Many things will be written about the events of 2016.

The populist victories in the US election and the UK Brexit vote will no doubt have some of the biggest impacts amongst the developed world. Dissatisfaction amongst the middle class across the developed world at their declining fortunes and prospects, aligned with the usual disparate minorities of malcontent, has forced a radical shift in support away from the perceived wisdom of the elite on issues such as globalisation. The strength of the political and institutional systems in the US and the UK will surely adapt to the 2016 rebuff over time.

The more fundamental worry for 2017 is that the European institutions are not strong enough to withstand any populist curveball, particularly the Euro. With 2017 European elections due in France, Germany, Netherlands and maybe in Italy, the possibility of further populist upset remains, albeit unlikely (isn’t that what we said about Trump or Brexit 12 months ago!).

The 5% rise in the S&P 500 since Trump’s election, accounting for approx half of the overall increase in 2016, has made the market even more expensive with the S&P 500 currently over 60% of its historical average based upon the 12 month trailing PE and the Shiller CAPE (cyclically adjusted price to earnings ratio, also referred to as the PE10). A recent paper by Valentin Dimitrov and Prem C. Jain argues that stocks outperform 10-year U.S. Treasuries regardless of CAPE except when CAPE is very high (the current CAPE is just above the “very high” reference point of 27.6 in the paper) and that a high CAPE is an indicator of future stock market volatility. Bears argue that the President elect’s tax and expansionary fiscal policies will likely lead to higher interest rates and inflation in 2017 which will further strengthen the dollar, both of which will pressure corporate earnings.

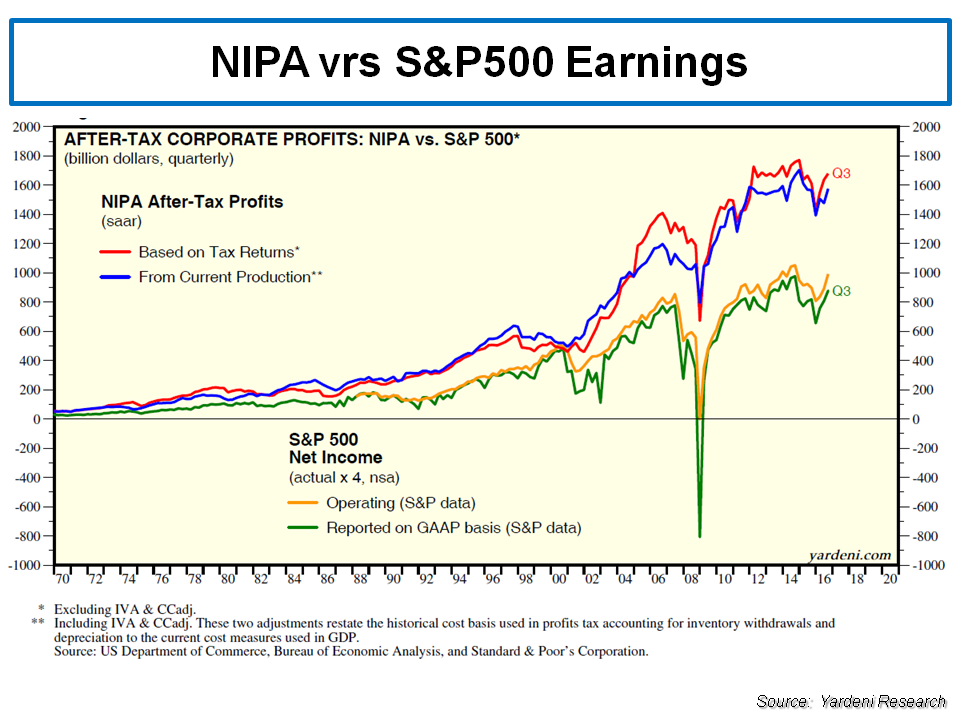

Critics of historical PE measures like CAPE, such as Jeremy Siegel in this paper (previous posts on this topic are here and here), highlight the failings of using GAAP earnings and point to alternative metrics such as NIPA (national income and product account) after-tax corporate profits which indicate current valuations are more reasonable, albeit still elevated above the long term average by 20%-30%. The graph below from a Yardeni report illustrates the difference in the earnings metrics.

click to enlarge

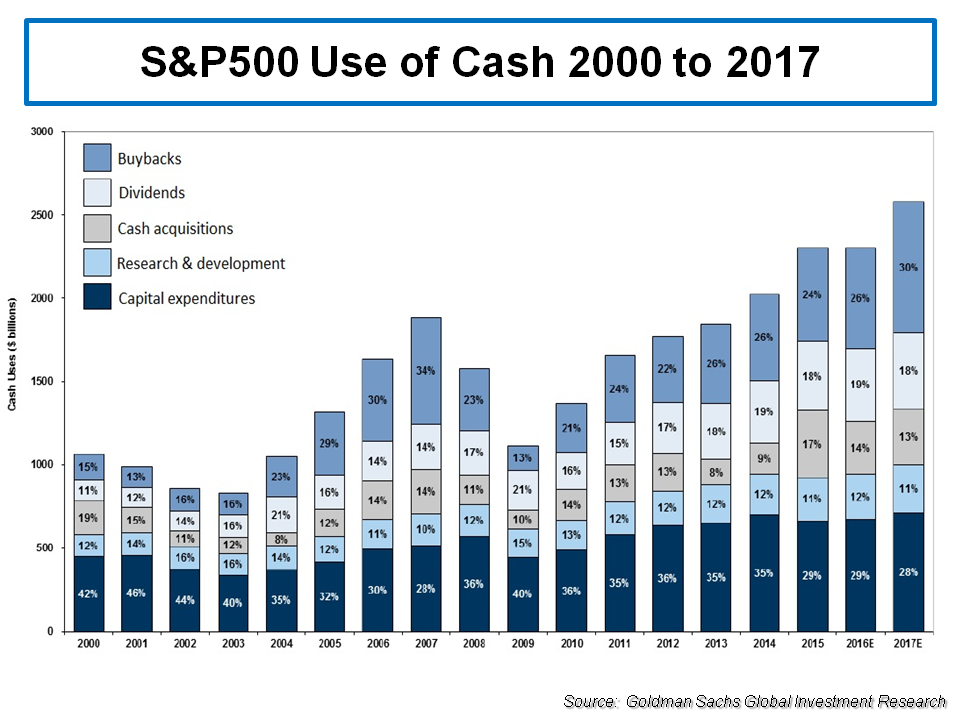

Bulls further point to strong earnings growth in 2017 complemented by economic stimulus and corporate tax giveaways under President Trump. Goldman Sachs expects corporations to repatriate approx $200 billion of overseas cash and to spend a lot of it buying back stock rather than making capital expenditures (see graph below) although the political pressure to invest in the US may impact the balance.

click to enlarge

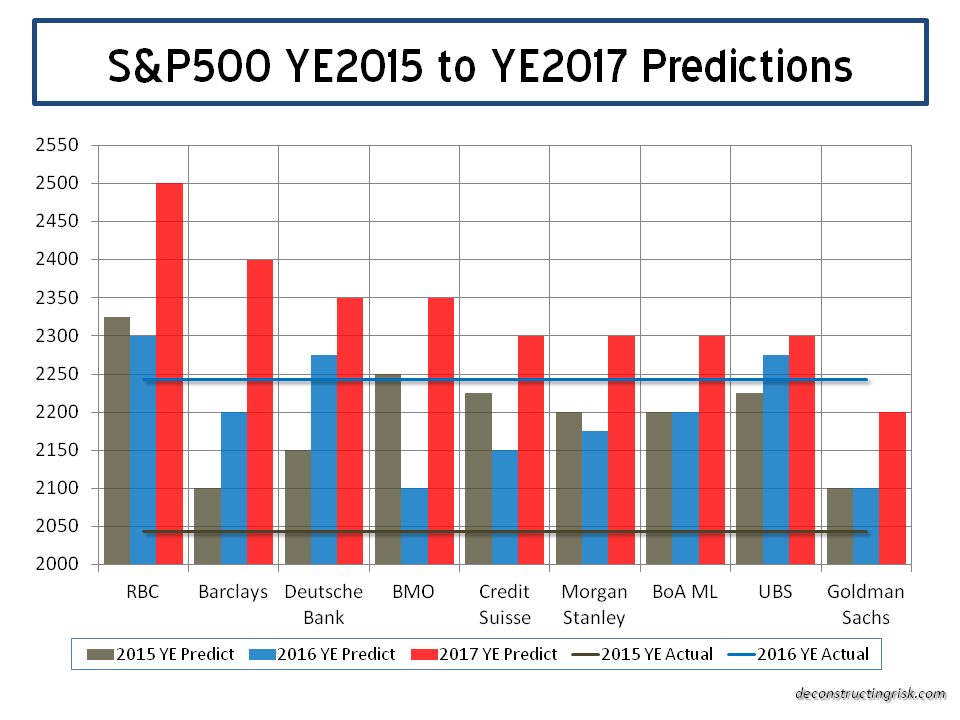

The consensus amongst analysts predict EPS growth in 2017 in the high single digits, with many highlighting further upside depending upon the extent of the corporate tax cuts that Trump can get past the Republican congress. Bulls argue that the resulting forward PE ratio for the S&P 500 of approx 17 only represents a 20% premium to the longer term average. Predictions for the S&P 500 for 2017 by a selection of analysts can be seen below (the prize for best 2016 prediction goes to Deutsche Bank and UBS). It is interesting that the average prediction is for a 4% rise in the S&P500 by YE 2017, hardly a stellar year given their EPS growth projections!

click to enlarge

My best guess is that the market optimism resulting from Trump’s victory continues into 2017 until such time as the realities of governing and the limitations of Trump’s brusque approach becomes apparent. Volatility is likely to be ever present and actual earnings growth will be key to the market story in 2017 and maintaining high valuation multiples. After all, a low or high PE ratio doesn’t mean much if the earnings outlook weakens; they simply indicate how far the market could fall!

Absent any significant event in the early days of Trump’s presidency (eh, hello, Mr Trump’s skeleton cupboard), the investing adage about going away in May sounds like a potentially pertinent one today. Initial indications of Trump’s reign, based upon his cabinet selections, indicate sensible enough domestic economy policies (relatively) compared with an erratic foreign policy agenda. I suspect Trump first big foreign climb down will come at the hands of the Chinese, although his bromance with Putin also looks doomed to failure.

How Brexit develops in 2017 looks to be much more worrying prospect. After watching her actions carefully, I am fast coming to the conclusion that Theresa May is clueless about how to minimise the financial damage from Brexit. Article 50 will be triggered in early 2017 and a hard Brexit now seems inevitable, absent a political shock in Europe which results in an existential threat to the EU and/or the Euro.

The economic realities of Brexit will only become apparent to the UK and its people, in my view, after Article 50 is triggered and chunks of industry begin the slow process of moving substantial parts of their operation to the continent. This post illustrates the point in relation to London’s insurance market. The sugar high provided by the sterling devaluation after Brexit is fading and the real challenge of extracting the UK from the institutions of the EU are becoming ever apparent.

Prime Minister May should be leading her people by arguing for the need for a sensible transition period to ensure a Brexit logistical tangle resulting in unnecessary economic damage is avoided. Instead, she acts like a rabbit stuck in the headlights. Political turmoil seems inevitable as the year develops given the current state of the UK’s fractured political system and lack of sensible leadership. The failure of a coherent pro-Europe political alternative to emerge in the UK following the Brexit vote, as speculated upon in this post, is increasingly looking like a tragedy for the UK.

Of course, Trump and Brexit are not the only issues facing the world in 2017. China, the Middle East, Russia, climate change, terrorism and cyber risks are just but a few of the issues that seem ever present in any end of year review and all will likely be listed as such in 12 months time. For me, further instability in Europe in 2017 is the most frightening potential addition to the list.

As one ages, it becoming increasingly understandable why people think their generation has the best icons. That said, the loss of genuine icons like Muhammad Ali and David Bowie (eh, sorry George Michael fans) does put the reality of the ageing (as highlighted in posts here and here) of the baby boomer generation in focus. On a personal note, 2016 will always be remembered by me for the loss of an icon in my life and emphasizes the need to appreciate the present including all of those we love.

So on that note, I’d like to wish all of my readers a prosperous, happy and healthy 2017. It looks like there will be plenty to write about in 2017…..

Not quite there but I wish you a happy new year 2017!

Will write more once I have a proper keyboard ;).

Best,

Eddie

Some random thoughts:

Europe: 2017 will be interesting. Some Italian banks are pretty much bust imo, the question is how to get around this nasty bail-in regime. What happens when the next bank goes belly up (not necessarily in Italy) will be interesting to watch. I expect the Euro to break up at some point, though. Either the internal devaluation in Southern Europe (combined with high levels of unemployment) continues for a long time and the politicians finally get their act together or the Germany transfer significant amounts of money (similar to what they did and still do to rebuild East Germany, just way more). Both seems unlikely to me.

Stocks: Jeremy Siegel pulls off his usual trick, comparing profits of all companies with the market cap of the listed ones. If he offers me the non-listed part of the US economy for free I will be a happy taker. There are probably pockets of value but I wouldn’t buy an index tracker and expect 10% p.a. right now.

Overseas cash: Last time cash was repatriated if neither went into buybacks nor into CAPEX, only in execuite coffers and bonuses. But maybe it’s different this time. We shall see. Even if it goes into buybacks this will be a one-off (destroying shareholder value, so a good reason to sell).

Brexit: If Mrs. May wants to convey the impression that she has no real clue how to prcess she is spot on imo. Balancing unrealistic promises (GBP 350m each week for NHS…) with the likely future of years of negotiations (much longer than two years) and the need to compromise with the rest of the EU which seems to be determined to play hardball (or give the impression… I think both sides have a lot to loose if a hard Brexit happens) is probably the most difficult political task out there right now.

tks Eddie,

agree as always

Europe scares the heck out of me, the UK has yet to see political reality & post Art50 will be a lot of fun.

Beginning to think that this Trump rally may be as good as it gets for awhile…….

M