As the market pulls back again this week in a much-needed dose of worry about where QE is leading us and how it will end, there is another interesting article from Buttonwood in this week’s Economist. Based upon work of analysts in investment banks BNP Paribas, Société Générale, and Goldman Sachs (Andrew Lapthorne of SG does high quality analysis and his work generally makes for insightful reading), the article highlights how valuations based upon price to book ratios have broken with pre-crisis history and currently differentiate more acutely between “quality” stocks (depending upon varying criteria as applied by the said analysts).

The article highlights the limited pool of “quality” stocks no-matter what criteria is used and Buttonwood also makes a point (which I fully agree with), namely that “investors have been flocking to equities because interest rates are so low; some, perhaps, on the naive view that using a lower discount rate on future cashflows translates into higher share prices today“.

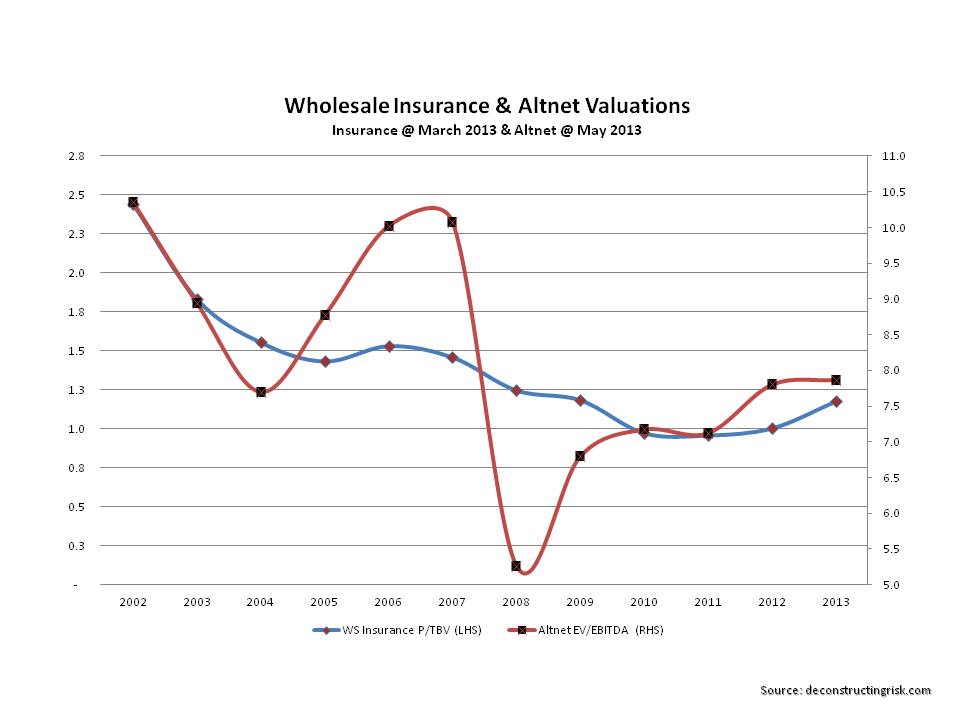

As readers of this blog will be aware, two sectors that I follow are the wholesale insurance and the alternative telecom sectors. In previous posts, I have presented my historical valuation metrics for both sectors (albeit from limited samples) and they are combined in the graph below (one based upon price to tangible book, the other an EV/ebitda metric). The alternative telecom sector is as far away from any “quality” stock criteria that one could imagine and would be in the lowest quintile (on volatility alone!) of any sensible criteria. Although results are volatile by definition in the wholesale insurance sector, some of the bigger names like Munich Re may get higher ratings, maybe a 2 or 3 on Buttonwood’s graph.

click to enlarge

The main point I am trying to make in this post is that relying on valuations returning to levels prior to the financial crisis for certain sectors is just not realistic or sensible. Unless the market goes into fantasy land on the upside (this may seem idle speculation given the market’s current mood but just think where sentiment was a few short weeks ago), the differentiation currently been made in the market between business models and their inherent volatility is rational. The worry, as the article points out, is that there is not enough “quality” stocks around currently to wet the appetite of hungry investors and historically that has been a negative indicator for future stock returns.