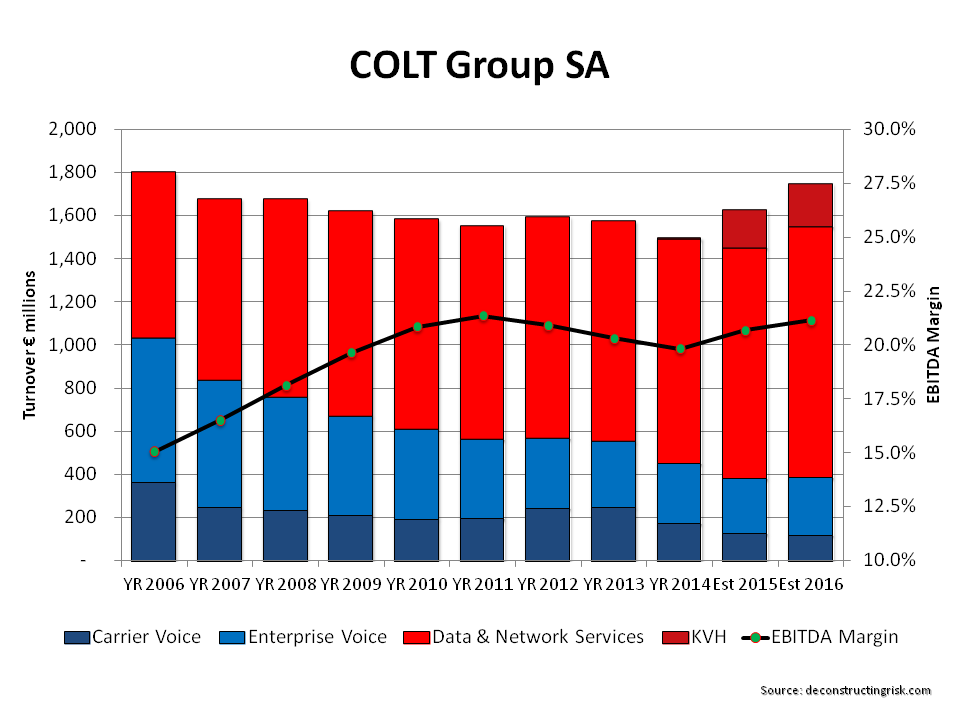

On Friday, Fidelity made a 190 pence offer, which is a 21% premium to the previous day’s close, for the approximately third of COLT that it doesn’t own. After years of underperformance and a series of restruturings, COLT has been long looking for a positive future. It bought the smaller Fidelity owned Asian carrier KVH last year (see previous posts here and here). COLT’s core European business has been slowly moving to higher growth and margin data and network business, as the graph below shows.

click to enlarge

Fidelity’s offer values the debt-free business at £1.7 billion (or €2.4 billion or $2.7 billion at current FX rates) which I estimate to be 7 times 2015 EBITDA or 6.44 times 2016 EBITDA estimates (assuming 2015 EBITDA of €335 million and a 2016 10% EBITDA YoY growth). The independent directors have called the offer too low but haven’t made a recommendation due to the lack of options for minority shareholders.

From Fidelity’s viewpoint, this looks like a clever move to force any likely bidders out into the open or, failing any bidders emerging, to take the firm fully private at an attractive price. Robert Powell over at telecomramblings speculates that other European carriers such as Interroute or the US based Level 3 may be possible bidders. It will be fascinating to see how this one plays out.