Mervyn King is not remembered (by this blogger at least) as a particularly radical or reforming governor of the Bank of England. It is therefore surprising that he has written an acclaimed book, called “The End of Alchemy”, with perhaps some of the most thoughtful ideas on possible reforms we could make to get the global economy out of its current hiatus. One of the central themes in the book is the inability of existing Western economic orthodoxy to adequately consider the impact of radical uncertainty. He quips that “current policies based upon the model of the economics of stuff rather than the economics of stuff happens”.

King defines radical uncertainty as “uncertainty so profound that it is impossible to represent the future in terms of probabilistic outcomes”. A current example could be the Brexit vote this coming Thursday, with commentators struggling to articulate the medium term knock-on impacts of this tightly forecasted vote. This post is not about Brexit as this blogger for one is struggling to understand the reasons and the impacts of the closeness of the vote. I do think the comments from Germany’s finance minister, Frank-Walter Steinmeier, this week that a leave vote would mean “the EU will find itself in a deep crisis” are pertinent and amongst the many issues we will likely face in the medium term if the UK actually disengages from the EU. The current mood of voters in Western economies, such as the UK and the US, does underline the urgent need for radical thinking to be adopted into the way we are addressing global economic and social issues in my view.

King’s book is not only full of interesting ideas but he also has a cutting turn of phrase. Amongst my favourites are: “economists mistrust trust”, “liquidity is an illusion”, and “any central bank that allows itself to be described as the only game in town would be well advised to get out of town”. Before I go over some of King’s ideas, I think it would be useful to recap on the conclusions from other recent books from UK authors on policy measures needed to address the current stagnation, in particular “The Shifts and the Shocks” by the highly regarded Financial Times commentator Martin Wolf and (to a lesser extent) “Between Debt and the Devil” by the former UK financial regulator Adair Turner. Wolf’s book was previously reviewed in this post and Turner’s book was referenced in this post.

Wolf articulated the causes of the financial crisis as “a savings glut and associated global imbalances, an expansionary monetary policy that ignored asset prices and credit, an unstable financial system, and naive if not captured regulation”. Wolf argues for practical policy measures such as much higher and more resilient capital requirements in banking (he rejects the 100% reserve banking envisaged by proponents of the so-called Chicago Plan as too radical), resolution plans for global systemic financial institutions, more bail-inable debt in banking capital structures and similar alignment changes to the terms of other financial contracts, proper funding of regulatory bodies and investigators of criminal misbehaviour, tax reform with a bias towards equity and away from leverage, tax on generational transfers of land, measures to address income inequality (due to the resulting dilution of demand stimulus measures as a result of the rich’s higher propensity to save) and measures to encourage business and infrastructure investment, education and R&D.

Wolf also highlights the need for new thinking at global institutions, such as IMF and those (unelected) bodies governing the Eurozone, particularly the urgent need (although he is pessimistic on the possibility) for global co-operation and radical action to address the imbalances in the global economy. The need for deeper co-ordination, irrespective of narrow short term nationalistic interests, is nowhere more obvious than in the Eurozone with the alternative being financial disintegration. The Brexit vote is an illustration of the UK electorate’s preference for disintegration (as is the popularity of Trump in the US), presented by shady politicians as a return to the good ole days (!??!), and is perhaps a precursor to a more general disintegration preference by voters across the globe. Wolf observes that “financial integration has proved highly destabilizing” and that “the world maybe no more than one to at most two crises away from such a radical deconstruction of globalized finance”.

Turner’s book is more focused on the failure of free markets to “ensure a socially optimal quantity of private credit creation or its efficient allocation” and the need for policy makers to constrain private credit growth, particularly excessive debt backed by real estate, and the creation of less credit intensive economies. Turner argues that “the pre-crisis orthodoxy that we could set one objective (low and stable inflation) and deploy one policy tool (interest rate) produced an economic disaster”. In common with Wolf, Turner also advocates structural changes to tax and financial contracts to incentivize credit away from land and towards productive investment and policies to address income inequality. Turner also rejects 100% reserve banking as too radical in today’s world and favours much higher capital requirements and restrictions on the shadow banking sector. On the need for China and Germany to take responsibility for the impact of their policies on global imbalances, he repeats the pious lecturing of current elites (without the negativity of Wolf on the reality of such policies actually happening). Similarly he repeats the (now) consensus view on the need for the Eurozone to either federalise or dissolve.

As to real solutions, Turner states that “our challenge is to find a policy mix that gets us out of the debt overhang created by past excessive credit creation without relying on new credit growth” and favours the uses of further monetary measures such as Bernanke’s helicopter money, once-off debt write off and radical bank recapitalisation. Although he highlights the danger of opening the genie of money finance, his arguments on containing such dangers in the guise of once-off special measures are not convincing.

King highlights many of the same issues as Wolf and Turner as to how we got to where we are. The difference is in his reasoning of the causes. He points to significant deficiencies in the academic thinking behind the policies that govern Western economies. As such, his suggestions for solutions are more fundamental and require a change in consensus thinking as well as changes in policy responses. As King puts it – “I came to believe that fundamental changes are needed in the way we think about macroeconomics as well as in the way central banks manage their economics”. According to King, theories upon which policies are based need to accommodate the reality of radical uncertainty, a model based upon the economics of stuff happens rather than the current purest (and unrealistic) models of the economics of stuff. King states that “we need an alternative to both optimising behaviour and behavioural economics”.

One of King’s most interesting and radical ideas is for a compromise between the current fractional banking model and the 100% reserve narrow bank model proposed under the so-called Chicago Plan. As King observes “to leave the production of money solely to the private sector is to create a hostage to fortune” and “for a society to base its financial system on alchemy is a poor advertisement for its rationality”. The alchemy King refers to here (and in the title of his book) is the trust required in the current “borrow short-lend long” model we employ in our fractional banking system. Such trust is inherently variable due to radical uncertainty and the changes in the level of trust as events unfold are at the heart of the reason for financial crises in King’s view.

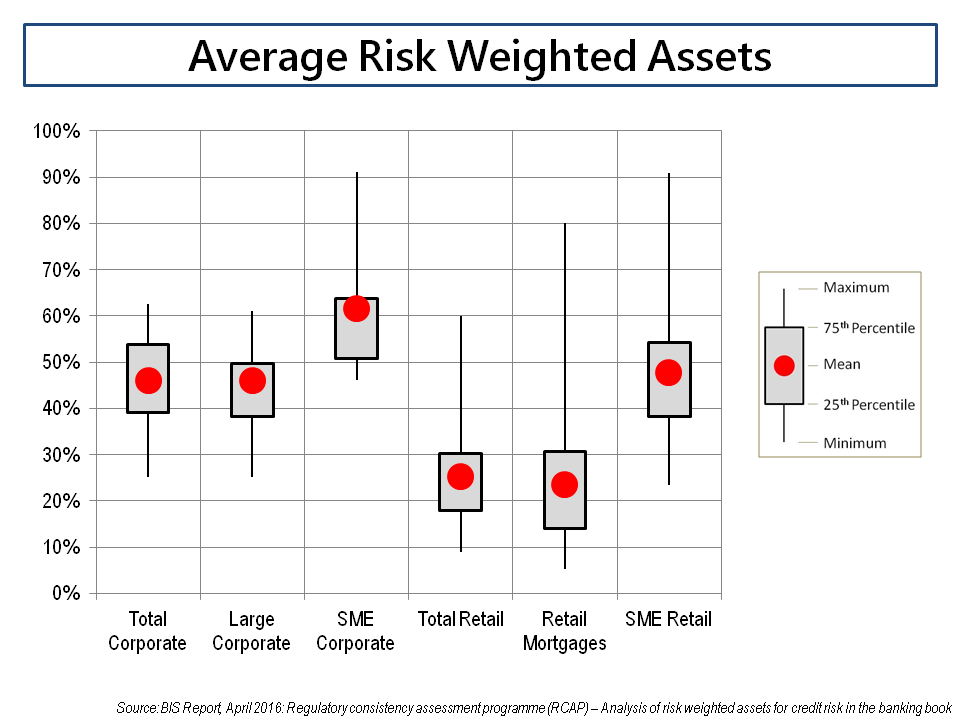

Perhaps surprising for an ex-governor of the Bank of England, King highlights the dangers of overtly complex regulations (the UK PRA rule-book runs to 10,000 pages for banks) with the statement that “by encouraging a culture in which compliance with detailed regulations is a defence against a charge of wrong-doing, bankers and regulators have colluded in a self-defeating spiral of complexity”. He warns that “such complexity feeds on itself and brings the system into disrepute” and that “arbitrary regulatory judgements impose what is effectively a high tax on all investments and savings”. This is a sentiment that I strongly agree with based upon recent experiences. All of the authors mentioned in this post are disparaging on the current attempts to fix banking capital requirements, particularly the discredited practise of applying capital ratios to risk weighted assets (RWA). A recent report from the Bank of International Settlements (BIS) illustrates the dark art behind bank’s RWA calculations, as per the graph below.

click to enlarge

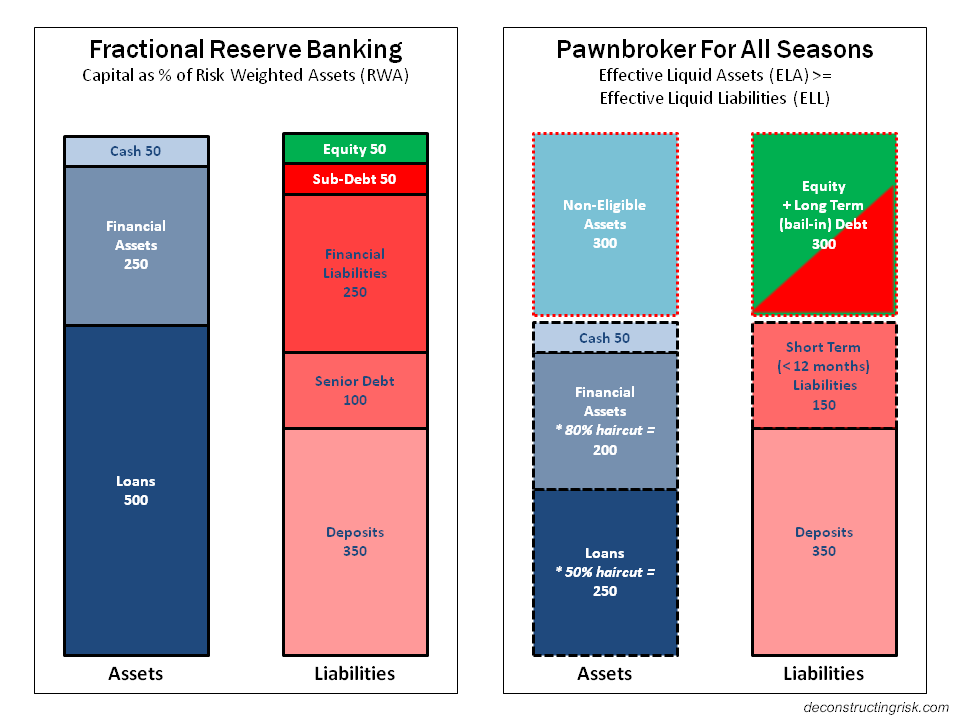

King’s idea is to replace the lender of last resort (LOLR) role of Central Banks in the current system to that of a pawnbroker for all seasons (PFAS). In non-stress times, Central Banks would assess haircuts against bank assets, equivalent to an insurance premium for access to liquidity, which reflect the ability of the Central Bank to hold collateral through a crisis and dispose of the assets in normal times (much as they currently do under QE). These assets would serve as pre-positioned collateral which could be submitted to the Central Bank in exchange for liquidity, net of the haircut, in times of stress who would act as a pawnbroker does. The current regulatory rules would then (over a transition period of 10-20 years) be replaced by two simply rules. The first would be a simple limit on leverage ratio (equity to total nominal assets). The second rule would be that effective liquid assets or ELA (pre-positioned collateral plus existing Central Bank reserves) would be at least equal to effective liquid liabilities or ELL (total deposits plus short term unsecured debt). The graphic below represents King’s proposal compared to the existing structure.

click to enlarge

King states that “the idea of the PFAS is a coping strategy in the face of radical uncertainty” and that it is “akin to a requirement on private institutions to take out compulsory insurance”. He highlights its simplicity as a workable solution to the current moral hazard of the LOLR which recognises that in a crisis the only real source of liquidity is the Central Bank and it structurally provides for such liquidity on a pre-determined basis. Although it is not a full narrow bank proposal, it does go some way towards one. As such, and as the graphic illustrates, it will require a significant increase in equity for private banks (similar to that espoused by Wolf and Turner, amongst others) which will have an impact upon overall levels of credit. Turner in particular argues strongly that it is the type of credit, and its social usefulness, that is important for long term sustainable economic growth rather than the overall level of credit growth. Notwithstanding these arguments, the PFAS is an elegant if indeed radical proposal from King.

Another gap in modern economic theory and thinking, according to King, is the failure to follow policies which address the problem of the prisoner’s dilemma, defined as the difficulty of achieving the best outcome when there are obstacles to co-operation. King gives the pre-crisis failure to recognise that each private bank faced a prisoner’s dilemma in running down its holdings of liquid assets, and financing itself as cheaply as possible by short-term debt, as the only means of competing with its peers on the profit expectations of the free market. The global economy currently faces a prisoner’s dilemma as the current (tired) orthodoxy of trying to stimulate demand is failing across developed economies as people are reluctant to consume due to fears about the future. In his own acerbic way, King quips that we cannot expect the US “to continue as the consumer of last resort”.

Current policy measures of providing short-term stimulus through low interest rates are diametrically opposite to those needed in the long run in King’s view. People, in effect, do not believe the con that Central Bank’s artificial reduction in risk premia is trying to sell, resulting in a paradox of policy. King believes that “further monetary stimulus is likely to achieve little more than taking us further down the dead-end road of the paradox of policy“. This means that Central Banks are currently in a prisoner’s dilemma – if any of them were to unilaterally raise interest rates, they would risk a slowing of growth and possibly another downturn in their jurisdiction. A co-ordinated move to a new equilibrium is what is needed and institutions like the IMF, who’s role is to “speak truth to power”, can hypnotise all they like about what is needed but the prisoner’s dilemma restricts real action. Unfortunately, King does not have any real solution to this issue besides those hopeful courses of action offered by others such as Wolf and Turner.

The unfortunate reality is that we seem to be on a road towards more disintegration rather than greater co-operation in the world economy. King does highlight the similarities of such a multi-polar world with the unstable position prior to the First World War, which is a cheery thought. Any future move towards disintegration across developed economies doesn’t bode well for the future, particularly when the scary issue of climate change is viewed in such a context. I hope we wouldn’t get more illustrations of the impact of radical uncertainty on our existing systems in the near future, nor indeed of our policymaker’s inability to address such uncertainty in a coherent and timely way.

I do however strongly recommend King’s book as a thought provoking read, for those who are so inclined.

Interesting how former central bankers change their respective minds once the left office (remember The Maestro, now firmly advocating gold as an investment?). I ordered his book already and will go through it in detail but his comments already make a lot of sense to me (like “liquidity is an illusion”… anyone who tried to unload some structured credit stuff during 2009 will likely subscribe to that… also warning about overly complex regulation rings a familiar bell).

What makes me wonder, a bit at least, is that liquidity is mentioned nowhere, there seems to be a strong focus on capital. If I remember correctly a handful of banks had liquidity issues during 2008/2009, basically a classic bank run when everybody tried to pull out his money, but capital was no issue. The upcoming regulations regarding liquidity, namely LCR (Liquidity Coverage Ratio) and NSFR (Net Stable Funding Ratio) should have a major impact going forward, especially in some corners where you don’t expect it (holding huge deposits from corporates and friends becomes very unattractive for example whereas you have to hold a ton of govies or similar stuff when only so much of these goes around). Which brings me back to the overly complex regulation topic…

A very nice write-up and I look forward to the day when I can lay my hands on his book :).

Eddie

Enjoy it Eddies.

Hope all good with you.

Another nice quote from King: Investors are simply people trying to cope with an unknowable future and behave, as we all do in such situations, sometimes cautiously, sometimes erratically, but always in a fog of uncertainty.

…..M

Thanks Mozoz, it just arrived the other day. I’m doing fine, thanks for asking.

So true…

Something completly different (being non-judgemental here): what is your assessment regarding the Brexit vote? Do you think they will it off?

Eddie

Not sure Eddie, still trying to figure it out, it’s clear though that the vote was a protest one, older generation hankering after yesteryear, p*ssed off at what low interest rates doing to pensions, lower class p*ssed off at globalisation and Internet economy, leave campaign have no idea of which exit model they want, EU disintegration real possibility.

I think it may a inflection point in trying to patch up old economic system, real change needed but unlikely.

A risk off period ahead as mess gets worse.

Just initial thoughts, still reading.

M

Thanks Mozoz. Given the distribution of Remain votes among London, Scotland and Northern Ireland I would also say it was quite a bit about protest and showing the so-called elite and the bankers that “normal” people are unhappy about the course of events. But I am afraid that things are much more involved and complicated than the Leave campaigners would admit (rest-EU has every reason to play hardball and someone has to fund that twin deficit after all while the rest of the world has no incentive to offer preferential terms). Buttonwood has a nice first analysis here:

http://www.economist.com/blogs/buttonwood/2016/06/after-referendum

Throw in the fact that Scotland and Northern Ireland depend on EU subsidies and Great Britain might become Little England over time.

This could be the kind of shell shock the EU needs to bring its act together and think about what people what, not just the politicians. I see some first encouraging signs.

Market wise… well, this is probably not a Lehman moment but it could be a Bear Sterns moment. Let’s see who has been swimming naked… we shall find out in due course I guess.

Eddie