Following on from a recent post on windstorms in the US, I have taken several loss preliminary estimates recently published by firms (and these are very early estimates and therefore subject to change) and overlaid them against the South-East US probable maximum loss (PML) curves and Atlantic hurricane scenarios previously presented, as below. The range of insured losses for Harvey, Irma and Maria (now referred to as HIM) are from $70 billion to $115 billion, averaging around $90 billion.

click to enlarge

The loss estimates by firm depend heavily upon the risk profile of each. As a generalisation, it could be said that the aggregate US wind losses are averaging around the 1 in 100 loss level.

Given there was over $20 billion of insured losses from H1 and factoring in developing losses such as the Mexico earthquake, the California wildfires and the current windstorm Ophelia hitting Ireland, annual insured losses for 2017 could easily reach $120 billion. The graph below shows the 2016 estimates from Swiss Re and my $120 billion 2017 guesstimate (it goes without saying that much could still happen for the remainder of the year).

click to enlarge

At a $120 billion level of insured loss for 2017, the 10 year average increase from around $55 billion to $65 billion. In a post in early 2016, I estimated that catastrophe pricing was about 25% too low based upon annual average losses of $40 billion per year. We will see whether the 2017 losses are enough to deplete the overcapitalisation in the market and return pricing towards their technical rate. I wouldn’t hold my breath on that as although there may be material aggregate losses in the private collateralised market and other pockets of the retrocession market, the appetite of yield seeking investors will likely remain unabated in the current interest rate environment.

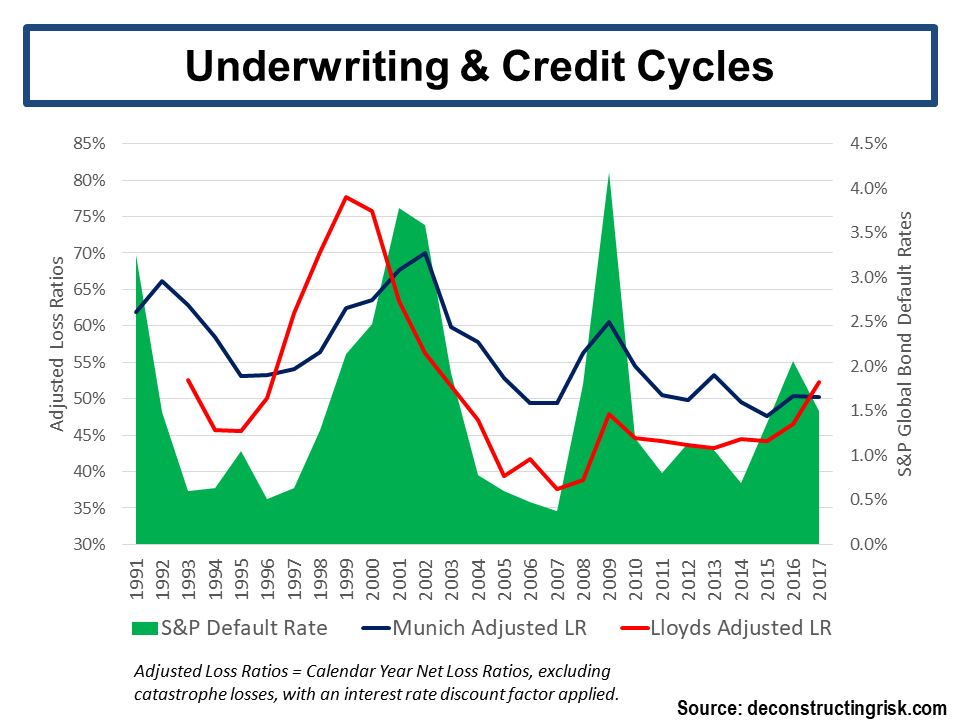

Although the comparison between calendar year ratios and credit defaults is fraught with credibility issues (developed accident year ratios to developed default rates are arguably more comparable), I updated my previous underwriting cycle analysis (here in 2014 and here in 2013). Taking the calendar year net loss ratios of Munich Re and Lloyds of London excluding catastrophe and large losses (H1 results for 2017), I then applied a crude discount measure using historical risk-free rates plus 100 basis points to reflect the time value of money, and called the resulting metric the adjusted loss ratio (adjusted LR). I compared these adjusted LRs for Munich and Lloyds to S&P global bond credit default rates (by year of origin), as per the graph below.

click to enlarge

This shows that the years of relatively benign attritional claims together with the compounding impact of soft pricing over the past years may finally be coming to an end. Time will tell. All in all, it makes for a very interesting period for the market over the next 6 to 12 months.

In the interim, let’s hope for minimal human damage from the current California wildfires and windstorm Ophelia.

Latest news was that Ophelia is the worst storm during the last 50 years, so I hope that human damage will be limited. Property damages may pose an interesting challenge for the reinsurance and cat bond markets, though. But I doubt (right now at least) that this is already enough to bring some sense into the markets…

Eddie