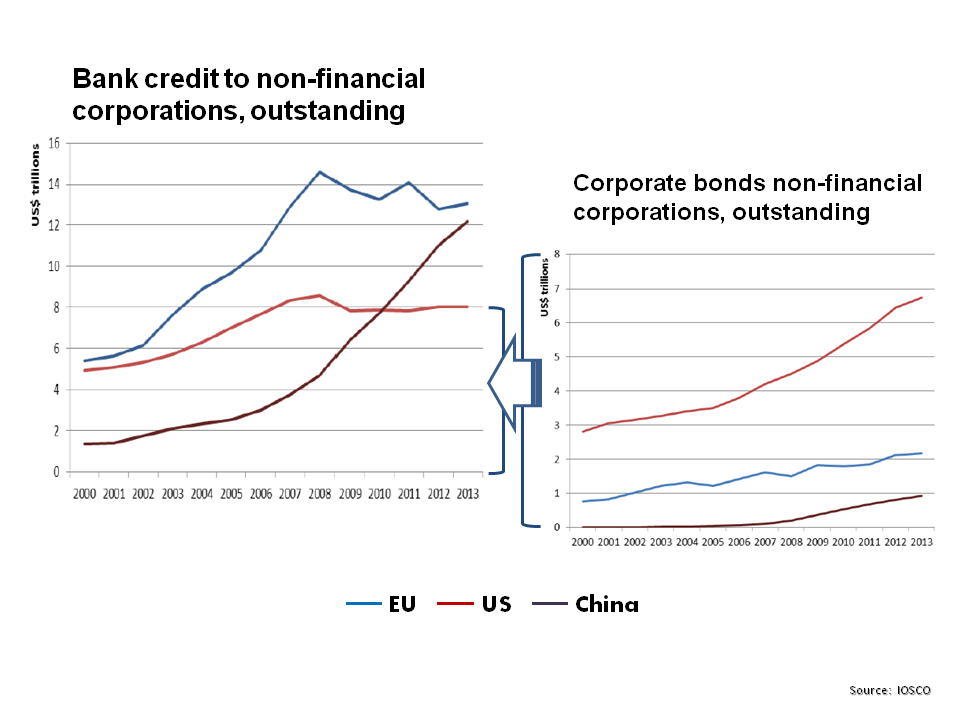

Other interesting graphs highlight how corporate bonds are taking up the stagnation in bank credit in the US and the EU, and also highlight the boom in bank credit in China, as below.

click to enlarge

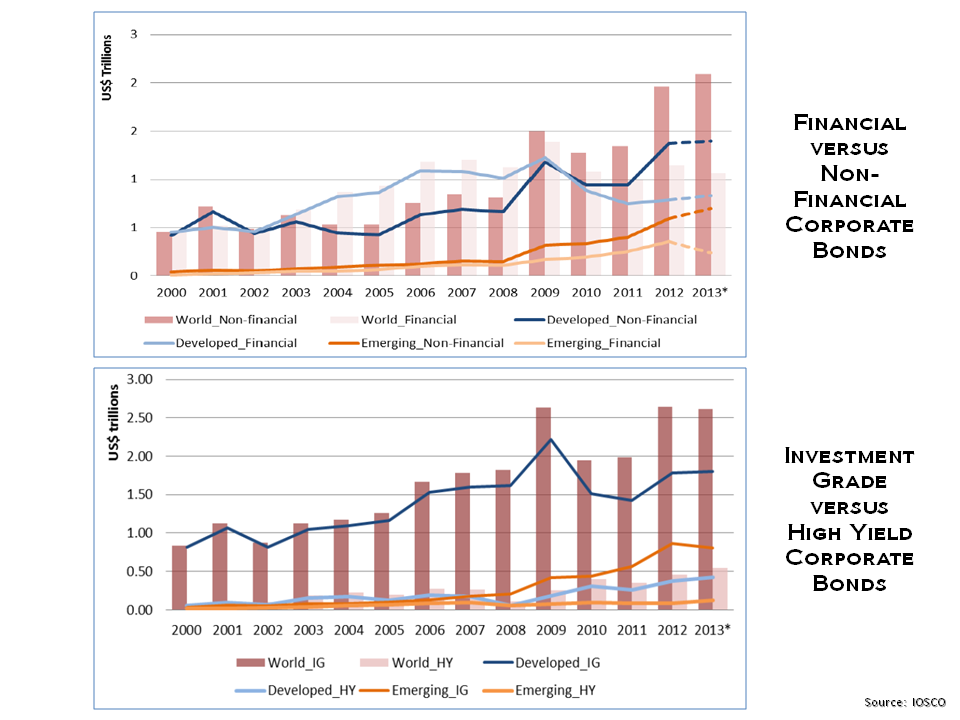

And finally the graphs below show the increase in non-financial corporate bond issuance and the modest growth in high yield issuance.

click to enlarge

Not sure whether I would call the growth in HY issuance modest. In terms of absolute figures, yes, still not that large, but in relative terms the amount almost doubled between 2011 and 2013. Which is a significant uptick imho (hunt for yield etc).

Eddie

Thanks Eddie,

Yep size wise HY has more than doubled since pre-crisis.

I saw comments from PIMCO that LBO deals are been done at high valuations, proforma ebitda multiples, covenant lite, and dividend before coupon terms. All depressingly familiar although hopefully the macro picture is more stable. Hopefully….

M

Talking about LBOs do you remember those 8x Debt/EBITDA buy-outs before the crisis ? The WSJ said the other days that deals with a 7.5x leverage are already back. 40% of all new lev loans are cov-lite or don’t have covenants at all afaik. Sounds all too familiar.

Eddie