In these weirdest of times, it is important to emphasis again Charlie Munger’s words of wisdom that “nobody knows what’s going to happen”. As developed countries across the world experiment with easing lock down measures, thoughts are moving to how economies can be re-opened. In what The Economist this week calls a 90% economy, they reflect upon a world where “the office is open but the pub is not”. A trite comment maybe but one that I think succinctly captures the new normal that those of us lucky enough to have our health can hope to be in for the next year.

Anyway, the point is that any projections in this environment are purely speculative. Add in my spotty record with AAPL, as this post in November attests to, and that AAPL have pulled guidance, highlights the likely futility of this post! Actually, I did dip my toe back in the water on AAPL around November after that post and when it shot up past $310 in January, I thanked the Gods and cashed out again (it went as high as $327 in February, daft!). The optimism about a new 5G iPhone super-cycle for next year that fed into that share price ramp has now been tempered by, well, the virus thing.

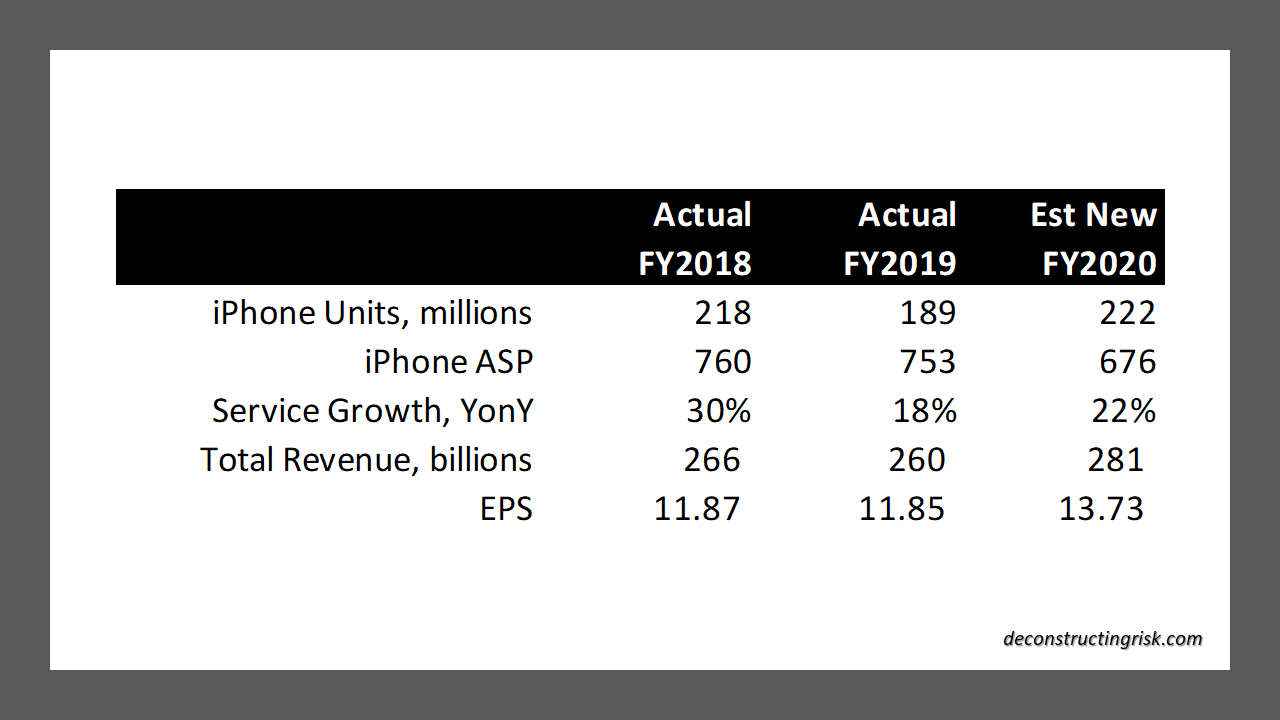

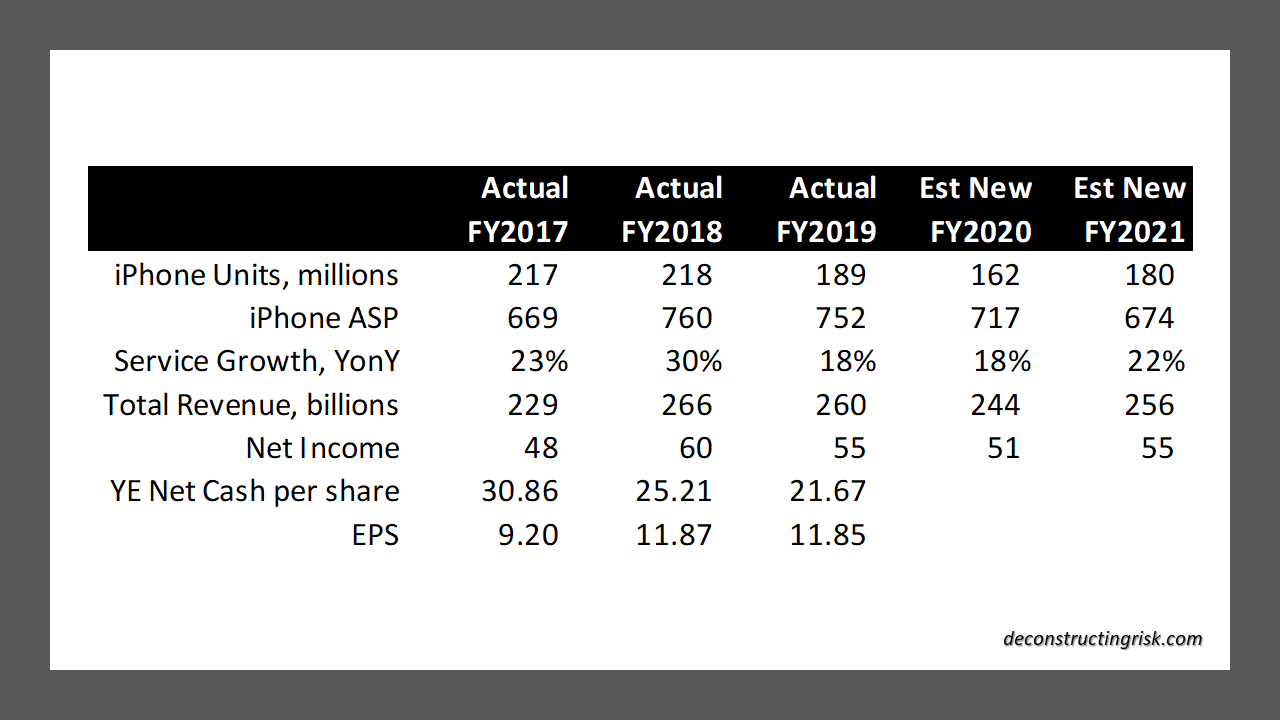

For my projections, I have assumed 26 million iPhone sales in the current quarter, down 27% on 2019, and 162 million for FY 2020, a 14% reduction from FY 2019. For FY 2021, I have assumed a pick-up in yearly unit iPhone sales due the launch of 5G iPhones, some in time for the holiday season, but at 180 units for FY 2021 it’s far short of the anticipated super-cycle refresh due to depressed consumer demand as the recession plays out next year. My assumptions are shown below:

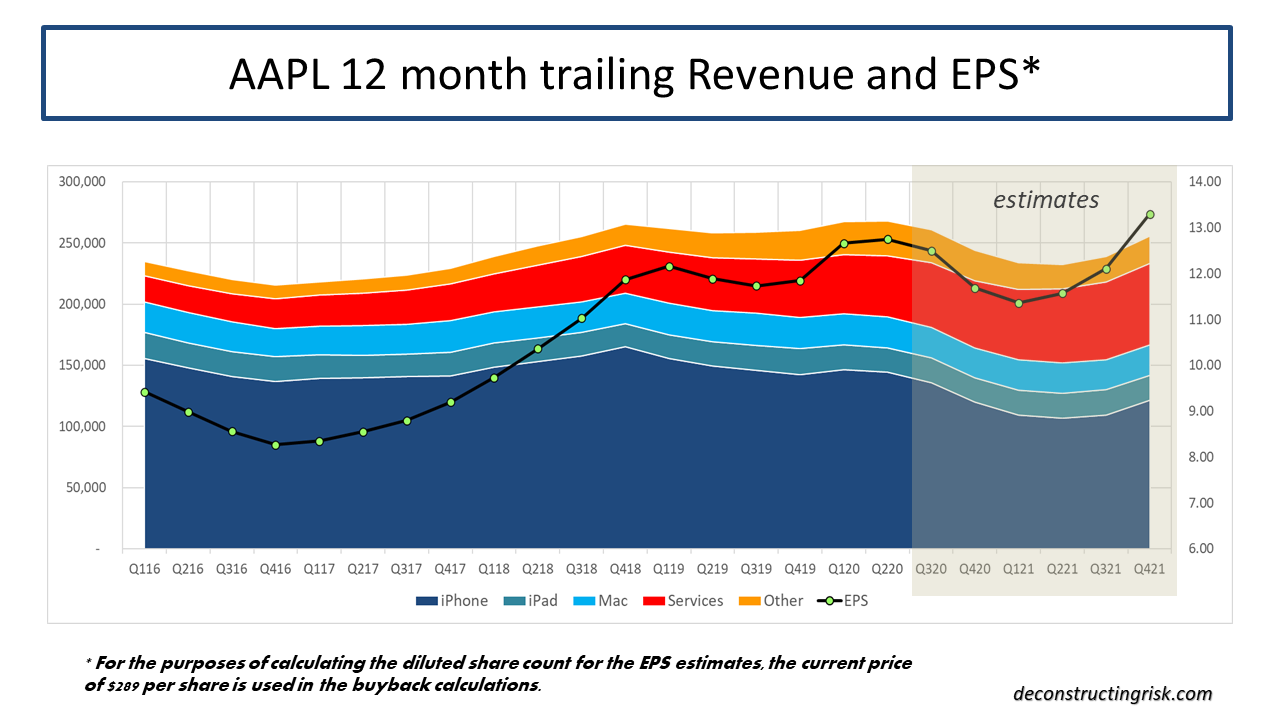

These assumptions are further illustrated in the trailing 12-month graph below.

Every great company needs an edge in the coming months and years to thrive. For AAPL, in addition to the quality of their products and their loyal installed base, their cash pile and their ability to manipulate share count through buy-backs has been a particular feature of their financial success in recent years, as the graph above clearly shows.

Although analysts were expecting a $75-100 billion increase in their buy-back programme in the Q2 quarter announcement last week, the announced $50 billion shows discipline and caution from management. I estimate that AAPL has spent approximately 130% of free cash-flow on dividends and buybacks in aggregate over the past 6 quarters, reducing their net cash balance by approximately $50 billion to $83 billion over those 6 quarters.

For the next 6 quarters to the end of FY 2021, I am assuming they return to shareholders, through both dividends and buy-backs, a similar amount of $126 billion to the previous 6 quarters, $105 billion through buy-backs alone. This shareholder return in terms of free cash-flow earned over the next 6 quarters would be an eye popping 200% according to my estimates. I further estimate a reduction in net cash on the balance sheet to approximately $40 billion by the end of FY 2021, an amount which I believe management, to be consistent with the firm’s DNA, should not feel comfortable going below for prudence sake (or to avail of further accretive M&A opportunities). One of the lessons of the COVID19 outbreak for well managed firms is surely the need for a contingency buffer against the unexpected. The resulting impact upon diluted share count and EPS of these assumptions at differing average buy-back share prices is shown below.

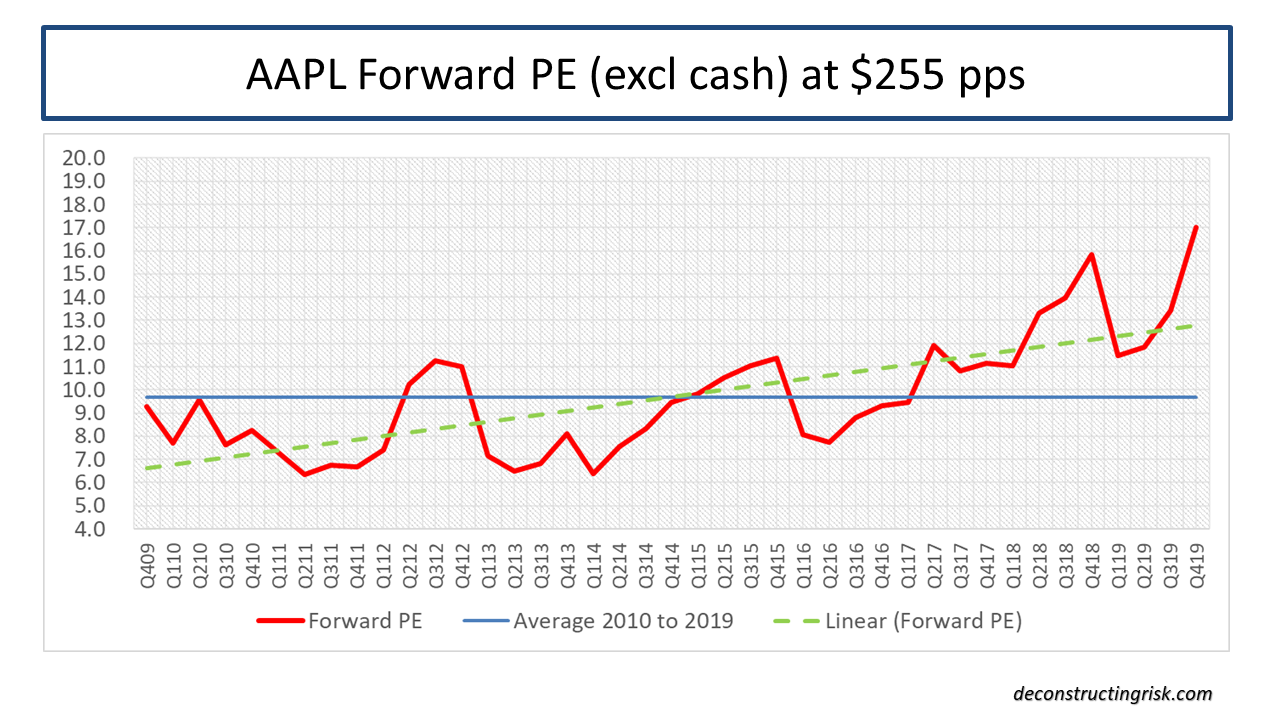

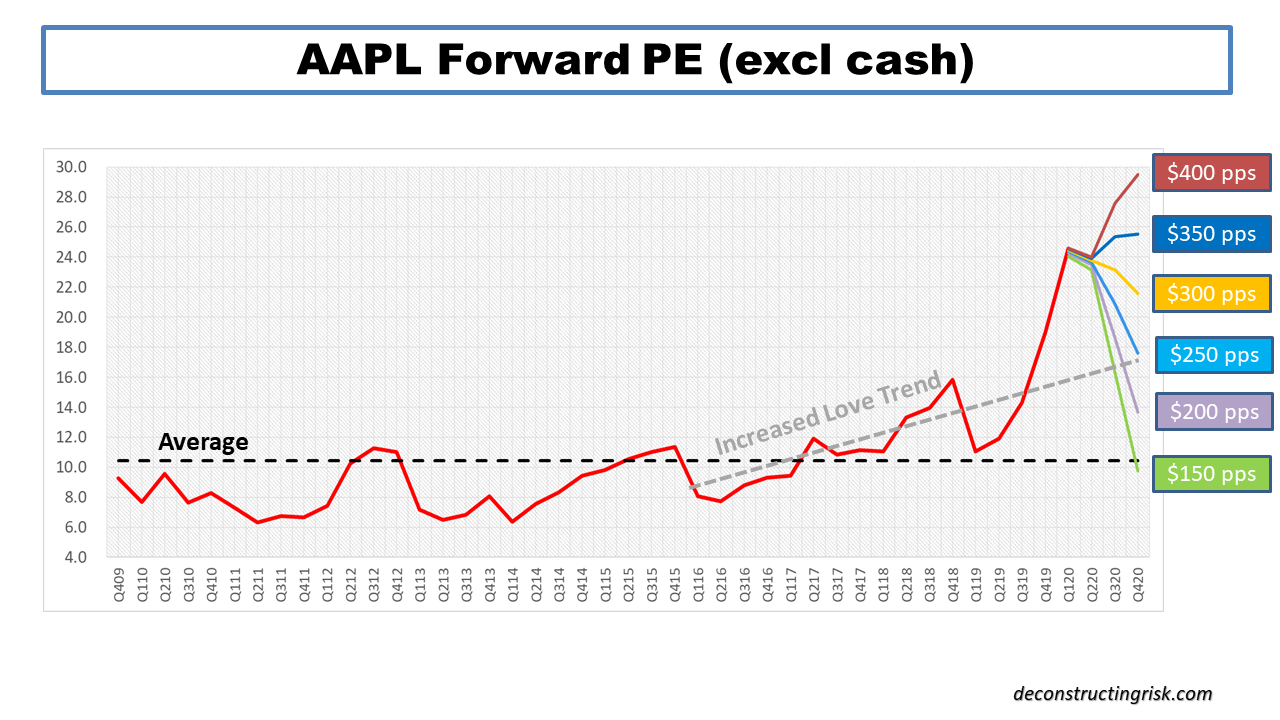

So, that just leaves the question of valuation. I will again warn that the subject matter in this post is based upon my assumptions which are highly speculative. I have proven myself to be hopelessly wrong in relation to AAPL at certain points in the past, so this time is unlikely to be any different! Using my preferred forward PE multiple excluding cash per share methodology, the graph below shows the forward multiples of my assumed performance over the next 6 quarters at share prices from $150 to $400, in increments of $50. The “increased love trend” is reflective of the higher multiple that AAPL has received as their service business has expanded and the hybrid hardware/software valuation has evolved.

Based upon this analysis, I would suggest that a share price below $250 should be considered as an entry point. Currently, I am uber bearish on equities and have exited 90%+ of my positions, taking advantage in recent weeks of this fairy tale rally (I mean, where is the upside from here?). Were AAPL to fall below $250, I would look closely at it again, albeit at a still heightened forward PE just below 18 based upon my estimates. Whether such an opportunity is afforded is anybody’s guess. As the man said, nobody knows.