It’s been a great 12 months for wholesale insurers with most seeing their share price rise by 20%+, some over 40%. As would be expected, there has been some correlation between the rise in book values and the share price increase although market sentiment to the sector and the overall market rally have undoubtedly also played their parts. The graph below shows the movements over the past 12 months (click to enlarge).

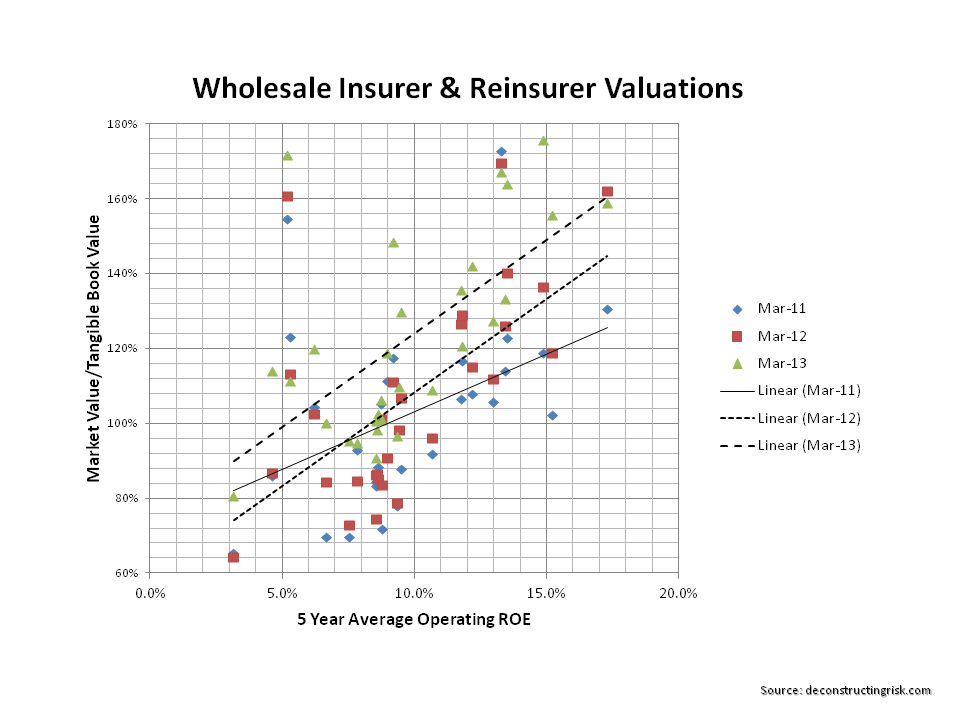

The price to tangible book is one of my preferred indicators of value although it has limitations when comparing companies reporting under differing accounting standards & currencies and trading in different exchanges. The P/TBV valuations as at last weekend are depicted in the graph below. The comments in this post are purely made on the basis of the P/TBV metric calculated from published data and readers are encouraged to dig deeper.

The price to tangible book is one of my preferred indicators of value although it has limitations when comparing companies reporting under differing accounting standards & currencies and trading in different exchanges. The P/TBV valuations as at last weekend are depicted in the graph below. The comments in this post are purely made on the basis of the P/TBV metric calculated from published data and readers are encouraged to dig deeper.

I tend to look at the companies relative to each other in 4 broad buckets – the London market firms, the continental European composite reinsurers, the US/Bermuda firms, and the alternative asset or “wannabe buffet” firms. Comparisons across buckets can be made but adjustments need to be made for factors such as those outlined in the previous paragraph. Some firms such as Lancashire actually report in US$ as that is where the majority of their business is but trade in London with sterling shares. I also like to look at the relative historical movements over time & the other graph below from March 2011 helps in that regard.

Valuations as at March 2013 (click to enlarge):

Valuations as at March 2011 (click to enlarge):

The London market historically trades at the highest multiples – Hiscox, Amlin, & Lancashire are amongst the leaders, with Catlin been the poor cousin. Catlin’s 2012 operating results were not as strong as the others but the discount it currently trades at may be a tad unfair. In the interest of open disclosure, I must admit to having a soft spot for Lancashire. Their consistent shareholder friendly actions result in the high historical valuation. These actions and a clear communication of their straight forward business strategy shouldn’t distract investors from their high risk profile. The cheeky way they present their occurrence PMLs in public disclosures cannot hide their high CAT exposures when the occurrence PMLs are compared to their peers on a % of tangible asset basis. Their current position relative to Hiscox and Amlin may be reflective of this (although they tend to go down when ex dividend, usually a special dividend!).

The London market historically trades at the highest multiples – Hiscox, Amlin, & Lancashire are amongst the leaders, with Catlin been the poor cousin. Catlin’s 2012 operating results were not as strong as the others but the discount it currently trades at may be a tad unfair. In the interest of open disclosure, I must admit to having a soft spot for Lancashire. Their consistent shareholder friendly actions result in the high historical valuation. These actions and a clear communication of their straight forward business strategy shouldn’t distract investors from their high risk profile. The cheeky way they present their occurrence PMLs in public disclosures cannot hide their high CAT exposures when the occurrence PMLs are compared to their peers on a % of tangible asset basis. Their current position relative to Hiscox and Amlin may be reflective of this (although they tend to go down when ex dividend, usually a special dividend!).

Within the continental European composite reinsurer bucket, the Munich and Swiss, amongst others, classify chunky amounts of present value of future profits from their life business as an intangible. As this item will be treated as capital under Solvency II, further metrics need to be considered when looking at these composite reinsurers. The love of the continental Europeans of hybrid capital and the ability to compare the characteristics of the varying instruments is another factor that will become clearer in a Solvency II world. Compared to 2011 valuations Swiss Re has been a clear winner. It is arguable that the Munich deserves a premium given it’s position in the sector.

The striking thing about the current valuations of the US/Bermudian bucket is how concentrated they are, particularly when compared to 2011. The market seems to be making little distinction between the large reinsurers like Everest and the likes of Platinum & Montpelier. That is surely a failure of these companies to distinguish themselves and effectively communicate their differing business models & risk profiles.

The last bucket is the most eccentric. I would class firms such as Fairfax in this bucket. Although each firm has its own twist, generally these companies are interested in the insurance business as the provider of cheap “float”, a la Mr Buffet, with the focus going into the asset side. Generally, their operating results are poorer than their peers and they have a liking for the longer tail business if the smell of the float is attractive enough (which is difficult with today’s interest rate). This bucket really needs to be viewed through different metrics which we’ll leave for another day.

Overall then, the current valuations reflect an improved sentiment on the sector. Notwithstanding the musings above, nothing earth shattering stands out based solely on a P/TBV analysis. The ridiculously low valuations of the past 36 months aren’t there anymore. My enthusiasm for the sector is tempered by the macro-economic headwinds, the overall run-up in the market (a pull-back smells inevitable), and the unknown impact upon the sector of the current supply distortions from yield seeking capital market players entering the market.