The broker reports on the January renewals paint a picture of building pricing pressures for reinsurers and specialty insurers. The on-going disintermediation in the property catastrophe market by new capital market capacity is causing pricing pressures to spill over into other classes, specifically on other non-proportional risks and on ceding commissions on proportional business.

The Guy Carpenter report highlight that traditional players are fighting back on terms and conditions through “an extension of hours clauses, improved reinstatement provisions and expanded coverage for terror exposures” and “many reinsurers offered more tailored coverage utilizing options such as aggregate and quota share cover, multi-year arrangements and early signing opportunities at reduced pricing”. Guy Carpenter also point to large buyers looking at focusing “their programs on a smaller group of key counter-party relationships that were meaningful in relation to the overall size of the program”.

The Aon Benfield report and the Willis Re report also highlight the softening of terms and conditions to counteract cheap ILS capacity emphasising items such as changes in reinstatement terms. Willis states that “the impact of overcapacity has been most clearly evidenced by the up to 25% risk adjusted rate reductions seen on U.S. Property Catastrophe renewals at 1 January and the more modest but still significant rate reductions of up to 15% on International Property Catastrophe renewals”.

Following an increase in valuation multiples from all time lows for the sector over the past 24 months, the current headwinds for the sector as a result of over-supply and reduced demand mean, in my opinion, that now is a good time for investors to reduce all exposure to the sector and move to the side-lines. I particularly agree with a comment in the Willis report that “experienced reinsurers will remember that the relaxation of terms and conditions more so than price reduction caused the real damage in the last soft market cycle”. Meaningful upside from here just doesn’t look on the cards to me particularly when compared to the downside risks (even M&A activity is likely to be with limited premium and/or on an all stock basis).

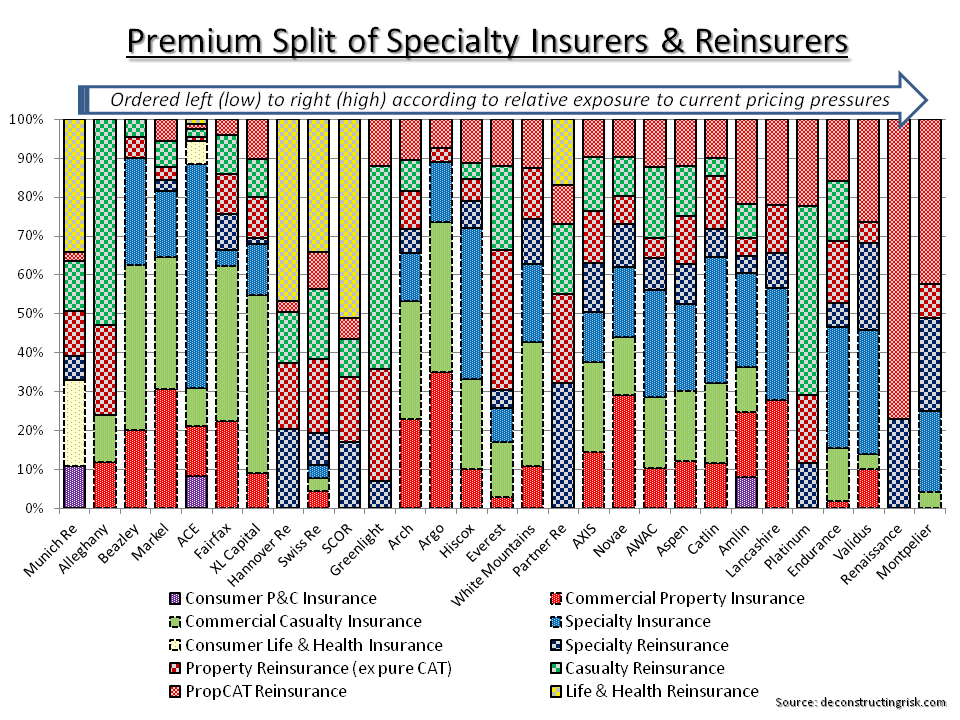

The graph below shows the premium split by main product line for the firms that I monitor. The firms have been sorted left to right (low to high exposure) by a subjective factor based upon exposure to the current pricing pressures. The factor was calculated using a combination of a market pricing reduction factor for each of the main business classes based upon the pricing indicated in the broker reports and upon individual business class discounts for each firm depending upon their geographical diversification and the stickiness of the business written. The analysis is fairly subjective and as many of the firms classify business classes differently the graph should be considered cautiously with a pinch of salt.

click to enlarge

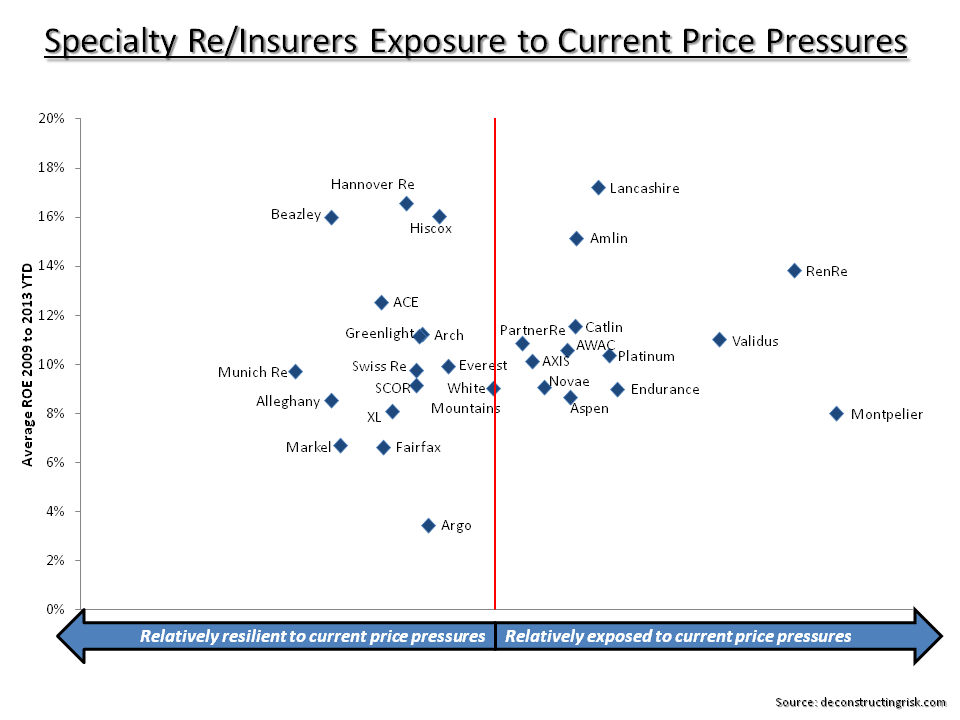

Unsurprisingly, reinsurers with a property catastrophe focus and with limited business class diversification look the most exposed. The impact of the reduced pricing on accident year ratios need to be combined with potential movement in reserves to get the impact on calendar year operating results. Unfortunately, I don’t have the time at the moment to do such an analysis on a firm by firm basis so the graph below simply compares the subjective pricing factor that I calculated against average operation ROEs from 2009 to Q3 2013.

click to enlarge

As stated previously, the whole sector is one I would avoid completely at the moment but the graph above suggests that those firms on the right, specifically those in the lower right hand quadrant, are particularly exposed to the on-going pricing pressures.

How are the business cycles in the primary insurance market and the reinsurance market correlated ? I remember reading that rates in the primary insurance market were grinding higher last year, somewhere in the single digit percentage point area. Thus I had the impression that times are getting a bit better for primary insurers (the Allianz and to some extent the Markels of this world). Whereas you say that reinsurers and to some extent specialty insurers are setting themselves up for a big fat whammy. Is there any type of co-movement in rates ?

I really like “experienced reinsurers will remember that the relaxation of terms and conditions more so than price reduction caused the real damage in the last soft market cycle”. This reminds me of so called covenant lite loans which were popular in 2006/2007 and are again popular now. Basically loans to low rated companies but without most of the protective clauses. I leave the results of this experiment to your imagination…

Best,

Eddie

Hi Eddie,

Yep the US commercial rates have been on the up (back to around 2001 rates) as per graphs from Aon Benfield report on page 7 & 8. The issue here is that the reinsurers are having to increase the commissions to the reinsureds for proportional coverage so the reinsurers have the same downside for less upside!!

The Excess & Surplus (E&S) market and Lloyds are more competitive (these are where Berkshire are moving into) and subject to spill over from overcapacity in the reinsurance market. The chunky risks in these markets with big premiums are the ones that most open to the ILS guys coming in and converting the premiums into coupons.

The more protected firms are those with smaller sticky business that is not as price sensitive to the big risks that go into the subscription market.

Covent lite debt provisions is a good metaphor for the relax in t&c under way in reinsurance. Its just starting but it could get ugly….

I will post a few graphs on the cycle between the US P&C market, Lloyds and the reinsurance market.

Best,

M

Thanks, that helped. I just read the abstract of the Aon Benfield report and started to shiver. Hefty price decreases, new features that cannot be hedged (ie offloaded)… we have been there before.

Can you explain me what is meant by “relaxed hours clauses” ? I googled but to no avail.

Best,

Eddie

I just went through the reports you provided. My first impression: more than enough capacity and new players almost everywhere. Looks like the dumb money is joining the party…

Eddie

Eddie,

Hours clause restrict the claims from one event to a specified period, generally 72 hours. so by pushing it out you may get more claims from one event. Most catastrophes do their damage within 72 hours. Some storms could hit land and go back out to sea & hit land again over a longer timeframe. Biggest uncertainties generally are over earthquakes and after-shocks which can cause more damage than initial tremors (by the way, it looks like quake risk is the most under-priced in the market). So events that previously may be cast as two events could now become one, increasing severity.Generally a sign that traditional reinsurers are fighting back against ILS by offering wider coverage and more optionality (for free!!).

Not too sure if the new capital is dumb. It does look like it is here to stay (until a re-pricing of risk across capital markets anyway). I think they know what they are doing but are desperate for yield and their models leverage the low risk adjusted returns from ILS due to the lack of correlation between financial assets and event driven assets. Why it provides more upside that simply including the equity of event driven (re)insurers is beyond me but I suspect its down to some quant black box giving over generous diversification benefits in their portfolios using correlations picked out of the sky….

A.

Thanks.

I don’t know the insurance market too well but I would assume that experience is a clear plus when underwriting new deals. Since we are talking about events that occur rather unfrequently and have a high degree of variability when it comes to severity I have the impression that it clearly helps if you have seen a couple of things. Models carry you only so far, sometimes you have to make adjustments beyond what you model says. This is my experience from the credit market at least.

So it might be the case that some players that currently enter the market are more model-driven than it is good for them. Unfortunately it takes a couple of years to realize that. By then it is probably too late. That is what I meant by “dumb money”. You can observe similar behaviour in HY credit for example. Once the Oaktrees of this world tighten up you better run for cover…

Eddie