Michael Lewis, in his 2011 book “Boomerang” on the consequences of the financial crisis, said that “leverage buys you a glimpse of a prosperity you haven’t earned”. Well, if that is true, we are all in trouble based upon the findings from the fascinating Geneva report “Deleveraging? What Deleveraging?” from Luigi Buttiglione, Philip Lane, Lucrezia Reichlin and Vincent Reinhart, published yesterday.

The report paints a stark picture, as the following statements illustrate:

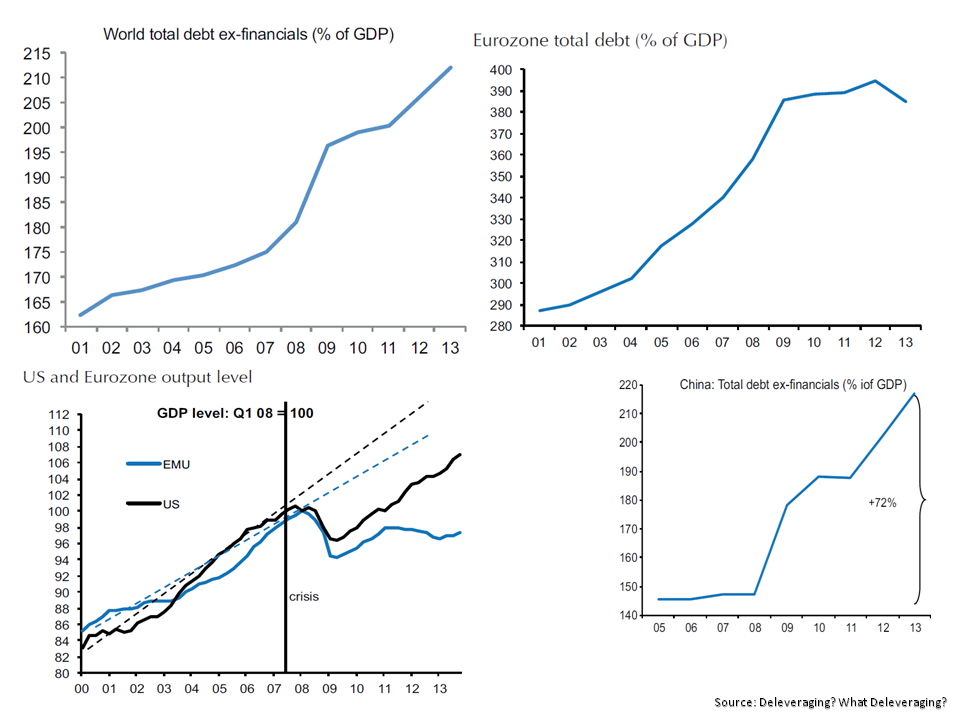

“Contrary to widely held beliefs, the world has not yet begun to delever and the global debt-to-GDP is still growing, breaking new highs. At the same time, in a poisonous combination, world growth and inflation are also lower than previously expected, also – though not only – as a legacy of the past crisis. Deleveraging and slower nominal growth are in many cases interacting in a vicious loop, with the latter making the deleveraging process harder and the former exacerbating the economic slowdown. Moreover, the global capacity to take on debt has been reduced through the combination of slower expansion in real output and lower inflation.”

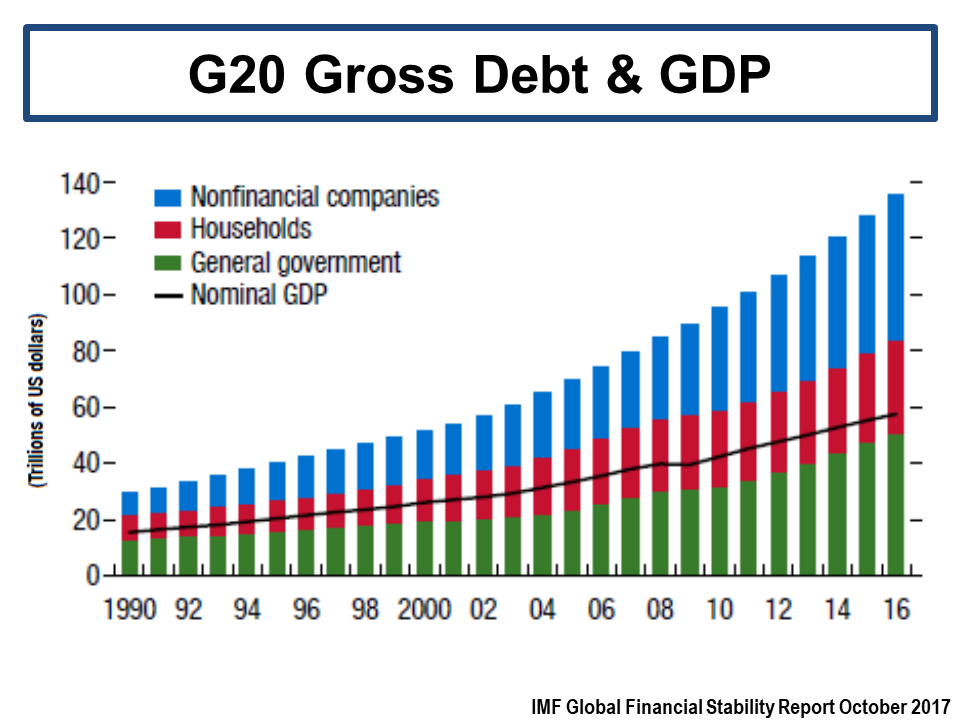

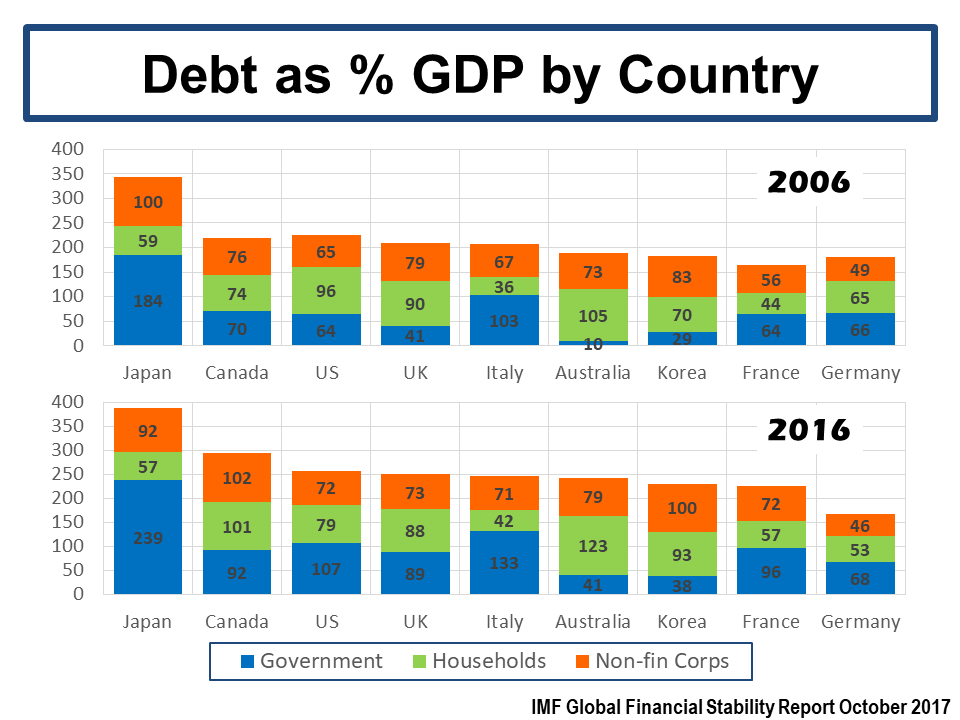

The report has a number of attention grabbing graphs on debt levels as a % of GDP like the one below on the US and others on Europe, China and global debt levels, as below.

click to enlarge

click to enlarge

The report is particularly pessimistic about China’s medium term prospects after its rapid 72% rise in debt levels since the crisis. On the US and the UK, for the countries who “managed the trade-off between deleveraging policies and output costs better so far, by avoiding a credit crunch while achieving a meaningful reduction of debt exposure of the private sector and the financial system” the legacy of “a substantial re-leveraging of the public sector, including the central banks” leaves a considerable challenge for the future.