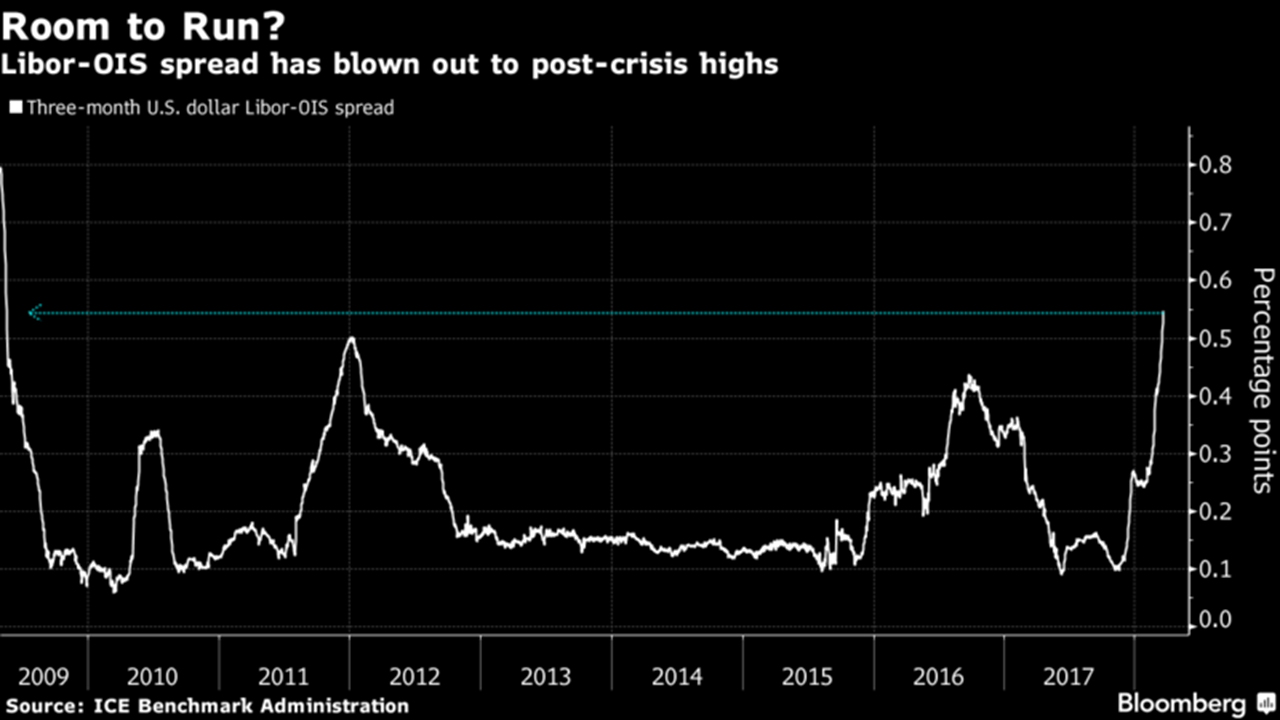

The market volatility in 2016 did seem odd in certain respects. Valuations were too high and a correction was needed. No doubt. It’s more the way the selling seemed to be indiscriminate at certain points with oil and equity prices locked in step. Some argue that China selling reserves to support their currency or oil producing countries selling assets to make up for short falls in oil revenue may be behind some of the erratic behaviour. Buttonwood had an interesting piece over the past weeks on how consequences from new bank regulations are impacting market liquidity with unusual activity in derivative pricing such as negative swap rates and relative CDS rates.

Gilian Tett, in a FT article in January, pointed to the example of capital outflows from China. Whether repaying US debt (or as Tett succinctly calls it, a quasi carry trade in reverse) in face of likely further yuan weakness or withdrawals from overzealous M&A (about a quarter of China outbound deals are said to be in trouble) or other reasons behind the veil of the Chinese economy, the outflows are having impacts. Tett said:

“Capital flows, fuelled by politics and policy change, are where the important action is taking place. Deep in the bowels of the system all manner of financial flows are switching course, creating unexpected knock-on effects for many asset prices. Capital flight from China is one example. The energy sector is another.”

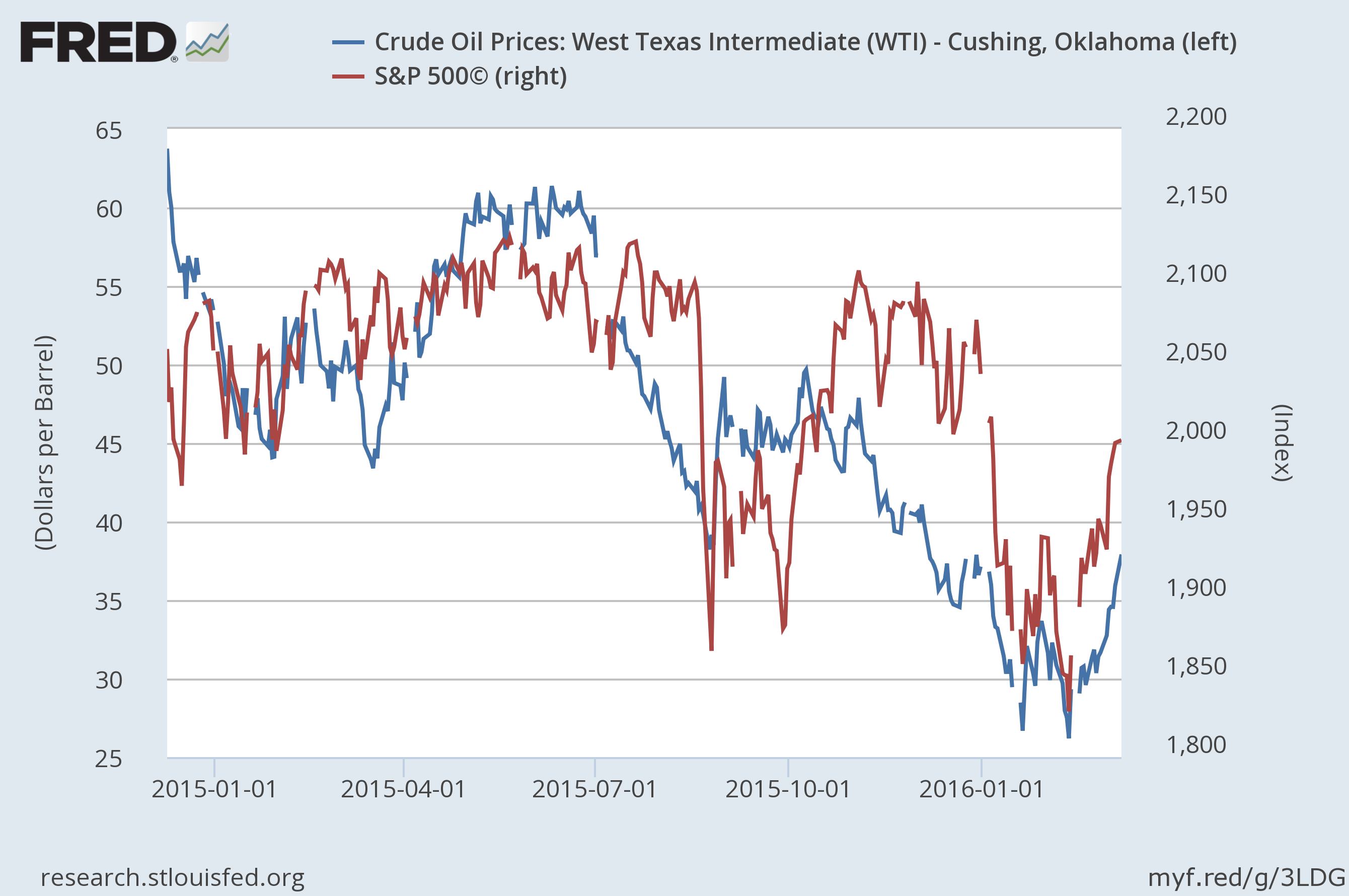

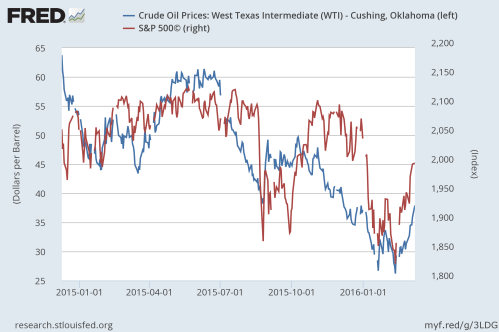

The strangle lockstep between oil and the S&P500 can be seen below.

click to enlarge

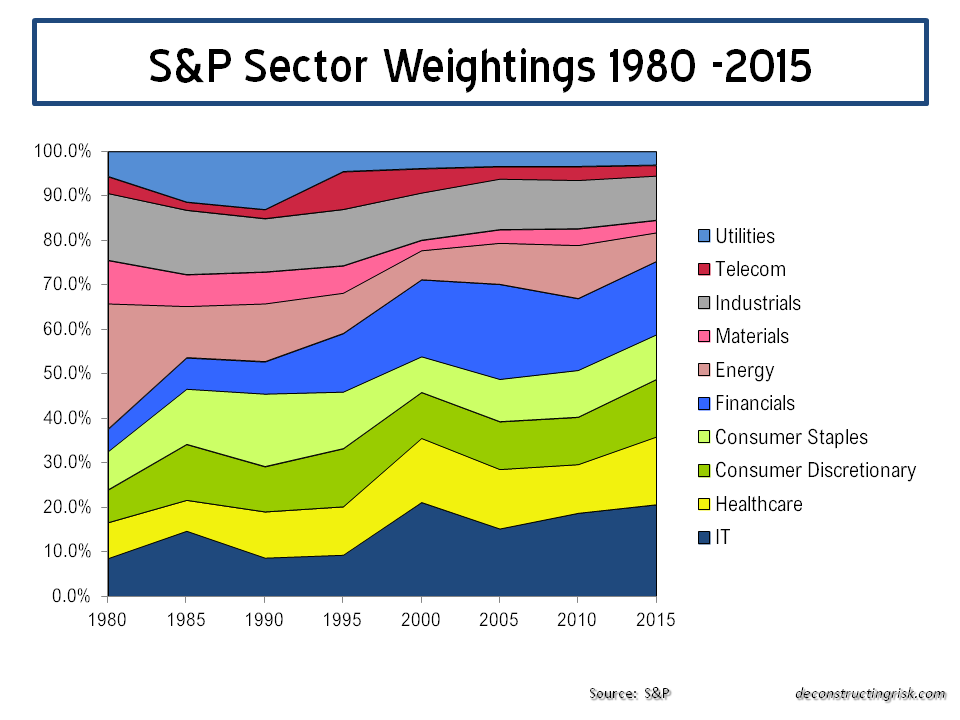

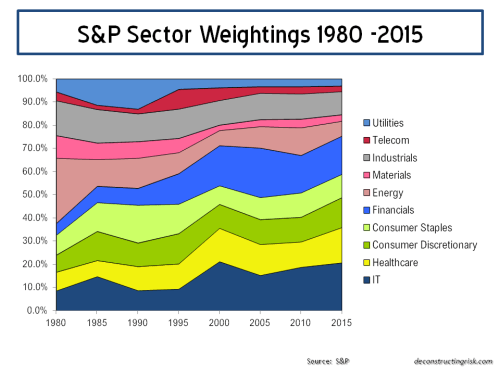

Energy has only a small impact on the S&P500 makeup, as can be seen below, and on the operating profit profile.

click to enlarge

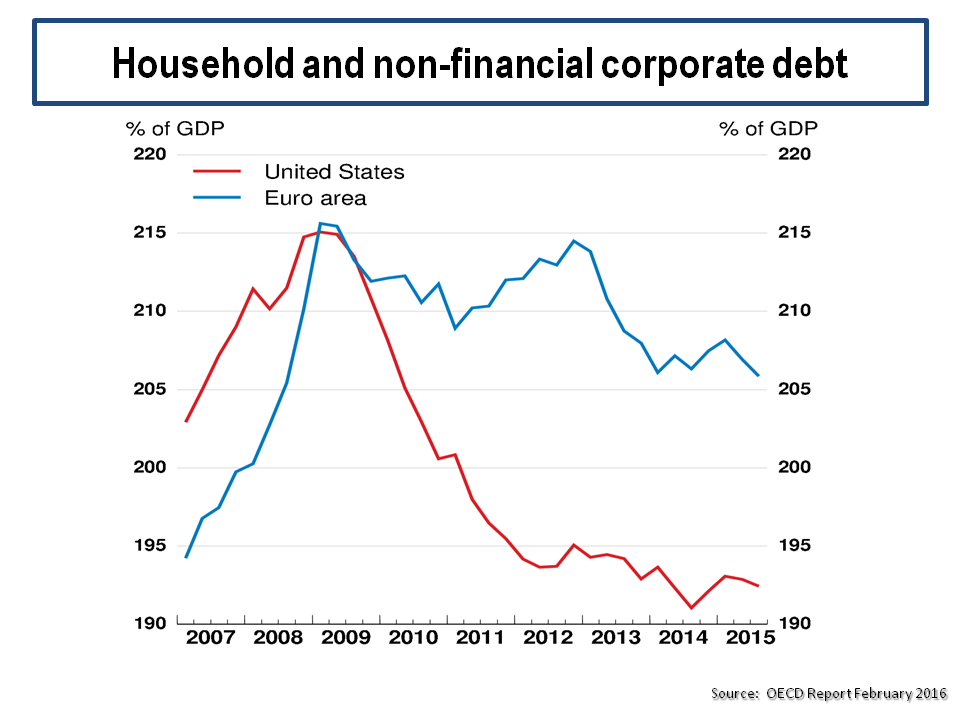

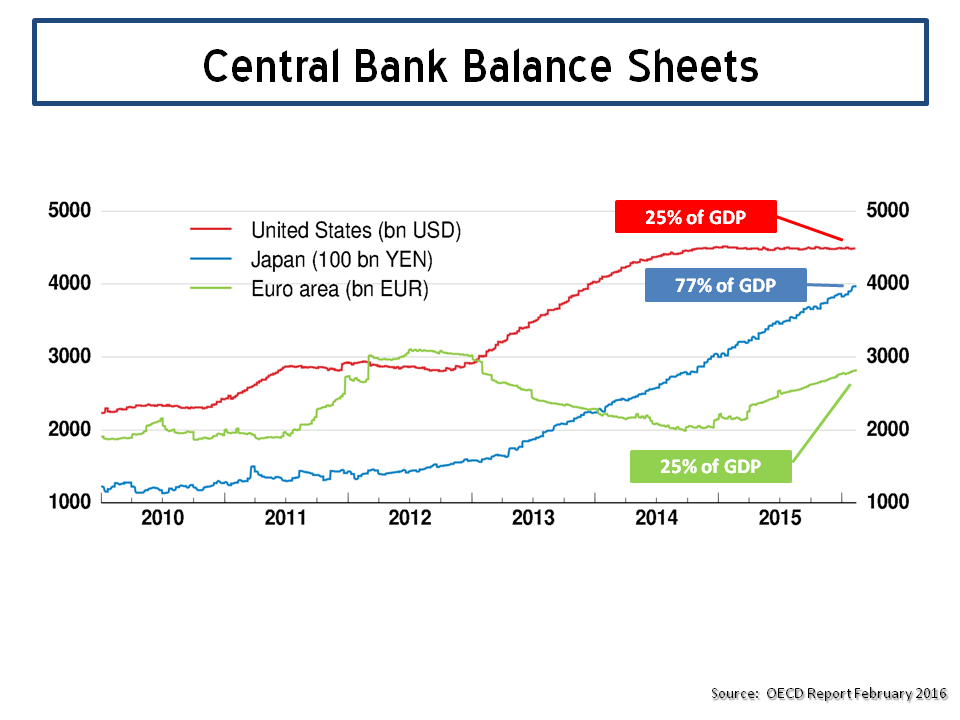

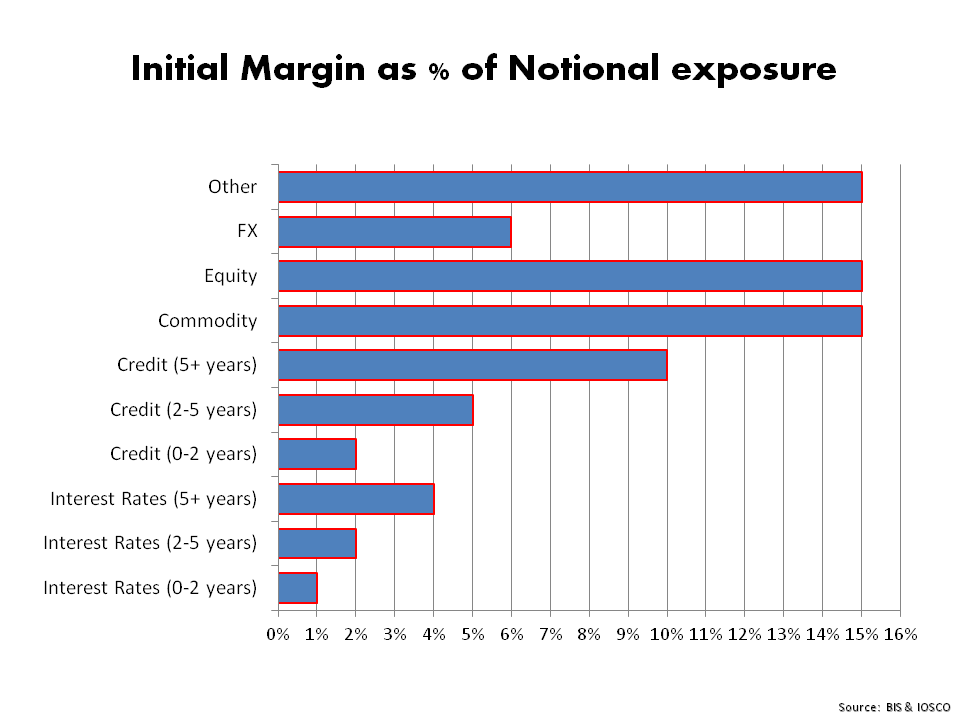

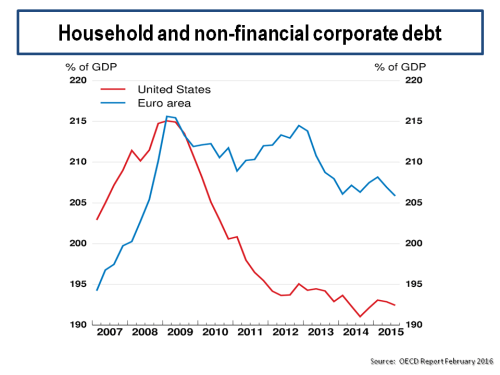

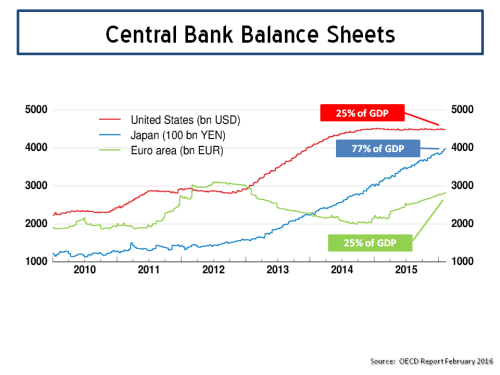

The OECD interim economic outlook by Catherine Mann on 18th February recommended “maintaining accommodative monetary policy, supportive fiscal policies on investment led spending and more ambition on structural policies which raise global growth and reduce financial risks”. Ah, yes the old structural reform answer to all of our ills. The OECD gave some graphic reminders of where we are, as below.

click to enlarge

click to enlarge

Central Bank policies remain stuck to QE and increasingly exotic forms of monetary policy despite the obvious failure so far for QE to kick-start either inflation or growth. The latest experiment is on negative interest rate which has had funny impacts on banks and the lending rates they need to charge. Japan in particular has shown how their brand of negative rates was countered by a currency whiplash. Mark Carney, the Governor of the Bank of England, offered the view that “for monetary easing to work at a global level if cannot rely on simply moving scarce demand from one country to another.”

A recent BIS article on negative interest rates in Switzerland, Europe and Japan stated that “there is great uncertainty about the behaviour of individuals and institutions if rates were to decline further into negative territory or remain negative for a prolonged period. It is unknown whether the transmission mechanisms will continue to operate as in the past and not be subject to tipping points“.

This week Mario Draghi came up with a new twist on negative interest rates, relying on targeted long-term refinancing operations (TLTROs) to give banks effectively free money. The currency impact will be interesting, particularly to see if the Japanese whiplash will repeat. One of the results of all this QE is that central banks are a much larger player in the system and have basically taken over the government bond markets in Europe, Japan, and America. The ECB even buys low-rated bonds, not just the AA and AAA positions taken by the Fed, and makes billions of euros in low-interest-rate loans to banks.

No less that Adair Turner, Martin Wolf and Ray Dalio have all made favourable comments about another evolution in QE, so called helicopter money (named after Milton Friedman). Wolf argues that central banks should enter the arena of public investment in the face of inaction by fiscal authorities (by which I assume he means elected politicians). He passionately says “policymakers must prepare for a new “new normal” in which policy becomes more uncomfortable, more unconventional, or both.” Turner believes that targeted stimulus of nominal demand poses “less risk to future financial stability than the unconventional monetary policies currently being deployed“.

The recent anxiety by electorates across the developed world in expressing a desire for the certainty of the past, whether it be the popularity of Donald Trump, anti-immigrant rhetoric in Europe or the arguments in the UK to leave the EC, show that ordinary people are worried about the future and no end of short term monetary stimulus is likely to change that. Helicopter money sounds like a medicated solution to the symptoms of low growth rather than any real answer to the problem of slowing growth, Chinese and Japanese unsustainable debt loads and global productivity challenges due to aging populations.

Maybe it’s just me, and I do respect the views of Wolf, Turner and Dalio, but it looks to me a measure that is open to so much moral hazard as bordering on the surreal. It gives Central Banks more power in the markets and that could be dangerous without more thought on the unintended consequences. If we are moving piecemeal towards a Chicago Plan or some other alternate economic model, then somebody should get the public on board. I think they are desperately looking for new answers to the way we run our economies.