The last time I posted on Paddy Power Betfair (PPB.L) in March, I highlighted the rich valuation and cautioned better value may be had on future dips, ending with the comment that “the game of speculation is all about getting the best odds”. Well, PPB.L has been on quite a ride in recent months. First the prospect of disappointing operating results put the stock under pressure and last week the bombshell that the golden boy CEO, Breon Corcoran, wants to do something more meaningful with his time. The result, as can be seen below, is PPB.L down 15% since the start of the year and 20% since this time last year.

click to enlarge

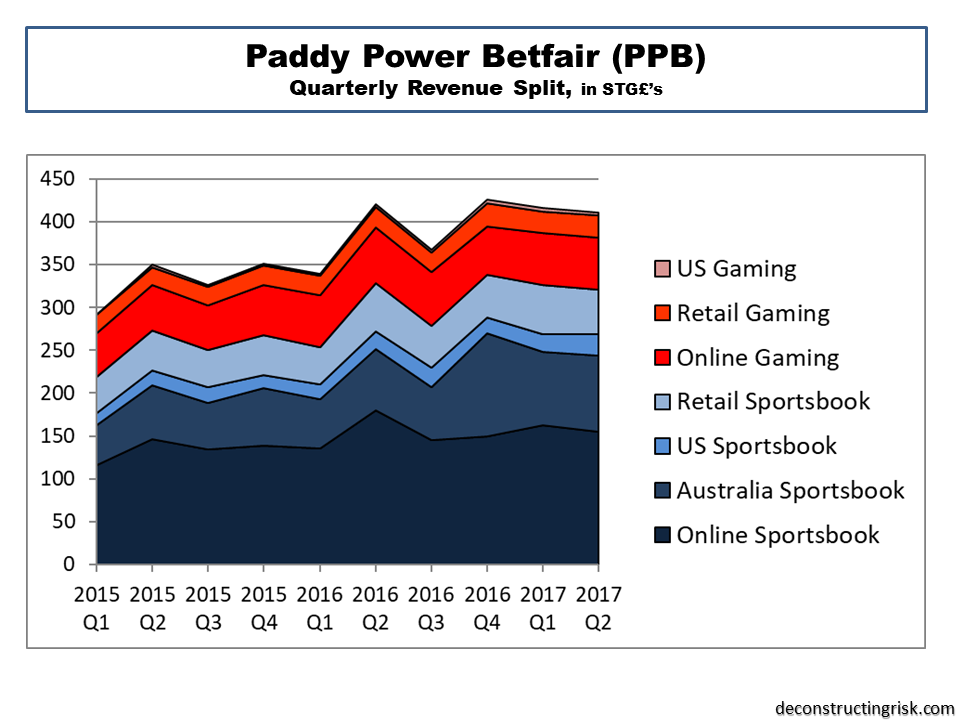

The revenue for the latest quarter, even after adjusting for the lack of the Euro soccer tournament in 2016, disappointed analysts who are fretting about whether reduced net revenue margins are part of a trend.

click to enlarge

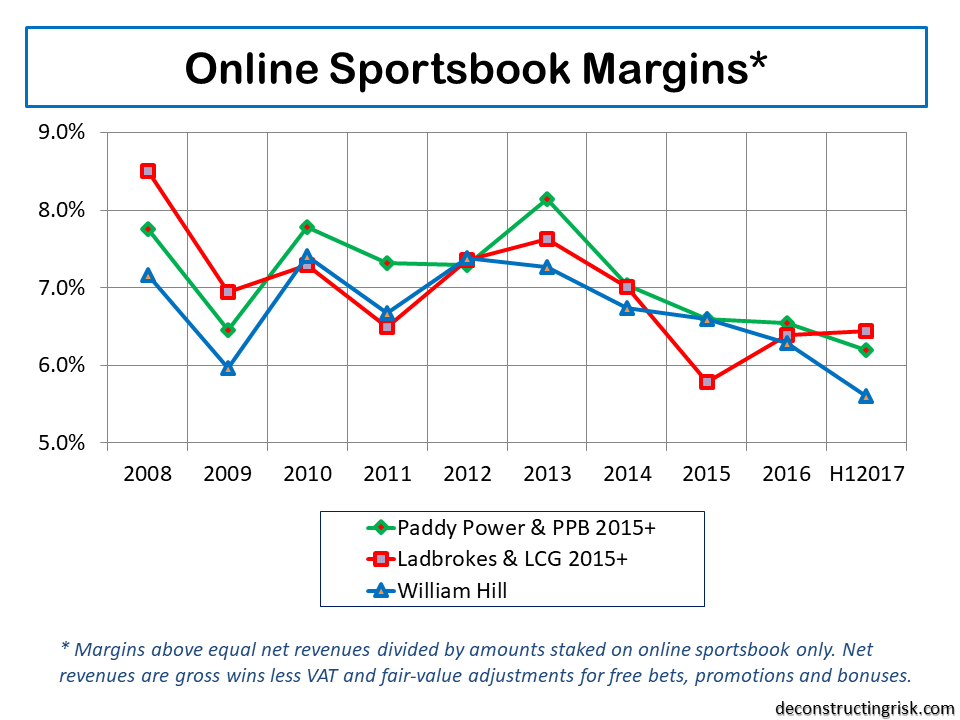

Despite the firm putting reduced net revenue margins primarily down to unfavourable sports results (increased promotion costs also contributed, doing things like paying out on Hilary Clinton prior to the actual election results doesn’t help!), the worry is that competitive pressures rather than bad luck are resulting in reduced net revenue and gross win margins. [Net revenues are gross wins less VAT and fair-value adjustments for free bets, promotions and bonuses]. Care needs to be taken when comparing gross win margins (i.e. gross win divided by amounts staked) and net revenue margins across firms as the make-up of the underlying portfolio is important (e.g. gross wins varies by sport type such as football, horses, tennis, etc and by geography) and firms may account for certain items differently. Also, the absence of the largest online player, the privately owned Bet365, makes industry analysis difficult for amateurs like me.

click to enlarge

Of course, this sector is haunted by regulatory risk. The predicted restrictions of the highly addictive gaming machines by the UK Government is expected to impact PPB’s high street competitors much more that PPB.L. For example, PPB.L only derives 6% of its revenue from gaming machines compared to 30% for William Hill. The reaction of PPB’s competitors to compensate for restrictions on gaming machine revenue is likely to have a bigger potential impact on PPB.L’s future results.

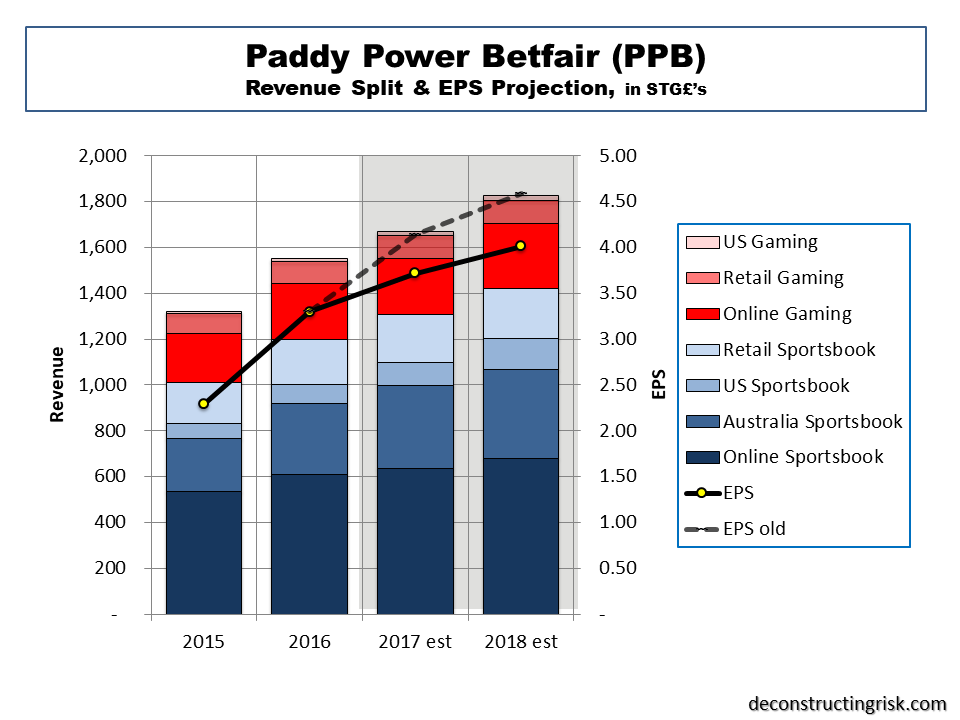

For me, the biggest disappointment in the Q2 results wasn’t the revenue line but the operating margins. The full year 2017 EBITDA projection was nearly 10% shy of my estimates. The firm acknowledged that the platform integration has been taking longer than planned and took up over 70% of internal technology resources in Q2. This is projected to reduce to 60% and 30% in Q3 and Q4 respectively before been completed by year end. Releasing these resources will allow a refocus on product development and on fixing other problem areas such as their online gaming offerings. As a result of the Q2 results, I have taken a knife to my earnings estimates (my revenue estimates only required minor adjustment) for 2017 and 2018, as the graphic below shows.

click to enlarge

My 2017 and 2018 EPS estimates have reduced to £3.72 and £4.01 respectively, down 10% and 12% from my previous estimates. That puts PPB.L’s current market cap at a PE of approximately 20 and 18 for 2017 and 2018. That’s not bad for a firm with EPS growth of 13% and 8% for 2017 and 2018 respectively although, if these figures turn out to be accurate, the share price is likely to have gone lower that it currently is on worries about reducing operating metrics in a fiercely competitive market.

These estimates are conservative in my view, possibly overtly so. They reflect a sense that Breon Corcoran’s reason to go off into the tech sunset now is really due to concerns about the medium-to-long term prospects for the sector. Corcoran obviously has put a different explanation forward, one which is suspiciously unconvincing given the amount left undone at PPB.L, although he still does have about £40 million of share options in PPB.L. No firm is simply about the CEO and at the end of the conference call an indication was given of ensuring more exposure to the full management team in future investor engagements. That should help investors get more comfortable with management depth at the firm. I know nothing about the new CEO, Peter Jackson, so he has a real challenge in gaining investor’s confidence. He has big boots to fill as far as investors are concerned.

So, yet again, I suggest the best course of action is to wait, both for existing and new shareholders, and see how 2017 develops for PPB.L. There can be little doubt that recent events mean that the odds on PPB.L have lengthened.

PS- PPB have already paid out on Floyd Mayweather prior to his 26th of August fight with Conor McGregor. In the unlikely event that the Irishman does achieve the impossible PPB’s Q3 net revenue margins will suffer……