Anybody who has young kids at school knows the incredible impact that the internet is having upon modern education. My kids love Reading Eggs, a spelling game by a company called Edmentum. Others rave about Edmodo, a free online platform for teachers and students with over 17 million users worldwide.

The digitalization of education content and the multitude of new online learning platforms are resulting in a substantive change in the education of our kids. A recent study of online learning found that, on average, students performed better than those receiving face-to-face instruction. Technology also offers an array of tools for teachers to monitor student’s learning and to highlight specific issues with students. John Fallon, the CEO of Pearson Plc, believes online learning is a “once-in-a-generation opportunity” and could be “one of the great growth industries of the future”.

Coupled with my kids’ interest in the latest learning game (when they are not playing Minecraft!), the re-emergence of a company called Houghton Mifflin Harcourt (HMHC) from bankruptcy in 2012 and its return onto the stock market in November 2013 has caught my attention. The rise and fall of HMHC over the past decade, a leading provider to the kindergarten through twelfth grade (called the K-12 market) educational sector in the US, is a fascinating case study on the effect of the financial crisis coupled with the disintermediating impact of technology.

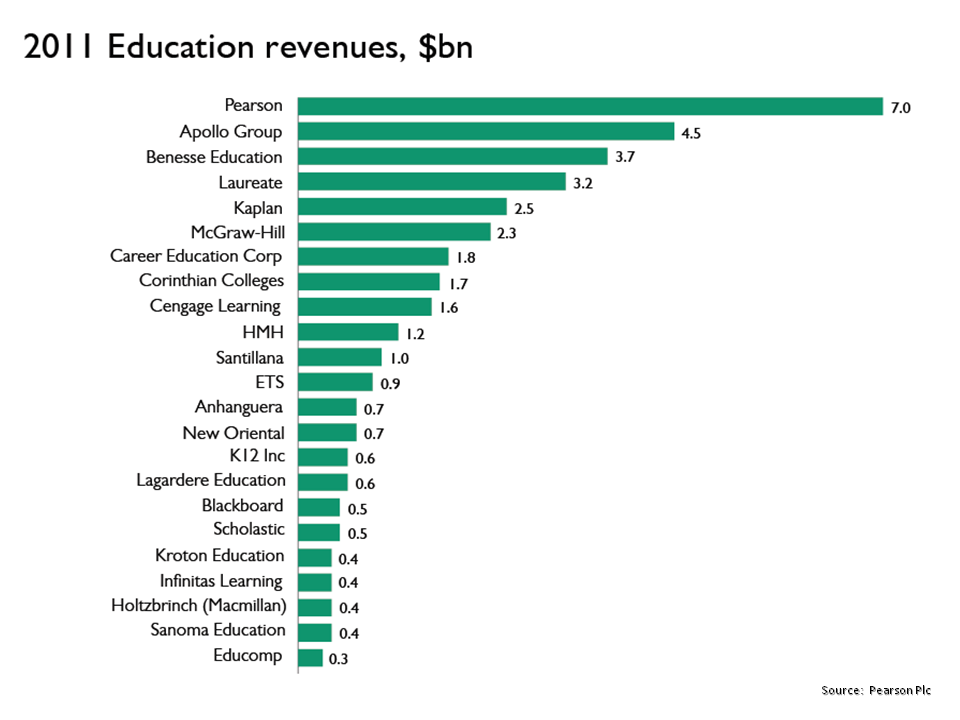

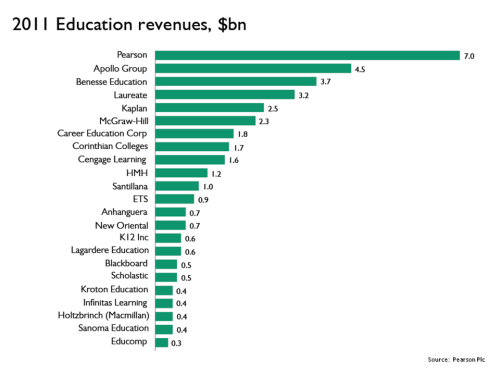

Before looking through HMHC’s past the exhibit below outlines the market leaders in the education sector according to a presentation from Pearson Plc.

click to enlarge

The firms above are from a cross section of the industry, some focus on adult education, others on universities, whilst others on the K-12 market. The main firms in the K-12 sector are Pearson Education, McGraw Hill Education, HMHC, Cengage Learning, Scholastic Corporation and K12 Inc.

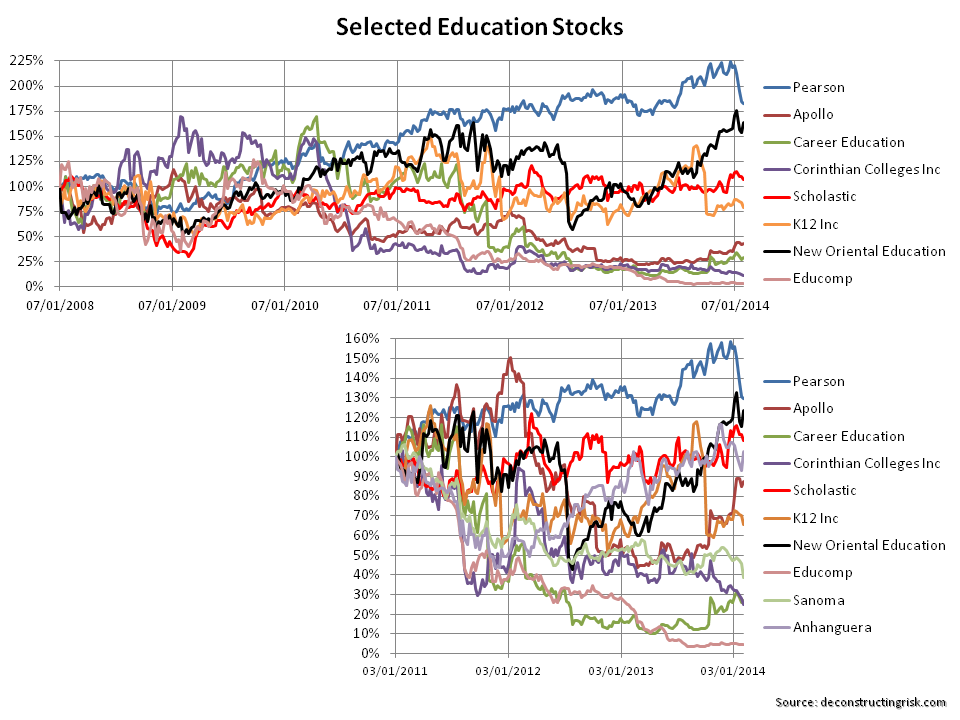

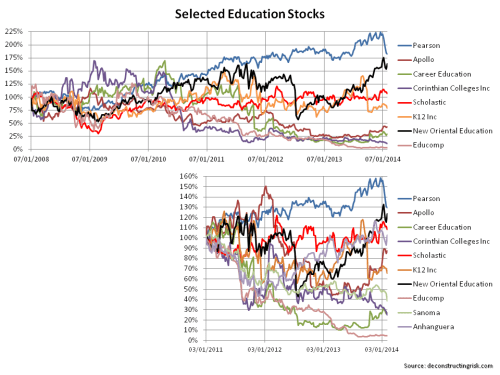

The educational textbook market has been struggling with declining sales. Cengage Learning filed for Chapter 11 bankruptcy last year and the private equity firm Apollo are known to be looking for an exit from its purchase of McGraw-Hill Education in 2012. The graphic below shows the share history of a number of the firms (from 2008 for many and from 2011 for a larger sample).

click to enlarge

As can be seen, the experience has been decidedly mixed with only Pearson achieving an acceptable long term performance (although it was hit recently by a profits warning in January due to poor US sales, particularly in the career college sector).

Houghton Mifflin has a long history in publishing going back to the 19th century. A public company since 1967, Houghton Mifflin was bought by Vivendi in 2001 for $2.2 billion and, following financial issues in Vivendi, resold in 2002 for $1.7 billion to a number of private equity firms. By 2005, Houghton Mifflin had revenues of $1.3 billion with an EBITDA margin of 23%.

Riverdeep was an Irish educational technology firm taken public in 2000 at the height of the internet boom by its then 30 year old CEO Barry O’Callaghan. O’Callaghan had a background in investment banking firms such as Credit Suisse where he had developed his deal-making and financial engineering skills. He took Riverdeep private after the internet crash and by 2005 Riverdeep had revenues of $140 million and an EBITDA margin around 50%.

In 2006, O’Callaghan orchestrated an audacious merger of Houghton Mifflin and Riverdeep, an old and a new firm in educational content. The deal involved $600 million of new equity with the merged entity leveraged with $3.5 billion of debt. In the deal, Houghton Mifflin was valued at 10 times 2006 forecasted EBITDA whilst Riverdeep got a 13 times multiple. The investment case for the deal was to use Riverdeep’s technological experience to drive new revenue opportunities for Houghton Mifflin’s content whilst cutting costs through supply chain optimization and outsourcing. Barely within a year of the deal, the merged Houghton Mifflin Riverdeep again went on the M&A trail. This time it purchased Harcourt Education, another significant player in the K-12 market, for $4 billion. The idea was to resell on a number of non-core units of the combined entity such as the College division (sold to Cengage Learning for $750 million) and Harcourt Religion Publishing to focus on the K-12 market.

The new company, which operated under the name Houghton Mifflin Harcourt, looked at quickly taking out the targeted $250 million of annual costs froml the combined entities (for example, printing was outsourced) and focusing on leveraging existing content in an online learning environment. Houghton Mifflin Harcourt increased market share and performed well in the first half of 2008 before the financial crisis started to take hold. For the full 2008 year, revenue was $2 billion down approx 5% from the 2007 proforma figures but, due to the impact of cost savings, EBITDA grew substantially to over $700 million and an impressive EBITDA margin of over 35%. The firm remained highly leveraged with debt of over $6.25 billion or over 8 times as at the end of 2008. The new Houghton Mifflin Harcourt was heading into a storm, the like of which had never been seen before in the sector.

The impact of the financial crisis wreaked havoc on the firm’s business as local State finances resulted in a sharp rise in postponed and deferred sales. Education textbook and material purchases are seasonal with particular liquidity strains on the business in Q1 and Q4. By mid-2009, the company announced a debt restructuring to reduce debt by over $1 billion. However, trading conditions continued to deteriorate in H2 2009 and the full year recorded a 25% reduction of revenue and a reduction in EBITDA of over 30%. Houghton Mifflin Harcourt ended 2009 with an estimated debt to EBITDA ratio of over 13 which was clearly unsustainable. A question mark loomed over it’s future.

In early 2010, a recapitalization involving a debt for equity swap and new investment of $650 million was agreed which reduced the firm’s debt load to below $3 billion and wiped out the existing equity holders. Paulson & Co and Guggenheim Partners were amongst the new owners. Astonishingly, Barry O’Callaghan kept his job as CEO after the recapitalization.

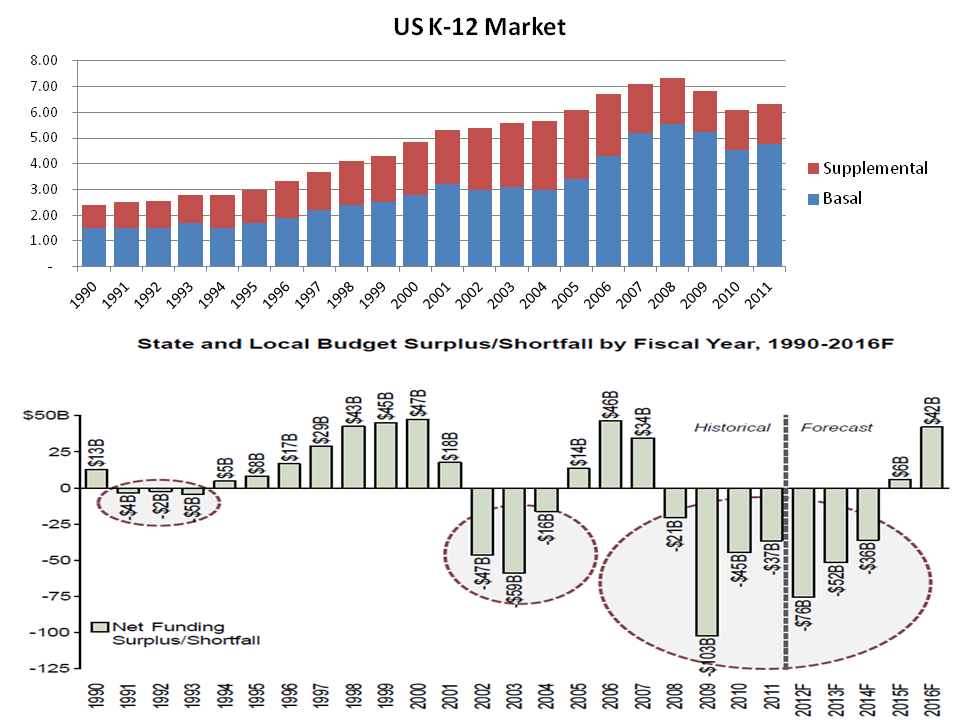

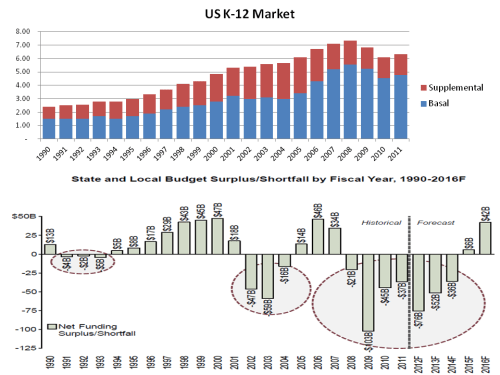

In the US, educational products are split into 2 categories – basal and supplemental. Basal materials are complete materials for students and teachers covering comprehensive courses. Supplemental materials speak for themselves. Approximately half of the States in the US follow a State wide adoption of basal materials by subject, usually ever 3 to 5 years (and are called “Adoption States”). The others allow districts to select their own course materials and are called “Open States”. Important adoption States in the K-12 market include the largest – Florida, Texas and California.

Unfortunately for Houghton Mifflin Harcourt, the impact of the financial crisis on education budgets was not yet over, as an exhibit below on State finances from a presentation by the Partheneon Group compared to basal and supplemental sales illustrates.

click to enlarge

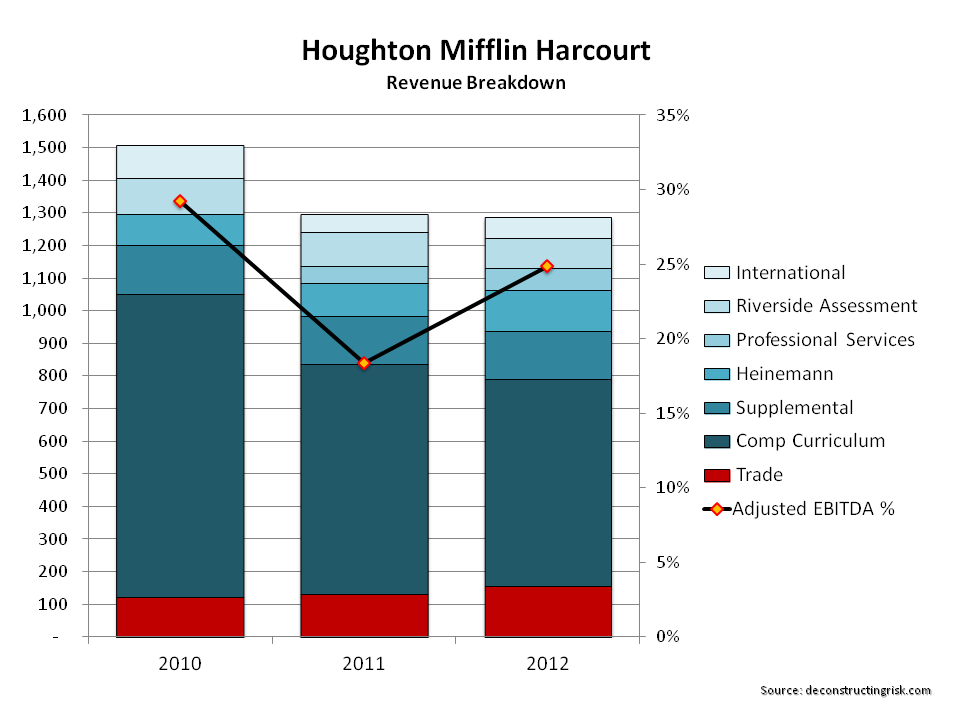

Houghton Mifflin Harcourt classifies their education products are follows:

- Comprehensive Curriculum which are materials for a complete study course, either at single of multi grade level and include subjects like reading, literature/language arts, mathematics, science, world languages and social studies.

- Supplemental Products which are materials to assist learning through incremental instruction.

- Heinemann produces professional books and developmental resources aimed at empowering pre-K-12 teachers whilst also providing benchmarking assessment tools.

- Professional Services provide consulting services to assist school districts in increasing accountability & training services.

- Riverside Assessment products provide district and state level solutions including psychological and special needs testing to assess intellectual, cognitive and behavioral development.

- International products are educational solutions in high growth territories primarily in Asia, the Pacific, the Middle East, Latin America, the Caribbean and Africa.

HMHC’s other business is the traditional trade publishing business with recent titles such as The Hobbit and Life of Pi.

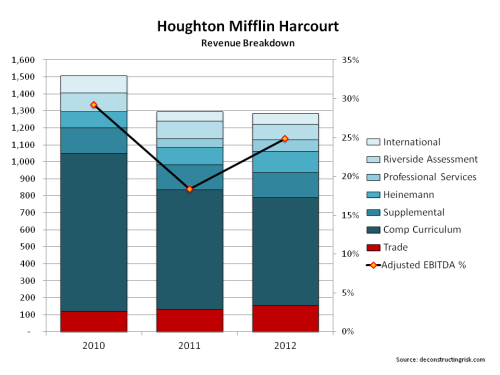

In 2011, Houghton Mifflin Harcourt was particularly impacted by a reduction in spending by Texas, one of the largest spending States, with revenues from Texas down from $190 million in 2010 to $70 million in 2011. The graphic below shows the business split by the above product classification for 2010 to 2012. The EBITDA margin is also shown (interestingly its averaging in the mid twenties at a level very similar to that achieved by the stand alone Houghton Mifflin in 2005!).

click to enlarge

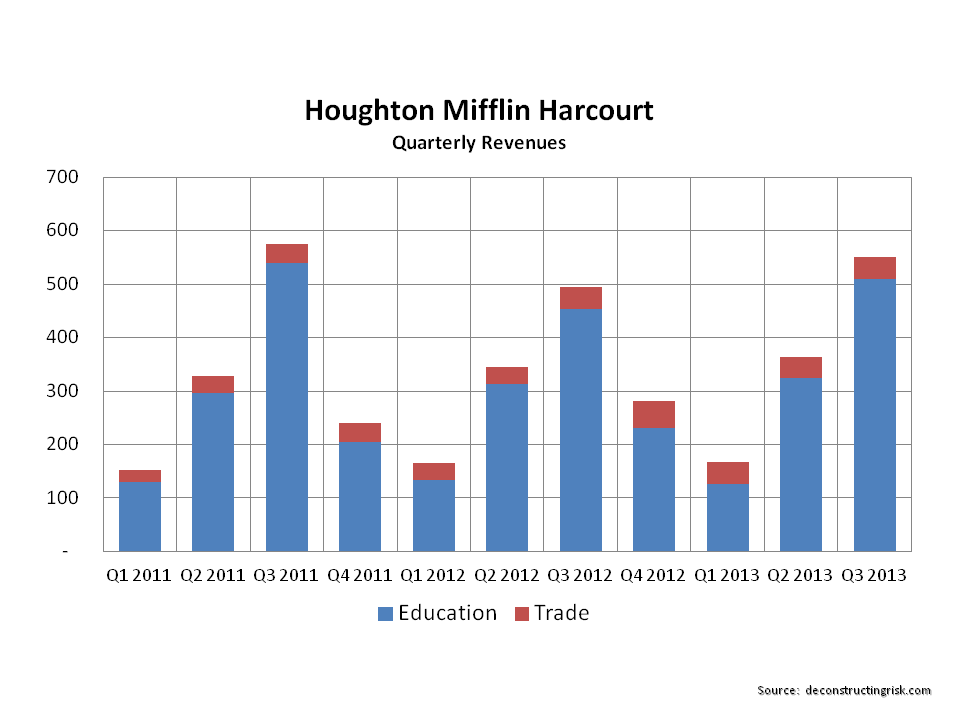

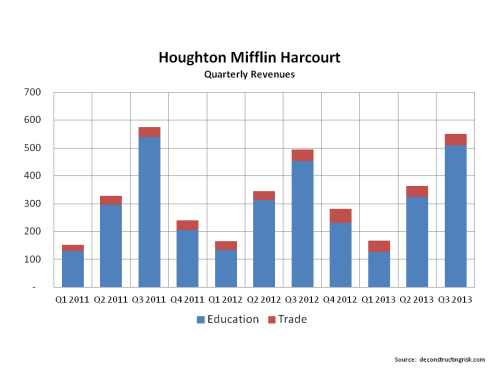

In September 2011, Linda Zecher took over as CEO from O’Callaghan who left the business. Zecher previously held leadership roles at Microsoft, Texas Instruments, and Peoplesoft. She has reorganised the executive suite, bringing in new expertise, many from Microsoft or with extensive technology backgrounds. In June 2012, Houghton Mifflin Harcourt emerged from voluntary bankruptcy under Chapter 11 with a cleaned up balance sheet with debt as at YE 2012 of less than $250 million and cash of over $450 million (cash balance is down to $230 million as at Q3 2012 with debt at the same level). Over the recent past, the business has been relatively steady if nothing spectacular. For FY2013, the business is likely to run at an operating breakeven, cashflow positive, with a EBITDA margin in the mid-20s. HMHC currently trades at an EV/EBITDA multiple of 7.5 which seems reasonable. They report their FY results in early March. The graphic below shows quarterly revenues since 2011.

click to enlarge

The company went public again in November 2013 under the ticker HMHC and points to its new found financial strength, its experience in digitalising its products, favourable demographics and the need for key States to adopt new programmes as catalysts. Florida, California and Texas are all scheduled to adopt educational materials for certain subjects between 2013 and 2016.

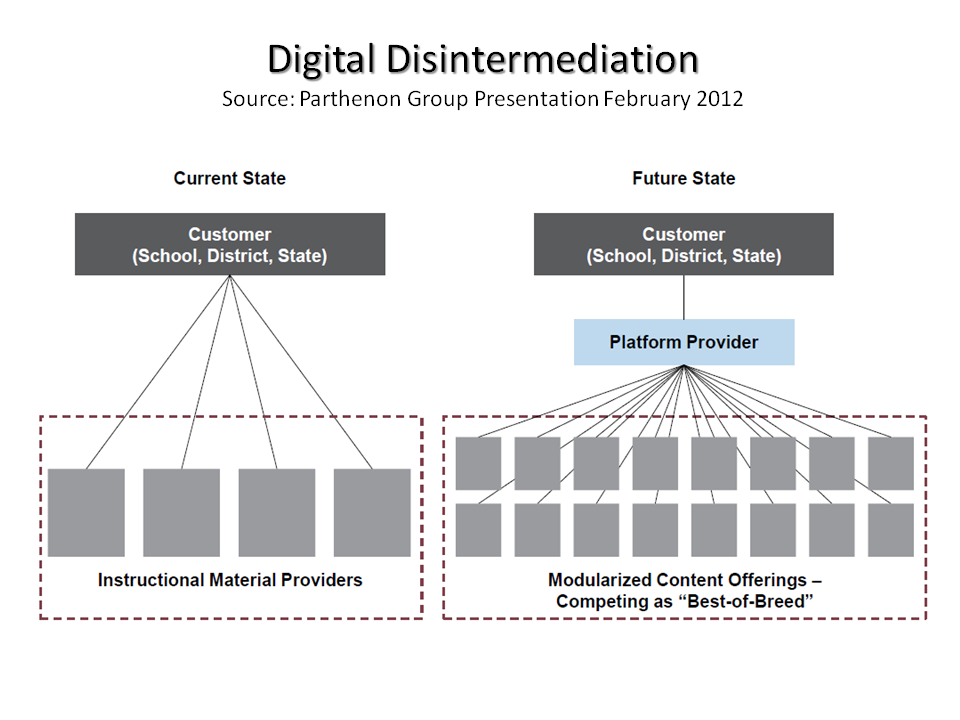

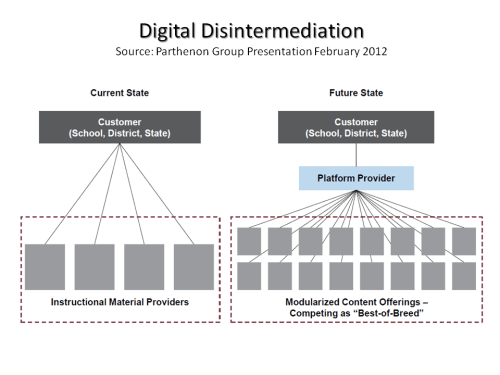

One important development that will determine the future success of firms such as HMHC is the newly developed Common Core State Standards agreed by State governors with implementation scheduled to begin in the 2014-2015 school year. Some, such as HMHC, argue that the long established firms with proven content and relationships will benefit the most from such standardisation. Others see these new standards as offering newer firms the opportunity to compete and innovate. The Partheneon Group, in the presentation referenced above, contend that digital disintermediation offers multiple content providers the opportunity to see their products if a common framework can be established, as the graphic below shows. Firms like Apple and Google are active in the education sector and would love to position themselves as such a platform.

click to enlarge

The future of companies such as HMHC may be uncertain but it will be interesting to observe how it plays out for them. Given HMHC’s recent experiences, I wish them well. Battle hardened now; they look in better shape than some of their old school competitors.

In some ways, you have to admire the vision of people like O’Callaghan for trying to pre-empt the future back in 2007. It is debatable whether the company would have survived with such an inflexible debt load in such a fast moving environment even without the financial crisis. To add the pressure of excessive leverage makes the task look foolhardy in retrospect.

click to enlarge

click to enlarge