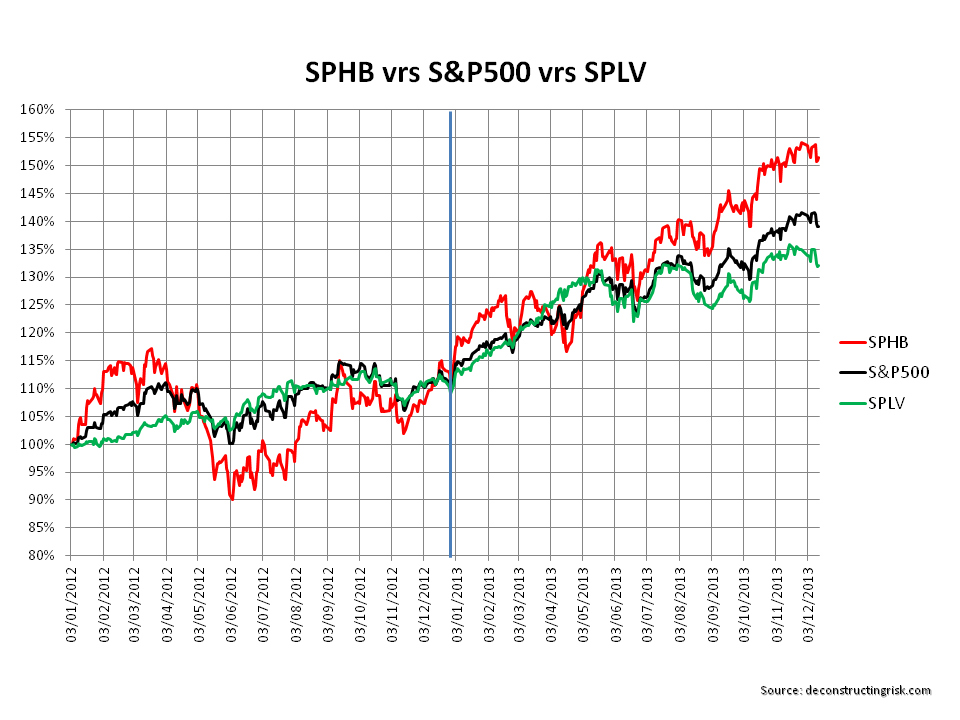

Following on from the last post on high beta delights, I had a look at a S&P high beta ETF (SPHB) against the S&P500 as well as a S&P low volatility ETF (SPLV) to test the assertion that the latest run in the market is a new phase whereby investors who missed out on early gains are taking on more risk in the form of high beta stocks to catch up. The two ETFs above have only been around since mid-2011 so I selected the start of 2012 until last Friday as the timeframe.

The graph below shows that the high beta ETF underperformed both the S&P500 and the low volatility ETF for most of 2012 (particularly after the May 2012 fall). For much of 2013 however, and particularly since June 2013, the high beta ETF has outperformed the S&P500 and significantly outperformed (by approx. 20%) the low volatility ETF. Also, since August the low volatility ETF has underperformed against the S&P500. This seems to confirm the assertion that investors are chasing returns and increasing risk.

click to enlarge

It’s a pity that no longer time series are available. Afaik researchers showed that high beta names tend to underperform the market whereas low beta names (however you measure beta… that would be an entire discussion on it’s own) tend to outperform. This effect has been attributed to performance chasing. Looks like this is the name of the game once more…

Eddie