Following on from the previous post, the graph below shows the historical P/TBV ratios for selected reinsurers and wholesale insurers with a portfolio including material books of reinsurance (company names as per previous post). The trend shows the recent uptick in valuations highlighted in the previous post. The graph is also consistent with the Guy Carpenter price to book value graph widely used in industry presentations.

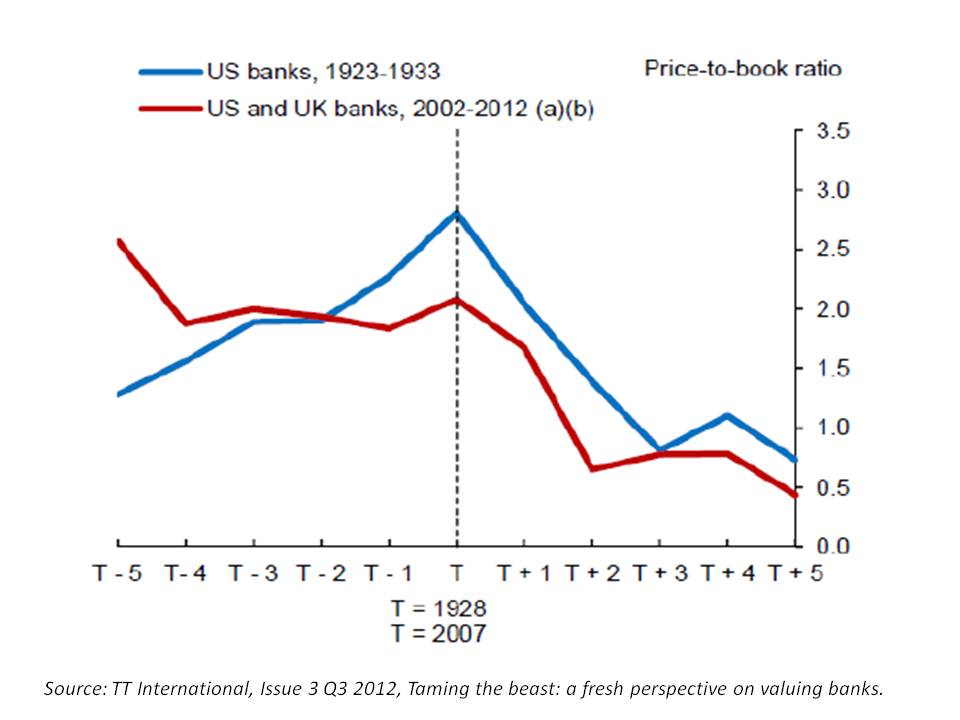

Over the past 12 months the sector has broken out of the downward trend across the financial services sector following the financial crisis, most notably in the banking sector as the graph below from TT International illustrates.

Over the past 12 months the sector has broken out of the downward trend across the financial services sector following the financial crisis, most notably in the banking sector as the graph below from TT International illustrates.

Tangible book value growth across the wholesale insurance sector was approximately 10% from YE2011 to YE2012 and the weighted average operating ROE of 11% in 2012 has been rewarded with higher multiples.

The sector faces a number of significant issues and a return to valuations prior to the financial crisis remains unrealistic. An increase in capacity from non-traditional sources and the increased loss costs from catastrophes are cited in industry outlooks as headwinds although I tend to agree with EIOPA’s recently published risk dashboard in highlighting the impact of macro-economic risks on insurer’s balance sheets as the major headwind.

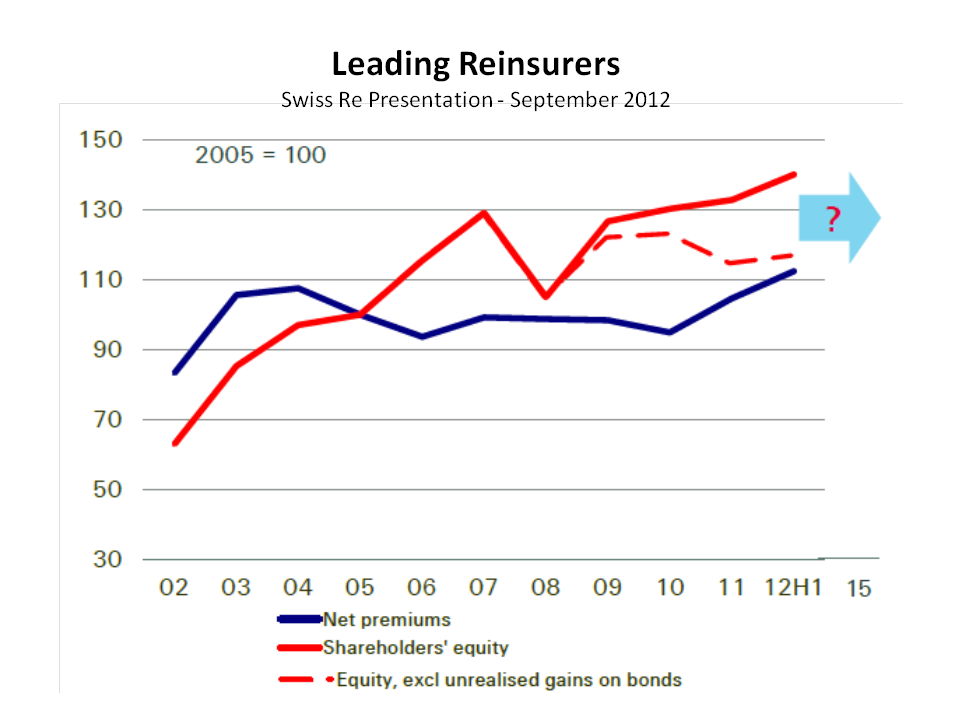

One issue that deserves further attention in this regard is the impact low interest rates have had on boasting unrealised gains and the resulting impact on the growth in book values. Swiss Re is one of the few companies to explicitly highlight the role of unrealised gains in its annual report, making up approximately 13% of its equity. In a presentation in September 2012, the company had an interesting slide on the impact of unrealised gains on the sector’s capital levels, reproduced below.

P/TBV is one of my favoured metrics for looking at insurance valuations. But no one metric should be looked at in isolation. The impact of any sudden unwinding of unrealised gains if the macro environment turns nasty is just one of the issues facing the sector which deserves a deeper analysis.