There was some interesting commentary from senior executives in the reinsurance and specialty insurance sector during the Q2 conference calls.

Evan Greenberg of ACE gave the media a nice sound-bite when he characterised the oversupply in the property catastrophe sector as “that pond with more drinking out of it”. He also highlighted, that following a number of good years, traditional reinsurers “are hungry” and that primary insurers are demanding better deals as their balance sheets have gotten stronger and more able to retain risk. Greenberg warns that, despite claims of discipline by many market participants, for some reinsurers “it’s all they do for a living and so they feel compelled” to compete against the new capacity.

Kevin O’Donnell of Renaissance Re put some interesting perspective on the new ILS capacity by highlighting that in the early days of the property catastrophe focused reinsurer business model, they “thought about taking risk on a single model”. These reinsurers developed into multi-model and some into proprietary model users. O’Donnell highlighted that the new capacity from capital markets “is somewhat similar to” earlier property catastrophe reinsurance business models and “that, but beyond relying in some instances, on just a single model, they are relying on a single point.” O’Donnell stressed that “it’s very important to understand the shape of the distribution, not just the mean.” Edward Noonan of Validus commented that “the ILS guys aren’t undisciplined; it’s just that they’ve got a lower cost of capital.”

Historically lax pricing in reinsurance has quickly trickled down into softer conditions in primary insurance markets. In the US, although commercial insurance rates have moderated from an average increase of 5% to 4% in recent months, the overall trend remains upwards and above loss trend. Greenberg believes that the reason why it could be different this time is “the size of balance sheet on the primary side on the large players” and that more intelligent data analytics means that primary insurers are “making different kinds of decisions about how to hold retentions” and “how to think about exposure”. Although Greenberg makes valid points, in my opinion if pricing pressures continue in the reinsurance sector, the knock-on impacts onto the primary sector will eventually start to emerge.

As always, the market in property catastrophe is dependent upon events, particularly from the current windstorm season. Noonan of Validus commented that the market can’t “sustain a couple more years of 15% off”, referring to the recent Florida rate reductions. Diversified reinsurers point to their ability to rebalance their portfolios in response to the current market. However the resulting impact on risk adjusted returns will be an issue the industry needs to address. The always insightful and ever direct John Charman, now at the helm of Endurance Specialty, highlights the need to contain expenses in the industry. Charman commented “when I look at the industry, it’s very mature.” He characterised some carriers as being “very cumbersome” and “over-expensed”.

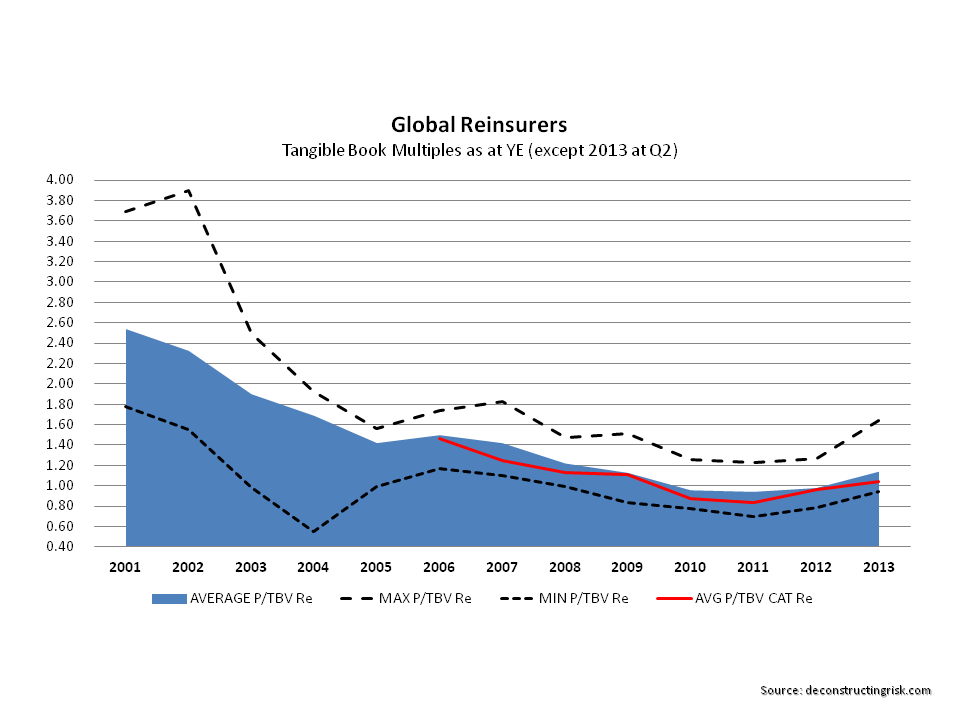

For the property catastrophe reinsurers, the shorter term impact on their business models will likely be that they will have to follow a capital management and shareholder strategy more compatible with the return profile of the ILS funds. In terms of valuations, the market is currently making little distinction between diversified reinsurers and catastrophe focussed reinsurers as the graph below of price to tangible book for pure reinsurers and catastrophe reinsurers show. Absent catastrophe events, that lack of distinction by the market could change in the near term.

click to enlarge

In the shorter term, the more seasoned and experienced players know how to react to an influx of new capacity. The conferences calls demonstrate those taking advantage of the arbitrage opportunities. Benchimol of AXIS commented that “we have actually started to hedge our reinsurance portfolio using ILWs and other transactions of that type.” O’Donnell commented that “we continue to look for attractive ways of ceding reinsurance risk as a means to optimizing our reinsurance portfolio.” Charman commented that “we also took advantage of the abundant capital by purchasing Florida retro protection”. Noonan commented that “we also found good value in the retrocession market and took the opportunity to purchase a significant amount of protection for our portfolio during the quarter.” Iordanou of Arch commented that “we did buy more this quarter” and that “we felt we were getting good deals.”

Right now, we are clearly in an arbitrage market and the reinsurers that will thrive in this market are those who are clever enough to use the current market dislocation to their advantage.