That markets often behave irrationally, particularly over the short to medium term, is generally widely accepted today. Many examples can be cited to show that human behaviour does not restrict itself to the neo-classical view of rational player’s expected utility maximisation. The subject of the behavioural impact of humans in economics and finance is a vast and developing one which has and is the subject of many academic papers.

As a result of a recent side project, I have had cause to dig a little bit deeper into some of the principles behind behavioural economics and finance. In particular my attention has been caught by prospect theory, so named from the 1979 paper “Prospect theory decision making under risk” by Amos Tversky and Daniel Kahneman (who received a Nobel Prize in 2002 for his work on the subject), largely seen as the pioneers of behavioural economics and finance. In essence, prospect theory asserts that humans derive utility differently for losses and gains relative to a reference point.

My limited knowledge on the topic has been tweaked by a paper from Nicholas Barberis in 2012 entitled “Thirty Years of Prospect Theory in Economics: A Review and Assessment”. Although Barberis states that “while prospect theory contains many remarkable insights, it is not ready made for economic applications”, he highlights some recent research that may “eventually find a permanent and significant place in mainstream economic analysis.”

Tversky and Kahneman updated the 1979 original prospect theory in 1992 to overcome initial limitations, so called cumulative prospect theory, based upon four elements:

1) Reference Dependence – people derive utility from gains and losses relative to a reference point (rather than from absolute levels).

2) Loss Aversion – people are much more sensitive to losses rather than gains of the same magnitude.

3) Diminishing Sensitivity – people are risk averse in relation to gains (e.g. prefer certainty) but risk seeking in relation to losses.

4) Probability Weighting – people weight probabilities not by objective probabilities but rather by decision weightings (e.g. objective weightings transformed by their risk appetite).

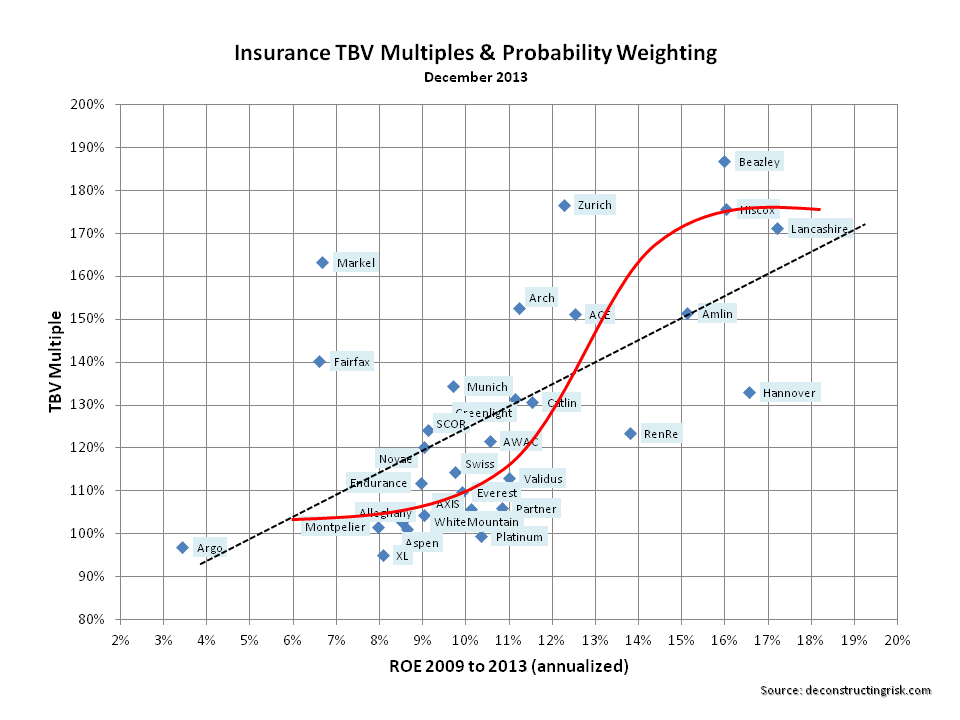

Graphically cumulative prospect theory is represented below.

click to enlarge

Barberis highlights a number of sectors where prospect theory, as a model of decision making under risk, has applications. I will only comment on areas of interest to me, namely finance and insurance.

Probability weighting highlights that investors overweight the tail of distributions and numerous studies confirm that positively skewed stocks have lower average returns than would otherwise be suggested by expected utility investors. In other words, investors overestimate the probability of finding the next Google. This explains the lower average return of classes such as distressed stocks, OTC stocks, and out of the money options.

Loss aversion has also been used to explain the equity premium compared to bonds (i.e. returns have to be higher to compensate investors for volatility). Using an assumption called “narrow framing” investors evaluate separate risks according to their characteristics. This has also been used to explain why many people don’t invest in the stock market.

Prospect theory is also used to explain one long standing failure of investor behaviour, namely selling winners too early and holding on to losers too long. This is something that I have learned from experience to my determent and one piece of advice that many professional investors emphasis again and again. This characteristic was highlighted in research as far back as 1985 in a paper by Shefin and Statman. Further research to formalise this “disposition effect” is on-going and much debated. Other research focuses on the impact of “realisation” utility when it comes time to sell a stock (e.g. we derive more utility in selling a winner).

In the insurance area, prospect theory has been used to explain consumers purchasing behaviour. For example, if we overweight tail events then we likely

purchase too much insurance, at too low a deductible! Purchasing of a product such as an annuity is also impacted by our mentality of being risk adverse on gains/risk seeker on losses. The consumer is therefore more sensitive to a potential “loss” on an annuity by dying earlier than expected as opposed to a “gain” by living longer. One area that has proven difficult in using prospect theory is to understand what reference point people use in making decisions such as the purchase of an annuity.

There have been recent criticisms on the use of behaviour theories in finance and economics. Daniel Kahneman himself, whilst promoting the paperback launch of his 2011 bestselling book “Thinking, Fast and Slow” expressed his frustration at the blasé labelling of a divergence of social science as behavioural economics – “When it comes to policy making, applications of social or cognitive psychology are now routinely labeled behavioral economics”.

Another recent report entitled “How Behavioural Economics Trims Its Sails and Why” by Ryan Bubb and Richard Pildes claims that some policymakers naive embrace of the new field may actually be doing more harm than good. The report states that “fuller, simpler, and more effective disclosure, one of the main options in behavioural economic’s arsenal, is not a realistic way, in many contexts, to rectify adequately the problems in individual capacity to make accurate, informed judgments with the appropriate time horizons.” The report cites examples such as opt-out options in automatic enrolment of retirement savings and disclosure on teaser rates in credit products that claimed to offer reasoned choices to consumers but ultimately led to unintended economic impacts.

It is ironic (and probably inevitable) that some features designed to modify behaviour backfire given that, in the words of behavioural economist Dan Ariely, the premise of the theory is that “we are fallible, easily confused, not that smart, and often irrational.”