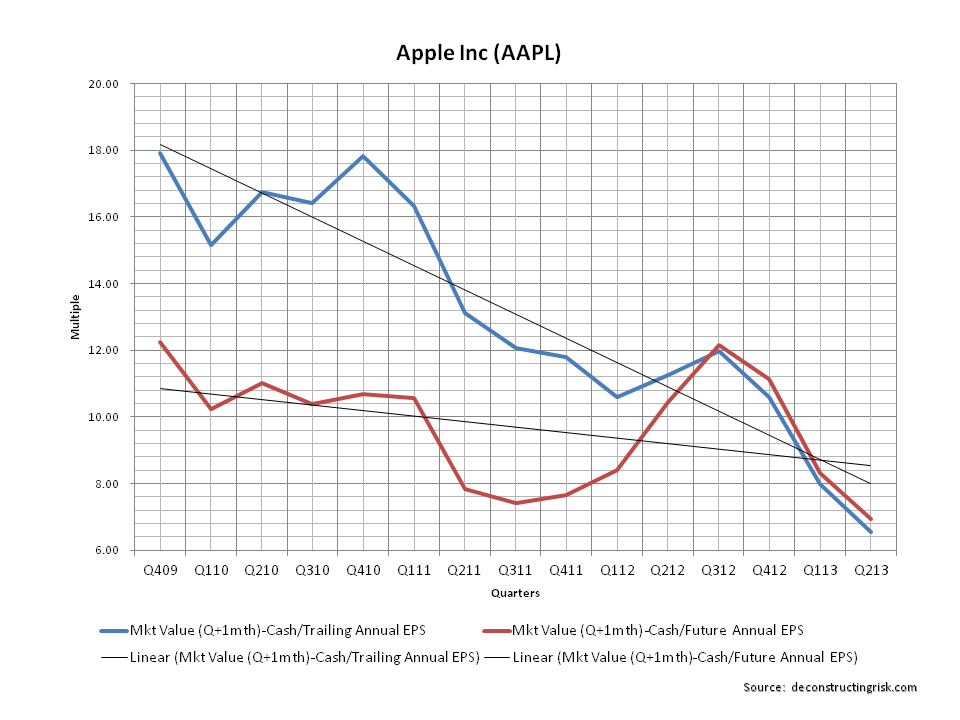

Following on from my initial post on Apple’s past, I have spent some time reading up on bull and bear views of its future. Oh my, there really is a massive amount of opinion out there! I knew that Apple was the most analysed stock in the world but I didn’t fully realise the extent of the chatter. The level of discussion was particularly strong last week as AAPL traded below $400. The focus now is the Q2 results due on Tuesday and the gross margins it will report and what can be assumed about Apple’s short term trajectory. There is a lot of noise about Apple at the moment but I am more interested with the medium term and the implied valuation from looking beyond the noise.

From past experience, I am very aware that when any stock falls from grace or reaches maturity, there is the danger that an attachment to the “glory days” can colour judgement on future prospects and capture sets in. As I am not an Apple user and have never directly owned Apple stock previously, I hope my perception is somewhat unbiased. The emotional capture trap that’s so dangerous in investing is something that I have fell for before and one I am very wary of.

I am in big believer in the wisdom of George Box’s quote that “all models are wrong, but some are useful”. In attempting to do a discounted cash flow analysis of a technology company like Apple, you have to make numerous assumptions, most of which will likely turn out to be way off the mark. The purpose here is not to predict the future but to get an idea of Apple’s valuation given the views prevalent today. Before detailing the assumptions for the three scenarios I selected, I have a number of observations:

1) The importance of the smartphone market (or whatever smartphones evolves into) to Apple will likely not decrease if its financial success is to be maintained. No foreseen new markets, such as TV or watches alone, can ever, in my opinion, match the size and profitability of the iPhone. iPhones and iPads are likely to evolve & merge into a variety of portable products – mini iPads, low cost iPhones, portable iTVs – of differing sizes and capabilities. Whatever they turn out to be, they will remain critical to Apple. There is of course the possibility of an unforeseen killer product or market for Apple in the future. However, as they say, “hope is not a strategy”. Simply relying on Apple to innovate successfully on a scale similar to the iPhone in the future is, in my opinion, naive and not refective of the maturing nature of the market.

2) It is increasingly likely that Apple will not be able to maintain the gross or net margins that it has achieved in recent years, both for its existing products and for new products. My projections assume varying levels of gross margin reduction and revenue per product reductions. Apple now has strong competitors and maintaining high margins and high prices in a competitive and increasing commoditised market (even at the high end) that is reaching maturity in the core developed jurisdictions is not, in my opinion, realistic.

3) Initially I did think one scenario would reflect a Nokia/Motorola type implosion for Apple. However, just as my analysis concludes that Apple’s rapid revenue growth years are behind it, Apple’s uniqueness, its unflinching focus on quality, its core loyal customer base, and its ecosystem make a rapid decline equally unlikely. Its DNA, driven by its past, and its cash pile also make such a decline improbable in my view.

So, with the understanding that the analysis below is rough and ready, and has been done by somebody with a partial knowledge of the underlying subject, the following is presented here purely to stimulate consideration of Apple’s current valuation.

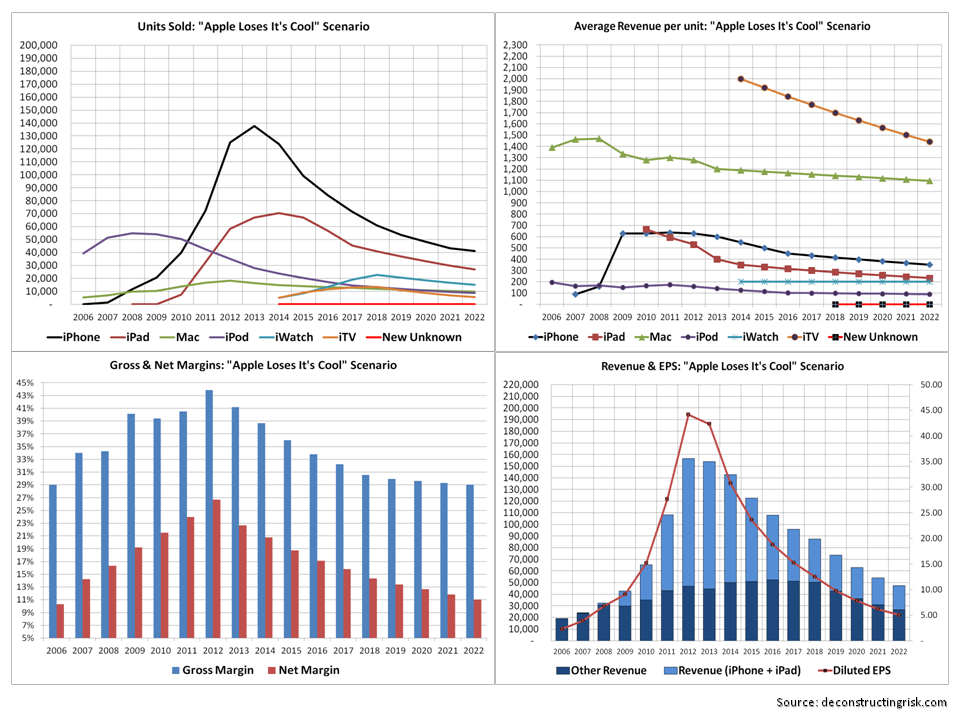

Scenario 1 – Apple Loses Its Cool

This scenario assumes the global mobile phone market grows at 2% annually and the Smartphone market grows from the currently approximate 50% of the mobile market to 70% by 2017. The iPhone sales are assumed to peak in 2013 at 137 million units and decrease thereafter at an average of 12% per year with the decrease peaking in 2015 at 20%. This represents a peak market share of 18% in 2012 to 3% by 2020 and a 3% share thereafter. Average revenue drops from $620 in 2012 to $450 by 2016 (as a result of the introduction of lower cost iPhones and a wider model range) and by 4% per year thereafter. Gross margins drop from the current mid 50% to below 50% by 2015 and by 2% a year thereafter until it reaches 40%. Revenues peak at $82 billion in 2013 falling to $30 billion by 2017 and to $15 billion by 2022.

iPad sales are assumed to peak in 2014 at just over 70 million units falling steadily to 27 million by 2022. Revenue per unit falls dramatically from $530 in 2012 to $330 by 2015 and $230 by 2022. Gross margins fall from 30% in 2013 to 25% in 2022.

Mac desktop & laptop products fall from approximately 18 million units in 2013 to 10 million by 2020. iPods also fall from 4 million in 2013 to below a million by 2021. Average revenue falls for each product steadily and gross margins fall modestly.

It is assumed that two new products – the iWatch and the iTV – are introduced with limited success. Both products start with 5 million of sales each. The iWatch reaches a peak of 23 million by 2018 before falling off to 15 million by 2022. Average revenue of $200 for the iWatch is assumed with a gross margin of 30% falling by 1% a year thereafter. The iTV reaches a peak of 13.5 units by 2018 before falling off to less than 7 million by 2022. The average revenue starts at $2,000 and falls by 4% annually. The gross margin starts at 30% and falls by 1% a year until it reaches 25%. Based upon an approximate global market of 250 units annually, Apple only manages to reach a peak of 5% market share by 2017 (assuming constant annual sales of 250 units). This scenario assumes that the iWatch is a niche product and the iTV only has limited success with core Apple users.

No other products are assumed to be introduced after 2014. This scenario therefore could reflect the situation where, after unsuccessful product launches and a drop in core markets, Apple essentially becomes a fallen company where management (likely to be new management) simply runs off the company to maximise cash-flow.

Overall revenue falls from over $150 billion in 2013 to under $50 billion by 2022. Gross margins fall from 41% in 2013 to 30% by 2019. Diluted EPS of above $42 in 2013 fall steadily to $5 by 2022.

(click to enlarge)

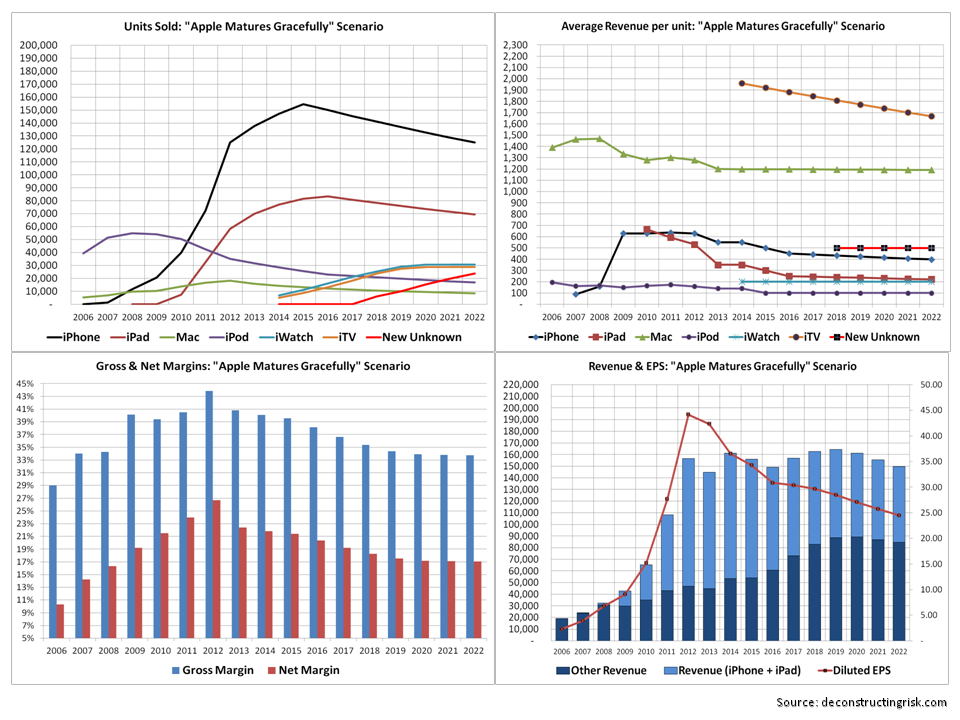

Scenario 2 – Apple Matures Gracefully

This scenario assumes the iPhone sales peak in 2015 at 155 million units and decrease thereafter by approximately 5 million annually to 125 million by 2022. This represents a peak market share of 18% in 2012 to a steady 9%-8% by 2018 and thereafter (assuming 2% average annual mobile market growth and 70% Smartphone share by 2017). Average revenue and gross margin drops as per scenario 1. Revenues peak at $81 billion in 2013 falling to $50 billion by 2022.

iPad sales are assumed to peak in 2016 at 83 million units falling steadily to 70 million by 2022. Revenue per unit and gross margin falls dramatically from $530 in 2012 to $250 by 2016 and $220 by 2022. Gross margins fall as per scenario 1.

Mac products as per scenario 1.

It is assumed that two new products – the iWatch and the iTV – are introduced with relative success. The iWatch is introduced in 2014 and sells 7 million units in its first year with steady annual grow, reaching over 30 million by 2020. Average revenue of $200 for the iWatch is assumed with a gross margin of 30% falling by 1% a year thereafter. The iTV is also introduced in 2014 reaching 5 million sales in its first year. It grows steadily to just under 30 million units by 2020. The average revenue starts at $2,000 and falls by 2% annually. The gross margin starts at 30% and falls by 1% a year until it reaches 25%. Based upon an approximate global market of 250 units annually (and 2% annual growth), Apple reaches a 10% market share by 2019 and retains it thereafter.

This scenario also assumes a new unknown product is launched in 2018 – $500 unit price, 35% gross margin, 6 million sales in first year growing to 24 million by 2022.

Overall revenue oscillates from 2014 to 2022 in a range between $150 billion to $160 billion – with a peak of $164 billion in 2019. Gross margins fall from 41% in 2013 to 34% by 2019 & thereafter. Diluted EPS of above $42 in 2013 fall steadily to $25 by 2022.

(click to enlarge)

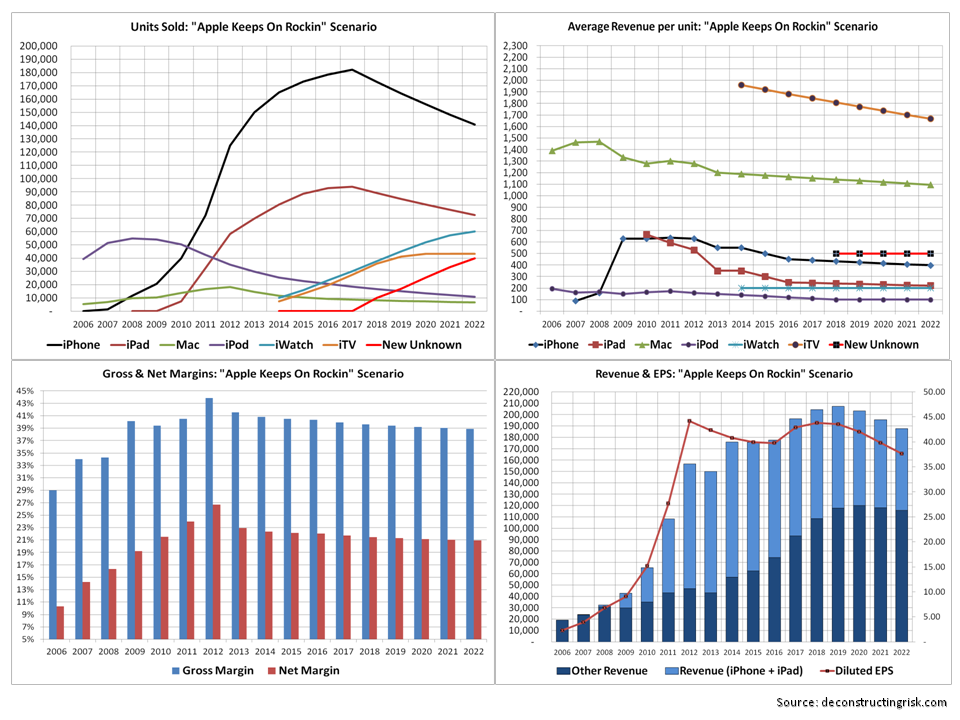

Scenario 3 – Apple Keeps on Rockin’

This scenario assumes the iPhone sales peak in 2017 at just over 180 million units and decreases gently thereafter to 140 million by 2022. This represents a peak market share of 18% in 2012 to a steady 10%-9% by 2018 and thereafter (assuming 3% average annual mobile market growth and 70% Smartphone share by 2017). Average revenue and gross margin drops as per scenario 1. Revenues peak at $91 billion in 2013 falling to over $70 billion by 2021.

iPad sales are assumed to peak in 2017 at 94 million units falling steadily to 70 million by 2022. Revenue per unit as per scenario 2 with gross margins constant at 30%.

Mac products as per scenario 1 with a steeper fall to approximately 7 million units by 2020 (given the strength of other products assumed move to hand held devices more extreme for PCs & laptops.

It is assumed that two new products – the iWatch and the iTV – are introduced with good success. The iWatch is introduced in 2014 and sells 10 million units in its first year with steady annual grow, reaching over 60 million by 2020. Average revenue of $200 for the iWatch is assumed with a gross margin of 30% falling by 1% a year thereafter. The iTV is also introduced in 2014 reaching 7.5 million sales in its first year. It grows steadily to just under 40 million units by 2019. The average revenue starts at $2,000 and falls by 2% annually. The gross margin remains at a very solid 40% throughout. Based upon an approximate global market of 250 units annually (and assuming 3% growth), Apple reaches a 14% market share by 2019 and retains it thereafter.

This scenario also assumes a new unknown product is launched in 2018 – $500 unit price, 35% gross margin, 10 million sales in first year growing to 40 million by 2022.

Overall revenue grows to $207 billion by 2017 before dropping back to $190 billion by 2022. Gross margins remain strong at 42% for 2013, 41% in 2014, 40% for 2015 to 2018, and 39% thereafter. Diluted EPS range between $40 to $43 from 2013 to 2022.

(click to enlarge)

Valuation & Projections

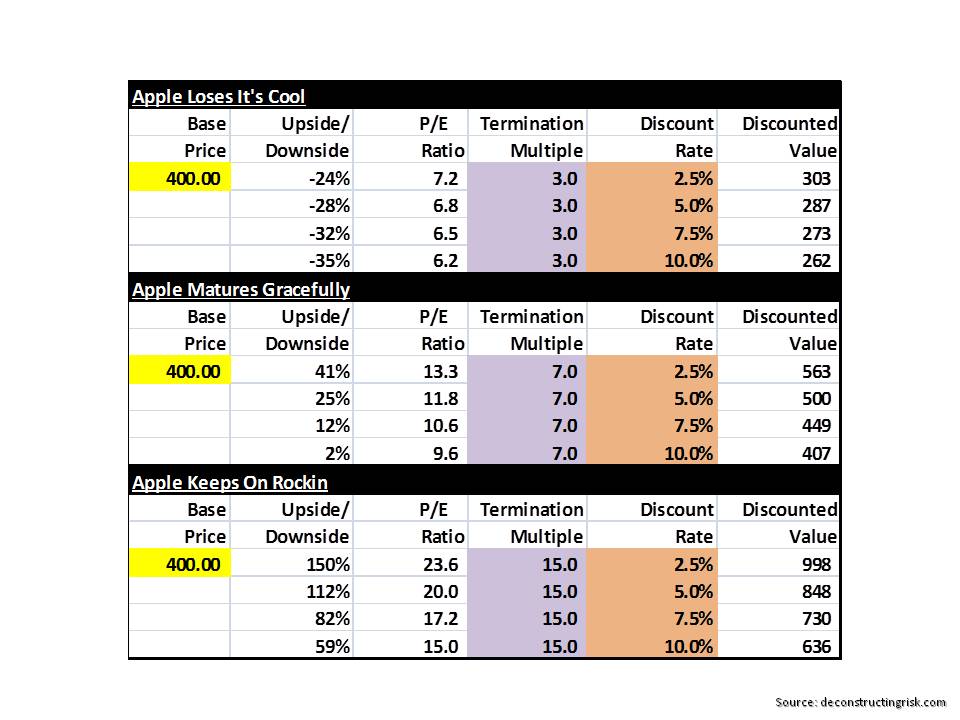

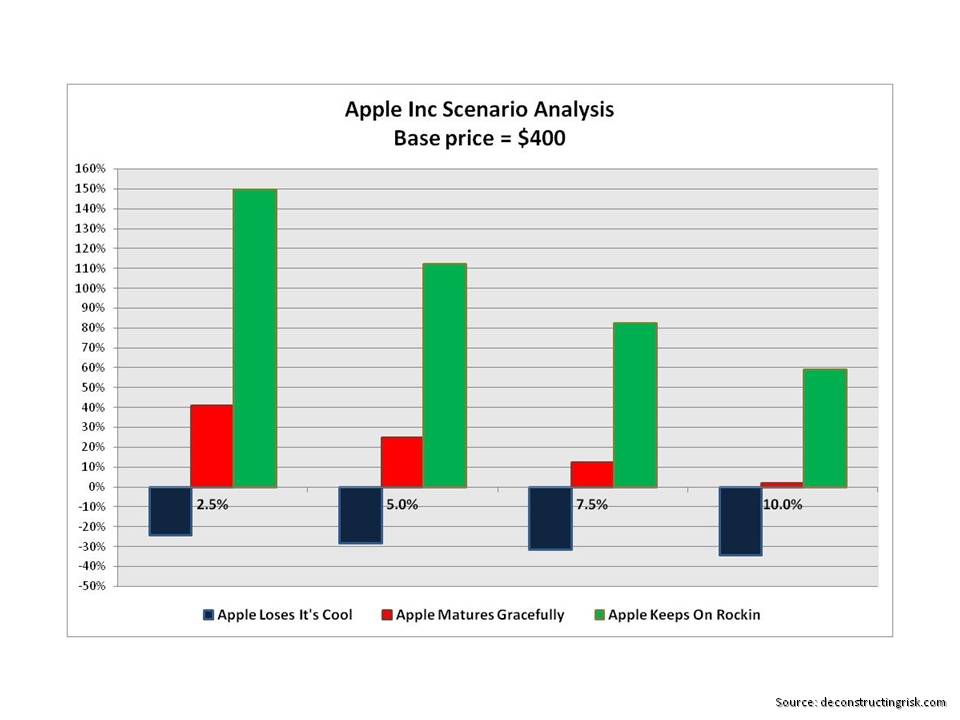

Cash-flows are projected over 10 years for 2013 to 2022 with a termination multiple applied to the discounted 2022 cash-flow. In any cash flow analysis, two key inputs are the discount rate and the termination value. The discount rate is normally tied to the weighted average cost of capital of a company. However, given the current reality detached risk premia in capital markets, I have simply used a variety of rates from 2.5% to 10%. For a company like Apple, given the rapidly changing nature of its market, my instinct says a rate higher than 5% and below 10% is a suitable range for Apple. Similarly, I have simply selected termination multiples based upon the characteristics of each scenario and what I believe is sensible. The results of the discounted cash flow analysis are below (click items to enlarge).

Conclusion

As stated above, the purpose of this analysis is to get a range of possible

valuations for Apple. I like to focus on downside and somewhere around a 30%

downside looks realistic here from $400 per share. One thing is clear, that as Apple enters a phase of reduced growth compared to recent years, the stock price will be volatile. The jitters concerning the Q2 results is simply a symptom of the market trying to figure out the new trajectory for Apple. If Q2 results show a gross margin below 40% and revenues just around expected, I can see the stock price dropping further. Until there is some visibility into the new product line, gross margins and average product revenue, I don’t expect to see any massive upside in AAPL (assuming the market doesn’t go off on one). That visibility is not likely until the latter half of 2013. My initial focus is on the upside and downside dynamics using the 7.5% discount rate which also suggests that there is no need for urgency in jumping into AAPL now. I am tempted to put a small position, between 10%-20% of my possible overall allocation, to average into any position although the analysis herein suggest that many of the current issues surrounding AAPL will remain unanswered come Wednesday.