The bull market is raging ahead with the S&P500 and the Dow both less than 1% away from key levels and Apple breaking $100 yesterday. Given my cautious stance on the market, as articulated in multiple posts for over a year now, it is therefore uncharacteristic of me to be talking about establishing a new position. After having watched Trinity Biotech, ticker TRIB, for nearly a year now (I previously posted on the firm last year here), I have been doing some more research and modelling on the firm.

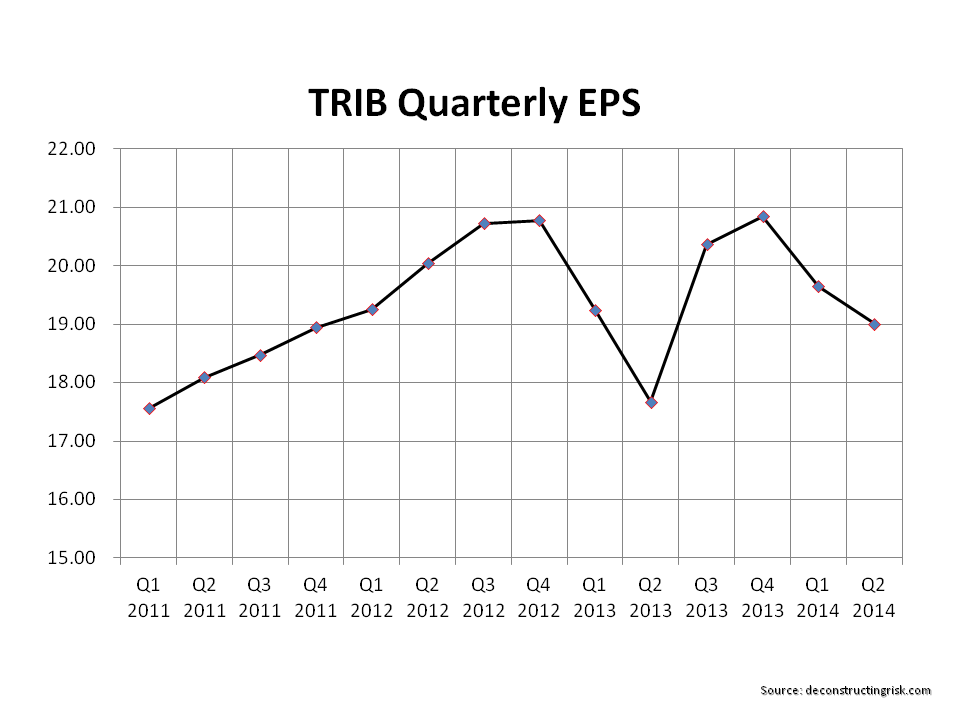

Last September, when the stock was trading around $19, I concluded that despite an attractive pipeline of new products following a number of acquisitions by TRIB, the stock was overvalued given the execution risks involved. Since that time, the stock climbed steadily to over $27 after Q3 and Q4 results last year before falling to trade around $23 since March before dropping to around $21 for the past few weeks. The graph below shows the quarterly EPS for the past 14 quarters.

click to enlarge

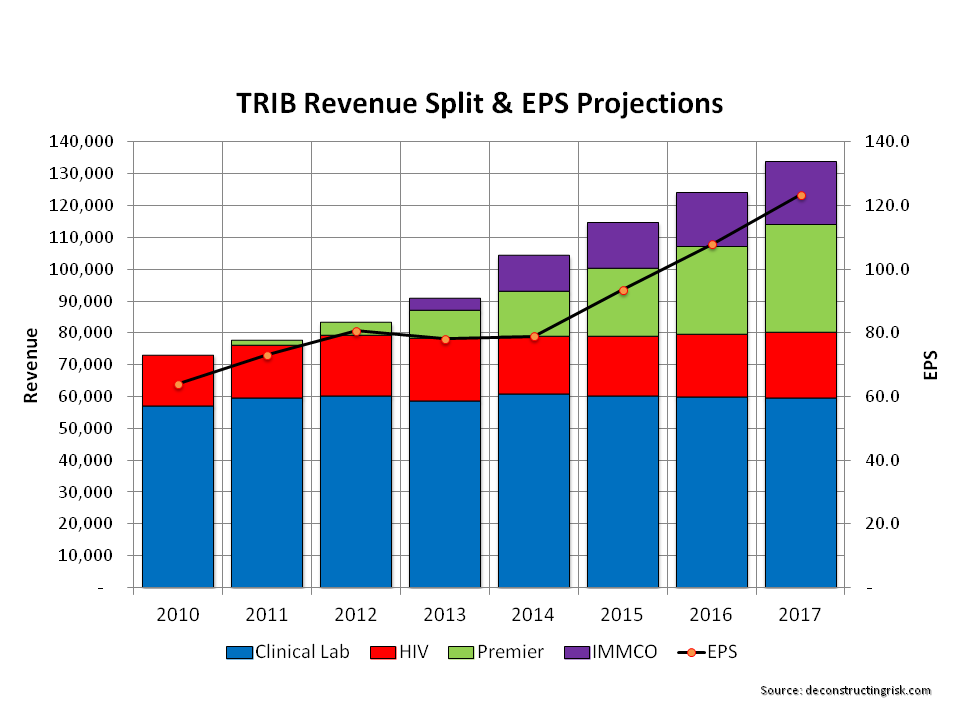

The past two quarters have been hit by subdued revenues, due to timing delays on Premier reagent income and lower lyme sales, and higher expenses from consolidating manufacturing costs and trial expenses on the Meritas Troponin cardiac test. In addition to the EPS misses, the recent drop may be as a result of cooling off on the tax inversion restructuring craze by US firms. There is always the possibility that it’s a result of some as yet unknown development (the impact of the Ebola outbreak on HIV test product sales in Africa is an example)!! Notwithstanding such a development, I spent some time going through TRIB’s releases and calls. The graph below represents my best efforts at a forecast.

click to enlarge

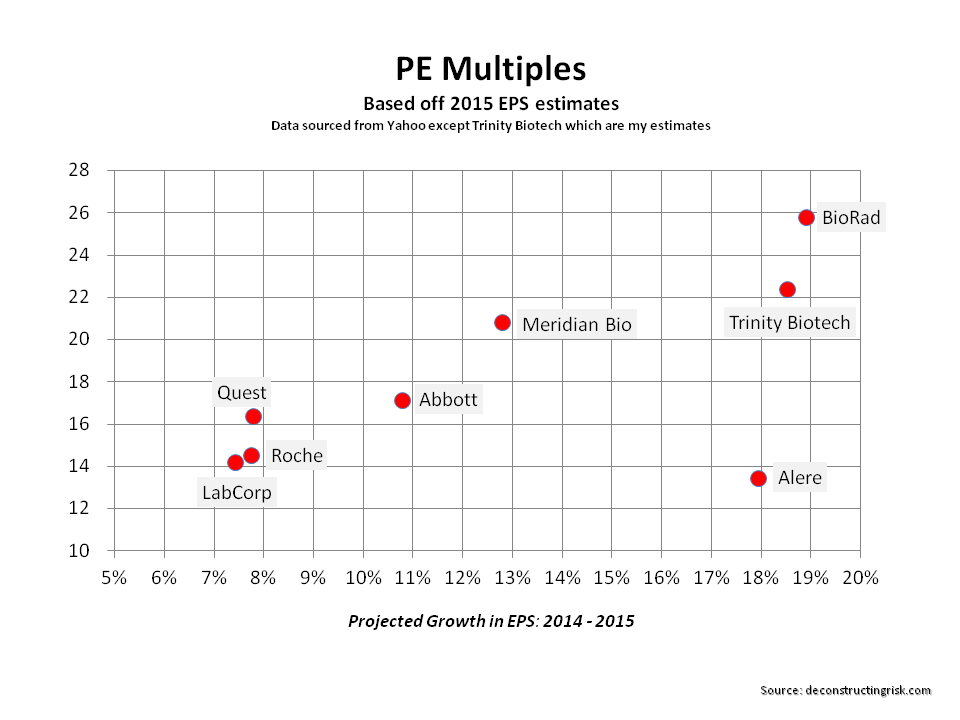

My revenue and EPS estimates for 2014 are slightly below estimates. My revenue and EPS estimates for 2015 are 10% and 15% below consensus respectively. Using my EPA estimates with the consensus estimates for TRIB’s competitors from yahoo-finance, the graph below shows the relative valuations of TRIB and selected competitors.

click to enlarge

This analysis shows a stock with good growth potential but one which is trading at 22 times forward earnings. Add in that TRIB have spent their cash-pile and have intangibles of $138 million making up 58% of assets (with a history of having to write-off intangibles, see previous post). Not exactly a cause to jump up and down. Indeed there are many similar growth stocks trading at lower multiples (such as SIRO as per a previous post). So, what’s the reason for my change in heart on TRIB?

Well, it’s really all about the aforementioned Meritas Troponin cardiac tests, the high sensitivity quantitative point-of-care immunoassay platform TRIB purchased in the Fiomi deal (Note – the financial projections above exclude any assumed benefit from these products). The worldwide market for point-of-care cardiac testing currently stands at about $650 million (with a larger potential for other related add-on tests) and is heavily U.S. centric. The market is dominated by three firms – Alere, Roche and Abbott – and will be a tough one to break into. However, new guidelines in the US mean that the existing products are no longer fit for purpose. A letter, dated the 25th of June 2014, from the FDA stated that “laboratories and clinicians using these troponin test results are not generally aware that the performance data listed in the device labeling is obsolete.” The letter further states the following:

“To address these concerns while improving patient care, FDA has started working with troponin assay manufacturers to modernize the performance evaluation and regulatory review of these critical tests. Our main interest is to ensure that laboratories and clinicians are informed of the true performance of troponin assays to help in result interpretation and laboratory verification of performance parameters. This is particularly important for newer, more sensitive troponin tests which may render values that can be difficult to interpret if sufficient information is not available in the device labelling. These recommendations solidified troponin’s importance in MI diagnosis and triage; at the same time, they formalized an adjustment in the clinical cutoffs and changed the way troponin results were interpreted and used.”

TRIB have obtained a European CE certificate for one of their Troponin tests and hope to gain another shortly (end of August was mentioned). However, Europe generally follows the US and the real approval required is from the FDA in the US. Studies conducted for the CE certificate show very positive results albeit with approximately 20% of the sample size required in the US, on US patients. The size of the studies required in the US has been the reason behind recent delays although TRIB hope to complete the studies and submit the results to the FDA by year end. FDA approval could then take up to 6 months so mid-year 2015 is a reasonable target date. However, these studies are dependent upon getting enough targeted patients into the study and that can be uncertain.

So, TRIB have a market opportunity for a new product line which they say has been proven in trails (albeit smaller than the FDA mandated sample sizes) to exceed the new guidelines. The opportunity is significant and will pit TRIB against some big names competitors (although Alere seems to be in a bit of a mess right now). Analysts estimate the option value of the cardiac products at between $8 to $10 per share depending upon the underlying assumptions of probability of the FDA approval and subsequent market penetration for Meritas.

I like the potential risk dynamic here as I see TRIB’s core business improve its performance over the coming quarters. News flow on the Troponin trials will likely drive share volatility but if future profits on the stock over the coming quarters from improving operating results could be used to buy options to play the embedded call in TRIB share price on the Troponin products, I can see a win:win situation arising. That does require taking a risk today however with the share price around $21. Although it is against the grain of where I believe the overall market is headed, I therefore established a small position in the stock earlier this week. Maybe I am just getting bored of the sidelines and being reckless!! Time will tell whether I am timing this really badly or not.