How many investment bankers does it take to change a lightbulb? Well there are numerous jokes on that. Here’s one: two – one to take out the bulb and drop it and another one to sell it before it crashes!

In the case of the Level 3 (LVLT) and Centurylink (CTL) proposed merger (see previous post), it took no less than five investment banking firms according to the recent S4 filing to get a deal agreed. Centurylink had Bank of America Merrill Lynch and Morgan Stanley as its main advisors with Evercore added for another fairness opinion. Level 3 had Citi as its main advisor with Lazard for another fairness opinion.

The S4 also reveals that there was no auction process. Although both sides have no doubt talked to many potential partners about deals (both telecom firms have extensive M&A experience) in the recent past, this merger proposal really got started after discussions with the CEOs in May, initially about a LVLT purchase of CTL’s business segment and a tracking stock on the consumer business. The tracking stock idea quickly got dumped with the cash and share purchase of LVLT by CTL discussed in principle in September with the details agreed in October. Given the breakup fee is only around $2 a share for any alternative bidder, LVLT decided it was best to nail down the deal with CenturyLink rather than look for other deals. The S4 stated the following:

In light of the premium being proposed by CenturyLink, Level 3 management’s view of the relatively low likelihood of any potential alternate bidder being willing to make a superior proposal within a short time frame and the risk of potential leaks raised by pursuing such a pre-signing market check, coupled with the ability of any potential interested bidder to submit a competing offer following the signing of a definitive agreement with CenturyLink and the ability of Level 3 to terminate any definitive agreement with CenturyLink post-signing to accept a superior proposal from another bidder, the Level 3 Board determined at that time to continue pursuing the transaction proposed by CenturyLink without approaching other parties.

Relying on investment bankers to give fairness opinions could be viewed with scepticism by anybody with a memory and a sense of humour. However, in this case, I believe that the strategy is a sensible one for shareholders. The business segment of CTL and LVLT clearly makes sense as a match up with the possibility of significant synergies (more I think than has been assumed). The consumer side of the merged entity can always be offloaded at an opportune time in the future. Also, any other potential bidders of LVLT, such as Comcast or a technology firm like Goggle or Microsoft, will be forced now to act if they want the unique assets of the firm. My sense is that the possibility of another bidder emerging over the coming months remains low.

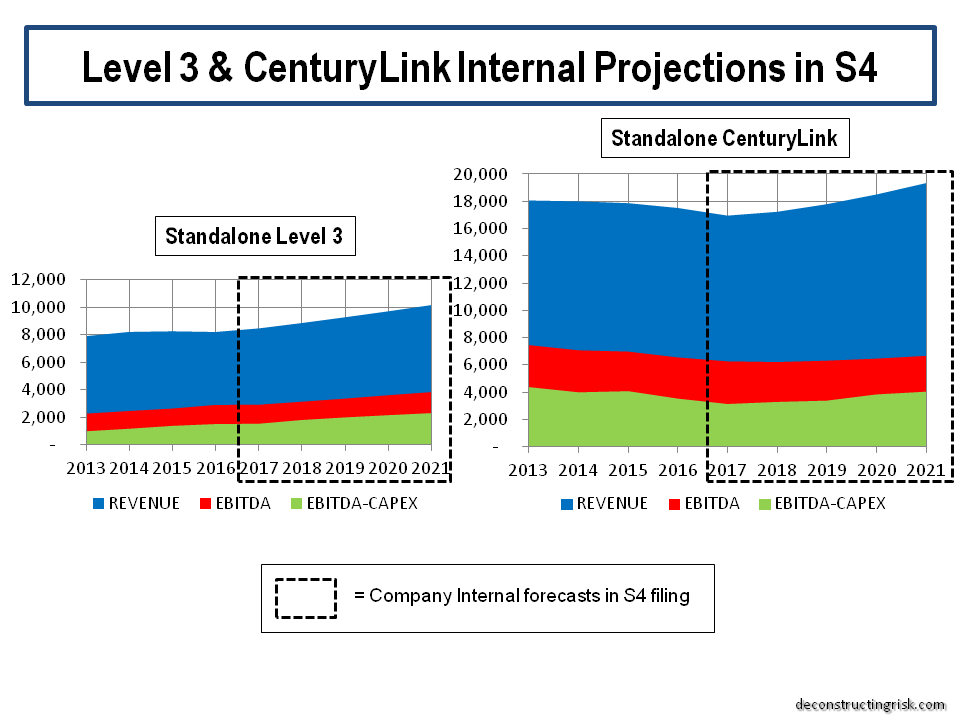

The financial projections, shown below, from management of each firm on a standalone basis are presented in the S4 and make for interesting reading.

click to enlarge

The projections for LVLT show higher capex figures for 2016 and 2017 than analyst estimates. From 2017 onwards, LVLT’s estimates of revenue are higher than analyst estimates whilst the resulting EBITDA is lower. This suggests a slower progression in EBITDA margins than analysts’ expectations with a figure closer to 35% and stable over the medium term. For CTL, the longer term revenue growth figures from the firm are more aggressive than analysts with EBITDA margins drifting down to the 35% level and below over the medium term.

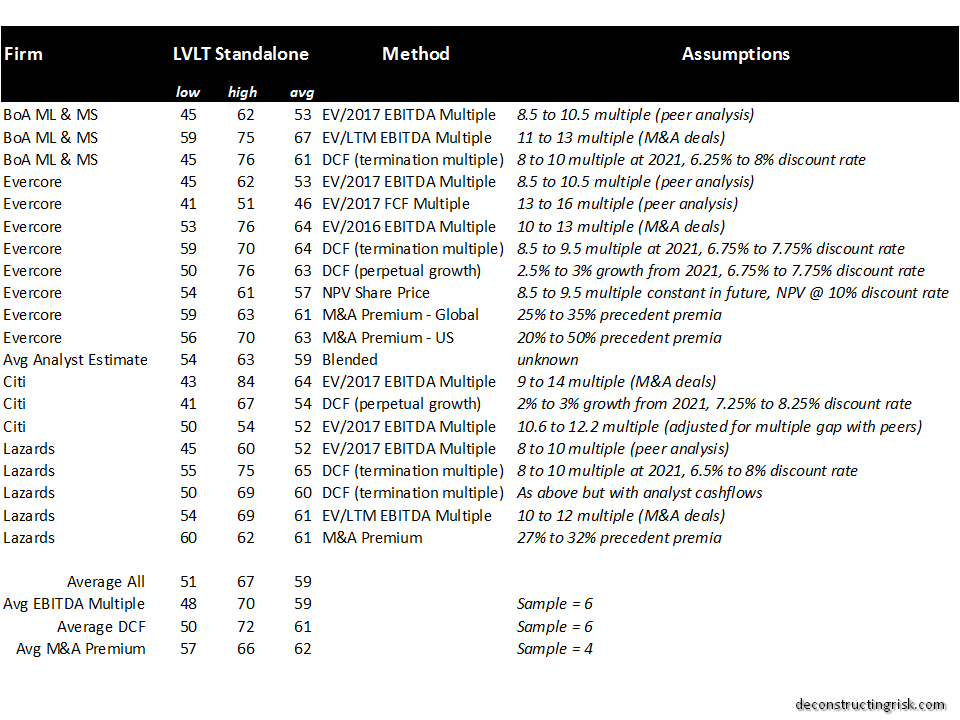

It is unclear how many adjustments have been made by advisors to the figures provided by management of both firms. I am not that familiar with CTL’s figures but the LVLT figures look reasonable enough. The fairness opinions generally state that they reviewed the figures provided and the assumptions behind them without actually coming up with their own figures. The valuations of a standalone LVLT in an M&A context, and the assumptions behind the methods used, outlined in the S4 are shown below.

click to enlarge

The valuations are generally consistent around a $60 per share level, varying from $50 to $70. Most include the value of the NOLs with Citi estimating their value separately at approximately $7 per share. A number of the bankers also valued the targeted synergies of the deal assuming 100% of these were assigned to LVLT shareholders. These estimates and the valuations of a standalone CTL are shown below.

click to enlarge

Comparing the average LVLT standalone valuations and those including the synergies shows a value of $25 per share (i.e. $84-$59), assuming shareholders get 100% of the synergies. That assumption is clearly unrealistic. If 50% of the synergies were assigned to LVLT shareholders (who will get 49% of the combined entity), than a reasonable expectation in the longer run would be a value equivalent to $72 per share. As can be seen below, this is equivalent to a share price of $32 per share for CTL under the merger terms. BofA Merrill Lynch and Morgan Stanley in the S4 calculated a proforma value of CTL after the merger (with the synergies realised) of $34.75 which would put the value of the deal to LVLT shareholders around $76 per share, as below.

click to enlarge

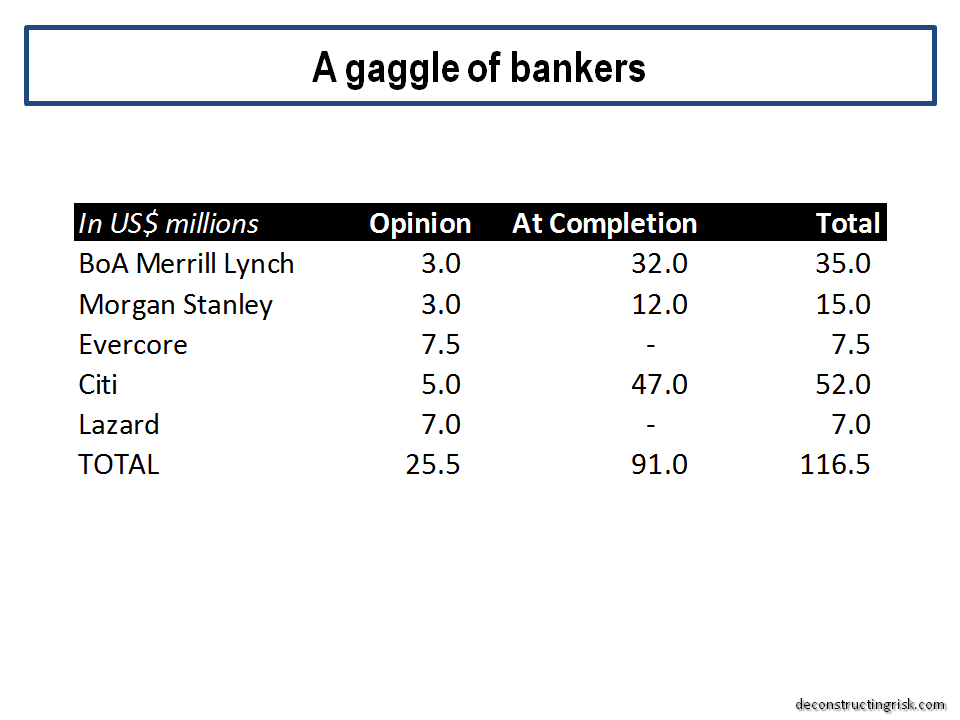

With CTL’s stock still trading just over $24, there is obviously a lot that can happen before this proposed merger closes. And even more time before the deal synergies are realised. One thing is for sure through, the investment bankers are making out well as the exhibit on their fees below shows. $25 million alone for a few week’s work to provide the fairness opinions is outrageous.

click to enlarge

The amount of such fees investment bankers get away with charging always boggles the mind and shows what a closed shop the business still is. Whatever happens to LVLT and CTL shareholders, these masters of the universe always make out like bandits.

Completly unrelated… I wish you happy holidays and a happy new year!

All the best,

Eddie

Thanks Eddie and a big happy Christmas to you and yours.

Here’s to an eventful 2017!

All the best

🙂