The onset of a wobbly tooth from a year old crown caused me to have a look at Sirona Dental Systems (SIRO) again. I last blogged on it in August 2014 here. SIRO has had a good run since then moving from around $80 to $109 today. The recent increase is due to the announcement in September of a merger of equals with DENTSPLY which is expected to close in Q1 2016.

SIRO, with 65% of its revenues outside of the US, felt the impact of the dollar strength with flat line revenue growth in 2015 (year ending in September). In local currencies, SIRO achieved 9.8% growth which was broad based across the US and international markets with respective growth at 9.2% and 10%. Despite the FX headwind, and a volatile Q2, operating margins were impressive, as the graph below shows. Operating cash-flow after capital expenditure has also been strong closely running at approximately 65% of operating income.

Click to enlarge

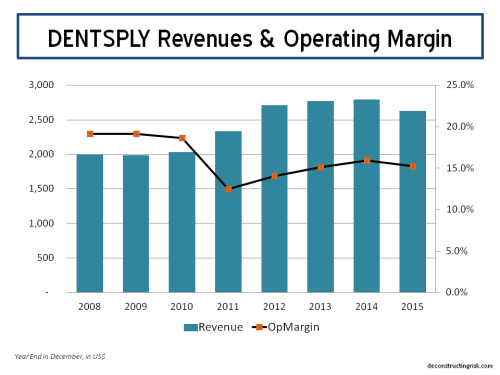

DENTSPLY (ticker XRAY) is a larger company in revenue terms with lower operating margins and a focus on dental consumable products. Dental specialty products such as endodontic (root canal) instruments and materials, implants and related products, bone grafting materials, 3D digital scanning and treatment planning software, dental and orthodontic appliances and accessories make up approximately 50% of revenues. Dental consumable products such as dental anesthetics, prophylaxis paste, dental sealants, impression materials, restorative materials, tooth whiteners and topical fluoride make up approx 30% of sales. The rest of sales are split between dental laboratory products and consumable medical device products. Geographically DENTSPLY also sells its products globally with 65% outside the US. DENTSPLY’s historical results (with assumed Q4 to December for 2015) are as below and the net cash-flow profile of DENTSPLY relative to operating income is similar to SIRO in recent years.

Click to enlarge

The investor presentation on the merger highlights further details. One interesting angle on the investment thesis is that the combined company is a good play on the aging population trend in the developed world. The $21 billion global dental market (of which the merged firm will have approximately 18%) is represented at increasing one to two times GDP. The plan also allows for a $500 million share buy-back programme post-closing with $125 million of operating costs savings (or approx 3% of operating margin based upon combined revenues) expected.

SIRO has approximately $500 million in cash with little debt. Goodwill and intangibles make up approximately 40% of SIRO’s total assets. DENTSPLY on the other hand has approximately $230 million in cash with $700 million in debt. Goodwill and intangibles make up nearly 60% of DENTSPLY’s total assets.

Based upon 5% top-line growth, my rough estimates for 2016 for the combined entity are a 21% operating margin post savings or approximately $830 million of operating income and $560 million of net income. Assuming 250 million shares (not taking the buy-back into account) I estimate an EPS of approximately $2.40. These are real back of the envelop calculations so I would caution against any rash conclusions. They do indicate a 25 times multiple of XRAY’s current share price around $60 which looks to me stretched given the integration risks. Still it’s a name for the watch list to monitor and wait for a better entry point.

In the meantime, it’s back to the dentist with this wobbly tooth.