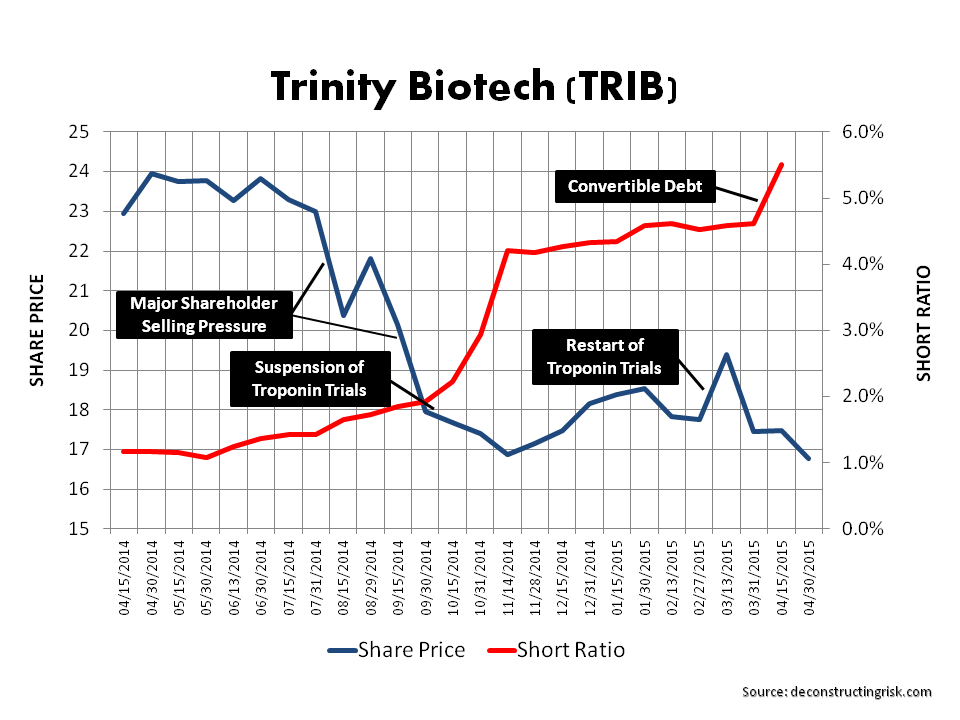

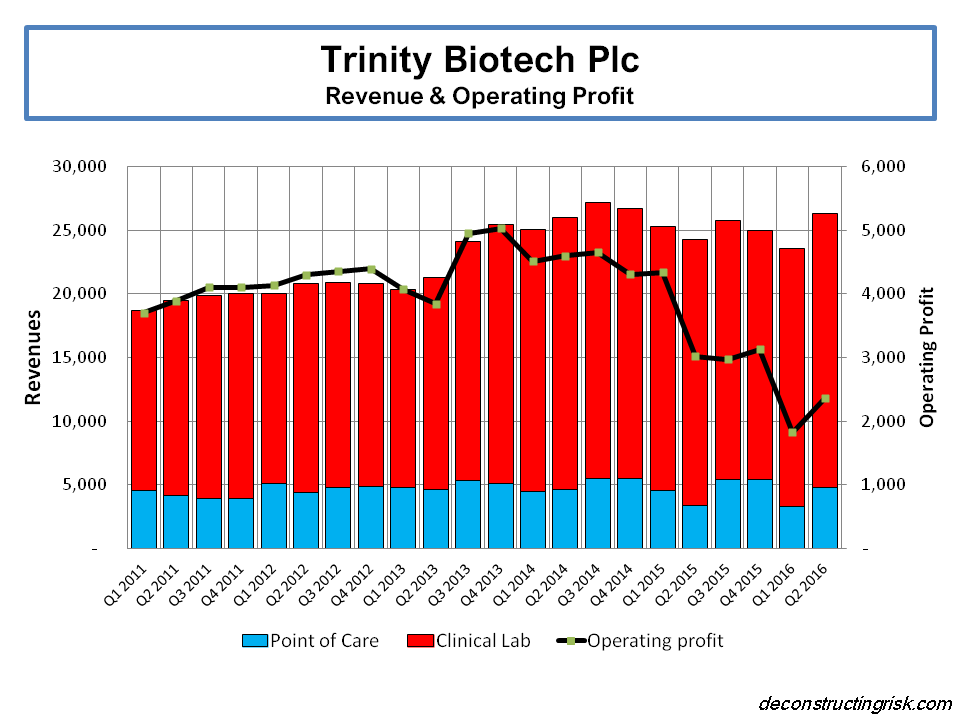

In May last year I posted on an undisciplined investment, Trinity Biotech (TRIB), which I bought at $21 per share and, after ignoring some basic investing rules, didn’t sell until it hit $16. I had thought that the underlying metrics of TRIB existing business would improve, with a big upside potential with the FDA approval of its Meritas Troponin Point-of-Care test (as outlined in this post). Since last year, I have kept an eye on the firm as their operating results continued to be uninspiring, as per the graph below.

click to enlarge

I continued to monitor the firm from afar to see how the FDA approval was progressing, for curiosity sake more than anything else (the investment case was similar a coin toss given the operating results and I have, thankfully, grown out of such gambles). The timing of any final approval was dependent upon FDA queries but Q4 was been talked of as a possible time for a final FDA decision.

It has therefore come as a considerable shock to all stakeholders, and a 50% collapse in the share price, when TRIB announced early on Tuesday that it has withdrawn its FDA application for the Troponin test on the advice of the FDA itself. Analysts representing investors vented their anger at the company’s management on the conference call on the news (worth a listen if you are so inclined).

I genuinely felt sorry for management as they tried to explain the “devastating news” about how they could have got the FDA approval so wrong. Although the FDA would not go into the gritty details on a 30 minute call communicating the news to management behind their “minded to refuse” position, TRIB’s management were restrained in expressing their (obviously very disappointed) view that the FDA had moved the goal posts in their assessment criteria. The FDA will give TRIB more detail on their decision over the coming months (strangely only on the condition that TRIB withdrew their application).

Management expressed their view, based upon the information from the FDA call, that any new application was unlikely given the large R&D expenses needed to address the issues raised and announced they would shutter the programme, reducing their annual capitalised expenses from $9 million to $1.5 million including the closure of their Swedish facility. Given they capitalise most of these expenses, the impact will primarily be on cash-flow rather than on the P&L (they may manage to be cash-flow neutral on a pro-forma basis). Insight into future operating results and what the balance sheet will look like after the write-offs needed on this withdrawal may come with the Q3 results.

At a share price of approx $6.50, TRIB indicated that their Board would likely instigate a large buy-back programme after the early release of their Q3 results (likely due by mid October). With $85 million of cash left from their $100 million convertible debt, TRIB has the firepower if it can get to positive cash-flow on an operating basis in the near term. Analysts were very blunt in their reaction, stating that management now had a major credibility issue and that a sale of the firm should now be the priority.

All in all, a sad day for TRIB, its employees and its future prospects. And, of course, for its shareholders.