In a previous post, I reproduced an exhibit from a report from Aon Benfield on the potential areas of disruption to extract expenses across the value chain in the non-life insurance sector, specifically the US P&C sector. The exhibit is again reproduced below.

click to enlarge

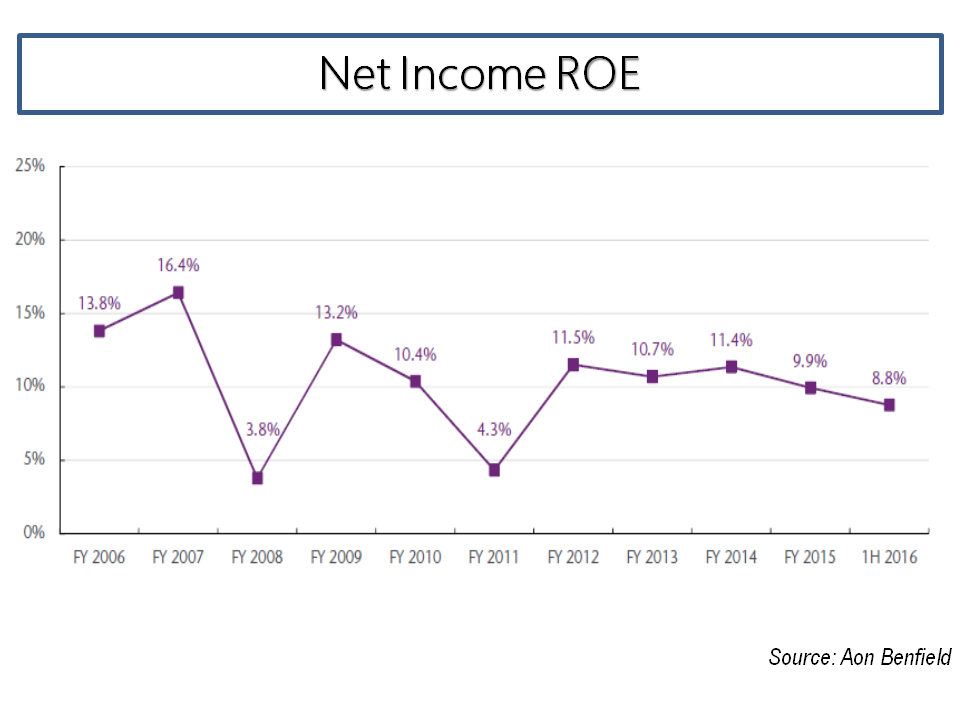

The diminishing returns in the reinsurance and specialty insurance sector are well known due to too much capital chasing low risk premia. Another recent report from Aon Benfield shows the sector trend in net income ROE from their market representative portfolio of reinsurance and specialty insurers, as below.

click to enlarge

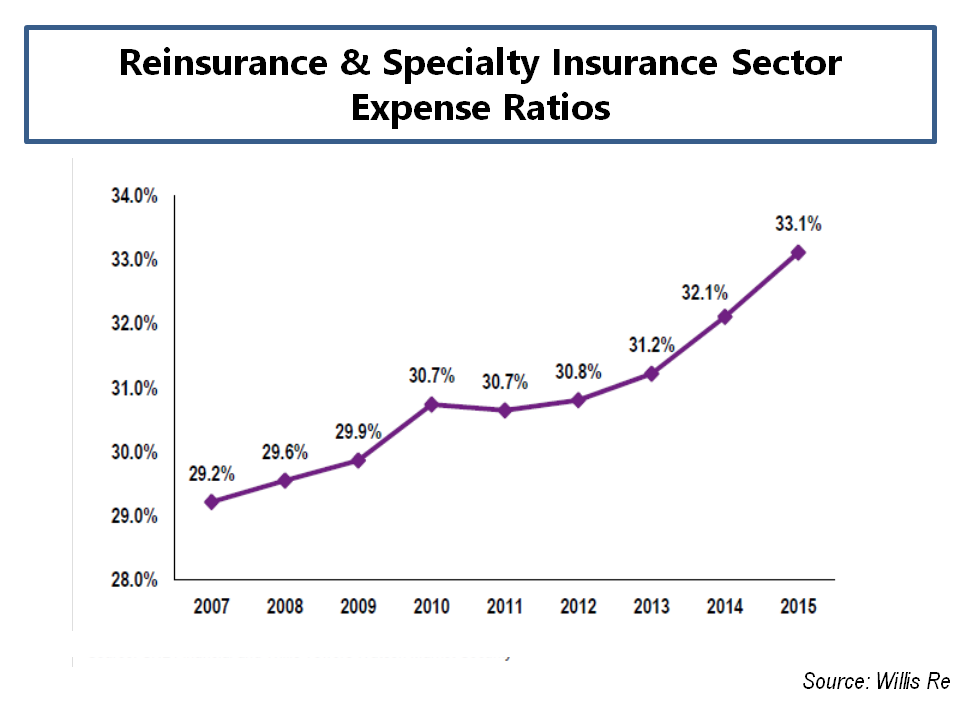

It’s odd then in this competitive environment that the expense ratios in the sector are actually increasing. Expense ratios (weighted average) from the Willis Re sector representative portfolio, as below and in this report, illustrate the point.

click to enlarge

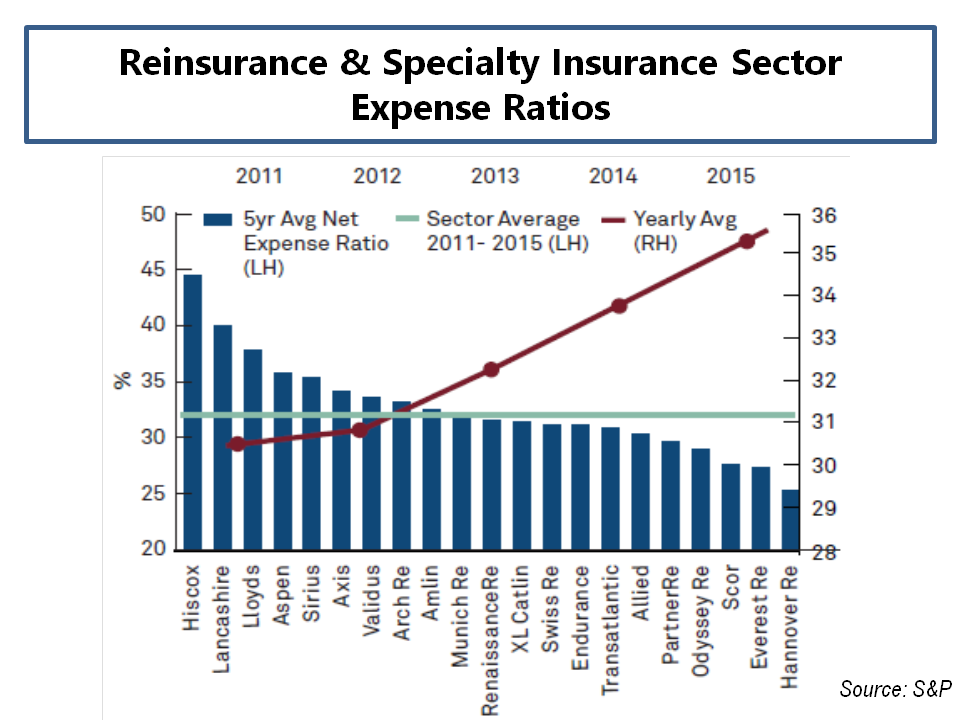

The 2016 edition of the every interesting S&P Reinsurance Highlights, as per this link, also shows a similar trend in expense ratios as well as showing the variance in ratios across different firms, as below.

click to enlarge

Care does need to be taken in comparing expense ratios as different expense items can be included in the ratios, some limit overhead expenses to underwriting whilst others include a variety of corporate expense items. One thing is clear however and that’s that firms based in the London market, particularly Lloyds’, are amongst the most top heavy in the industry. Albeit a limited sample, the graph below shows the extent of the difference of Lloyds’ and some of its peers in Bermuda and Europe.

click to enlarge

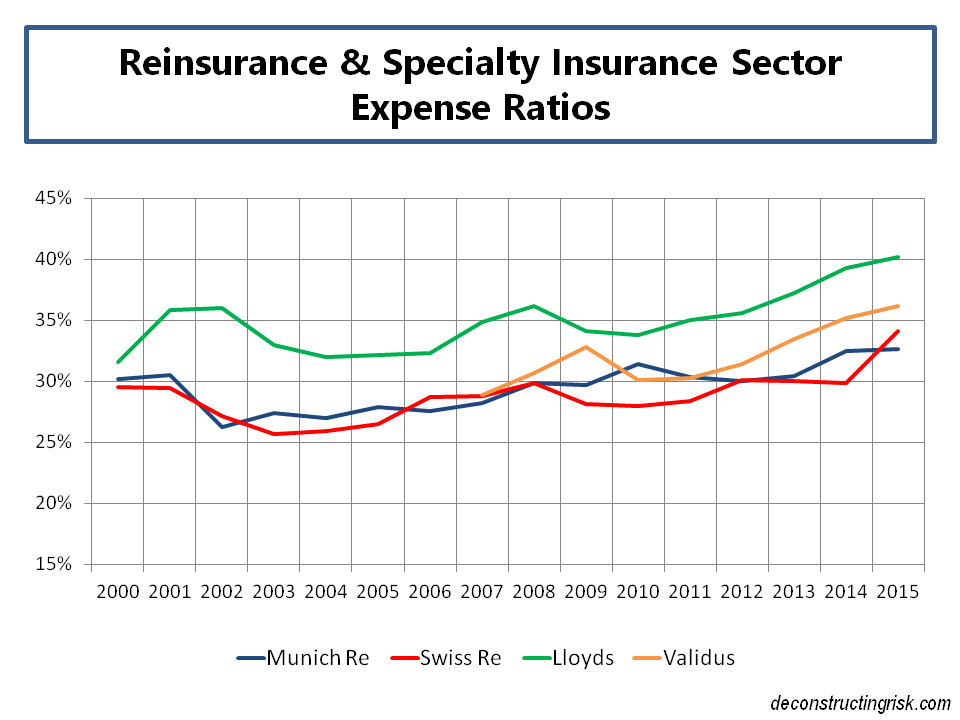

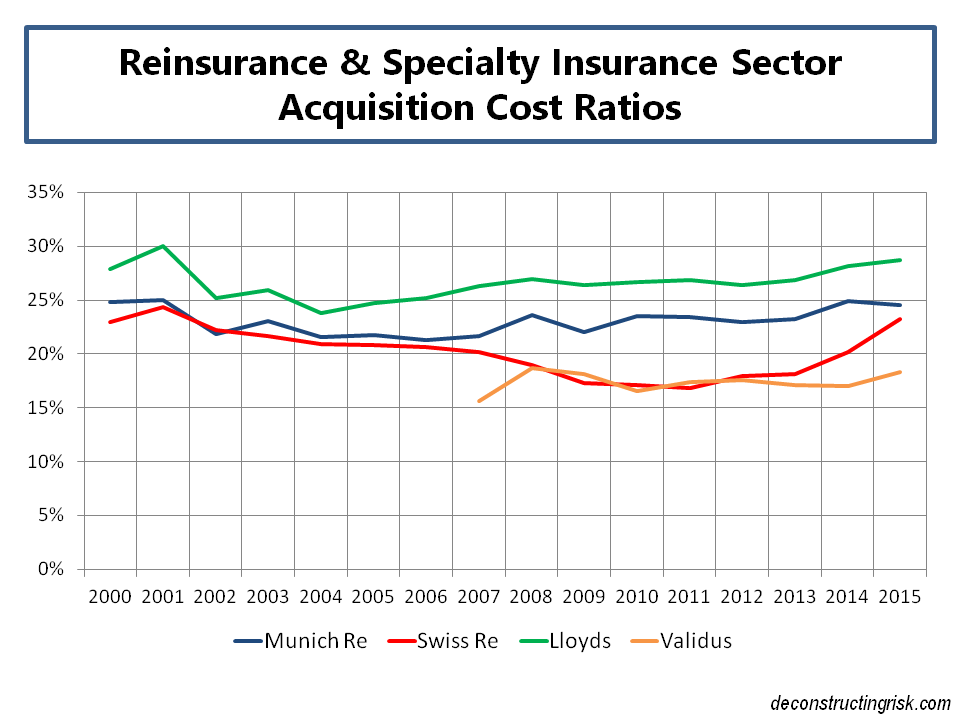

Digging further into expense ratios leads naturally to acquisitions costs such as commission and brokerage. Acquisition costs vary across business lines and between reinsurance and insurance so business mix is important. The graph below on acquisition costs again shows Lloyds’ higher than some of its peers.

click to enlarge

Although Brexit may only result in the loss of fewer than 10% of London’s business, any loss of diversification in this competitive market can impact the relevance of London as an important marketplace. Taken together with the gratuitous expense of doing business in London, its relevance may come under real pressure in the years to come. London is, most definitely, not calling.

Which brings up the next question: “Should I stay or should I go?” 🙂

…straight to hell or safe European home…. we shall see.

Hope all good with u eddie, where did the year go..

M

You tell me… weeks are just flying by right now and the year… well… it seems quite long in retrospective, but still time passed quickly,

Everything is fine so far, thanks for asking. Currently wrapping a few things up and preparing myself for Christmas.

Best,

Eddie