I have been doing some digging into the dynamics of betting exchanges, the largest and best known of which is BetFair. The betting and gaming sector itself has been the subject of a mountain of academic research, there is even a journal dedicated to it! Quants have moved in and are actively pitting their algorithms against human gambling behaviour on the exchanges. A recent intriguing Bloomberg article on tennis betting illustrates some strategies now common in the marketplace.

Technology has driven disruptive disintermediation across many sectors such as the travel & airline industry and more recently across the retail sector. There was a fascinating documentary on the BBC by Robert Preston late last year on the UK retail sector which concluded that the future for many clothing retail outlets would be to act like galleries for consumers to peruse items with the ultimate purchase decision being made online.

The betting and gaming sector is one undergoing structural changes due to the massive increase in online activity. Additional competitive threats from disintermediated business models such as betting exchange pose interesting questions for the sector. Such structural market changes may be useful in understanding the impact of new business models in other sectors such as financial services – peer to peer (P2P) lending in banking or the ILS market in insurance come to mind. On the growing P2P lending sector, there was an article on the front page of Friday’s FT on how a UK developer sourced £4 million of debt through online P2P platform Lendinvest which may prove to be defining moment of change. On the impact of the ILS market, there was another interesting FT article that contended that the ILS market is resulting in structural changes in a market with “a lot of excessive overhead, ie highly paid staff, that can be eliminated”.

Before looking deeper into structural changes in the betting and gaming sector, I needed to understand the “traditional” betting market better. Besides the odd poker tournament (with real people), I am not a gambler and therefore not a user of the services provided by betting firms. I know enough that the odds are obviously in the bookies favour but I know very little about the economics of the betting industry. As such, this post details my research on the UK betting industry. A follow on post will go into the broader picture and some (likely rambling) thoughts on the impact of structural changes from betting exchanges like Betfair.

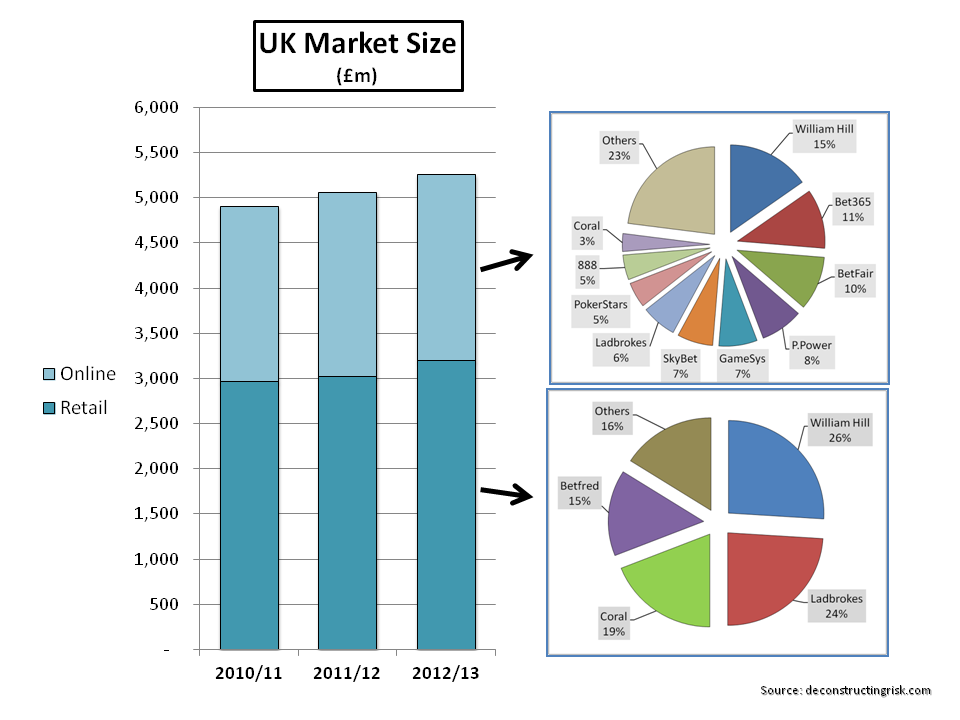

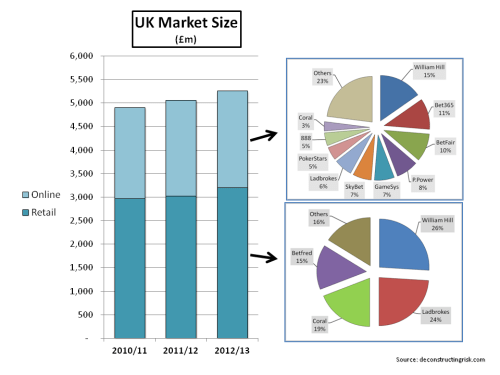

So, I concentrated on the UK market where data is freely available. The graphic below outlines the size of the UK betting and gaming market with the main providers. The market is split by revenue approx 60% retail and 40% online. The retail market is split approx 50:50 between over the counter betting at shops and gaming on machines (aka fixed odds betting terminals or FOBTs). On the online side, sports betting (commonly referred to as the Sportsbook) is approx 40% with gaming making up the remainder, led by casino (approx 30%), poker and bingo (approx 15% each).

click to enlarge

The main players on the retail side stress the advantages of their multi-access models and, to counter the impression that retail betting shops attach the older demographic, cite statistics that show even younger customers often use retail outlets (more and more in combination with online and mobile).

The gaming machine/FOBT sector has come under renewed focus recently. Derek Webb, a successful gambler, is one of the principles behind the Campaign for Fairer Gambling and has described the machines as “crack cocaine”. Campaigners point to the rapid rise in revenue from FOBT, which were only widely introduced in the early 2000s, the addictive nature of the machines and that users are high frequency gamblers with a concentration amongst younger men with low incomes. Bookies point to the high payouts (the margin taken by the bookmaker is generally about 3% to 4% of the amount staked whereby such margin is referred to as the gross win) and the importance of machines supporting the retail shop model (I estimate that FOBT can contribute 70% to 80% of retail operating profits). Political pressure is mounting to restrict the amount that can be bet on the machines and JP Morgan recently cut its rating on Ladbrokes and William Hill saying that the likely change “could make the bottom 20pc of Ladbrokes and William Hill shops loss-making, with a further 20pc only marginally profitable, and require significant restructuring to close shops in order to cut costs.”

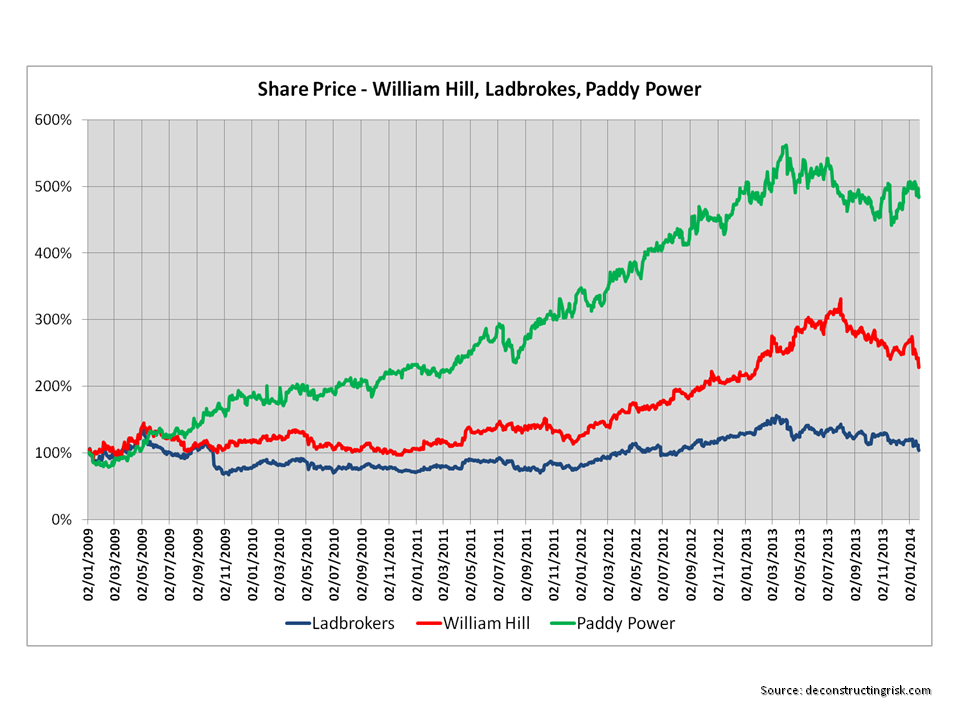

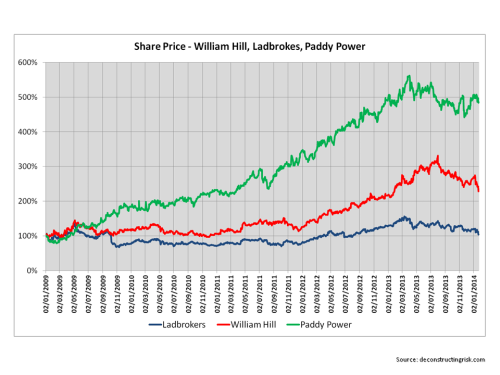

I selected Ladbrokes, William Hill and Paddy Power as firms to do some deeper analysis. William Hill and Ladbrokes are long established firms, particularly in the retail sector. William Hill is also the market leader in the online sector with a particular strength in online casino gaming. Paddy Power is the new kid on the block growing aggressively in online, particularly over the past 5 years, from its Irish base into the fourth largest in the online sector. Size wise, William Hill and Ladbrokes had revenue of £1.3 billion and £1 billion in 2012 respectively while Paddy Power had 2012 revenue of €650 million (approx £570 million). It would have been interesting to have a deeper look at the online only Bet365, which was founded in 2000 by Denise Coates and is now the number 2 in the UK online market with over £200 million in revenue, but unfortunately Bet365 is private. The graph below shows the share price moves of the selected firms since 2009.

click to enlarge

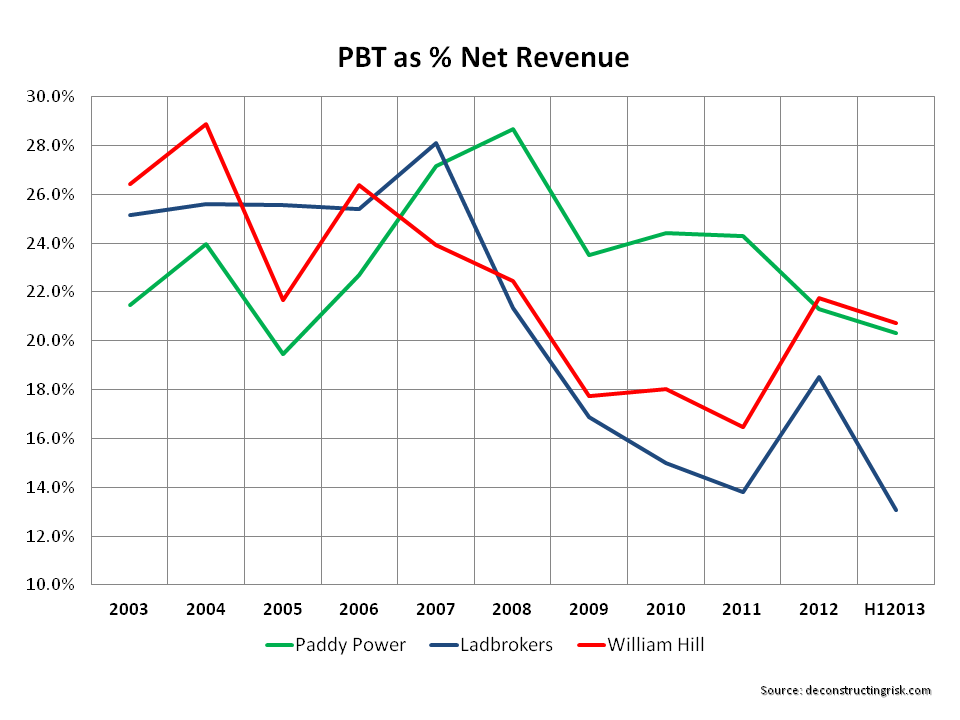

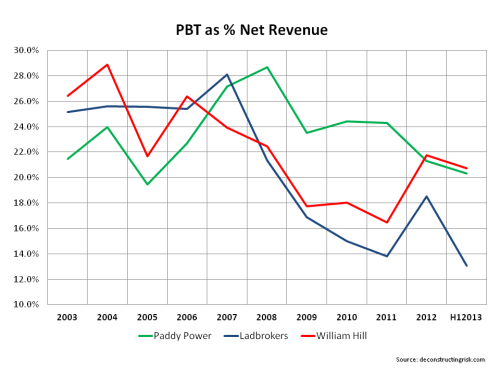

The graph below shows the profit before tax margins of the firms since 2003. As can be seen, profit margins have been under pressure, particularly for Ladbrokes in recent years.

click to enlarge

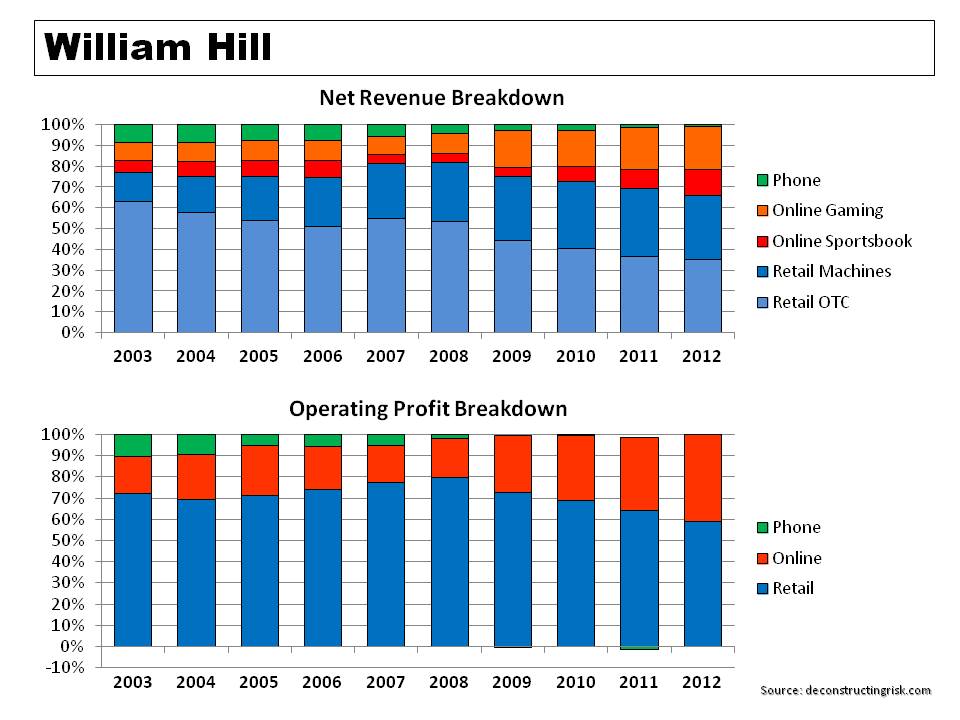

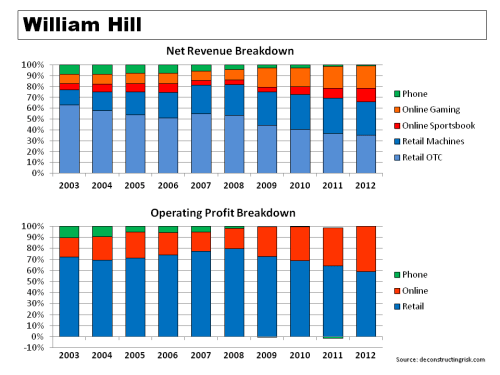

Revenue and operating profit breakdown for William Hill is below.

click to enlarge

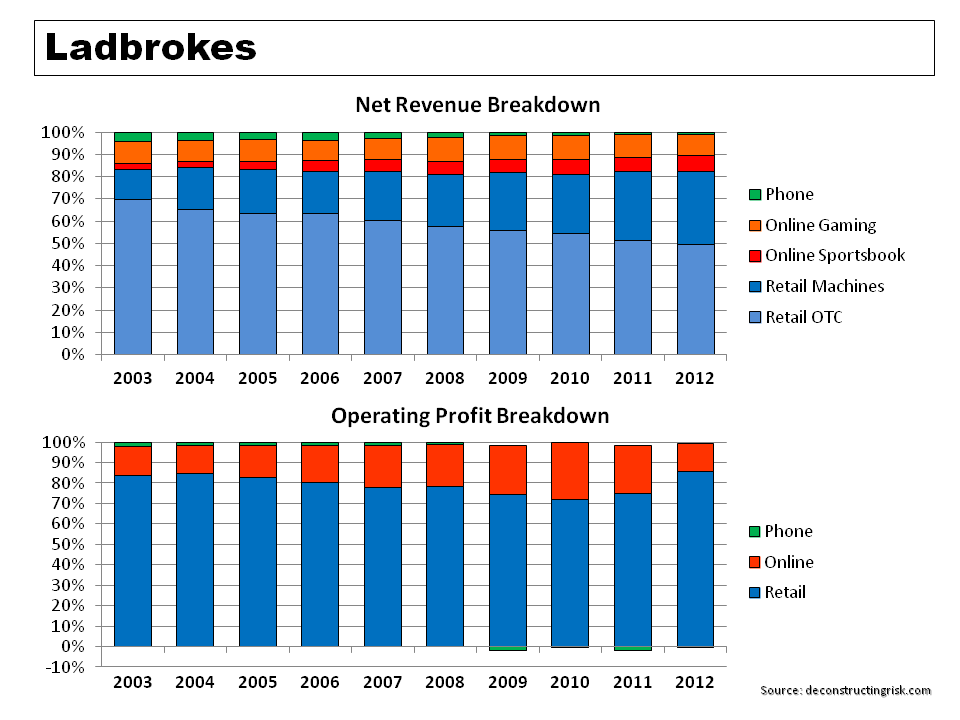

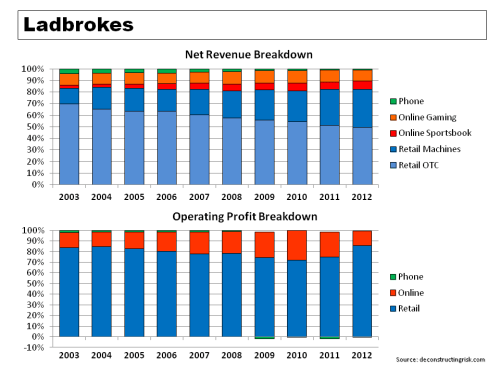

Revenue and operating profit breakdown for Ladbrokes is below.

click to enlarge

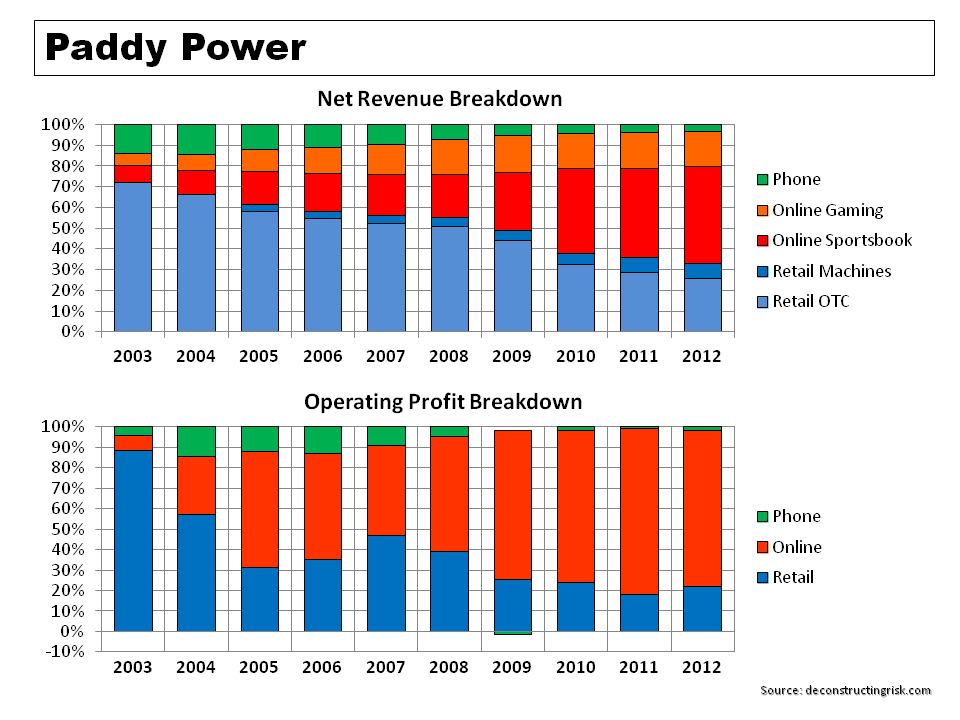

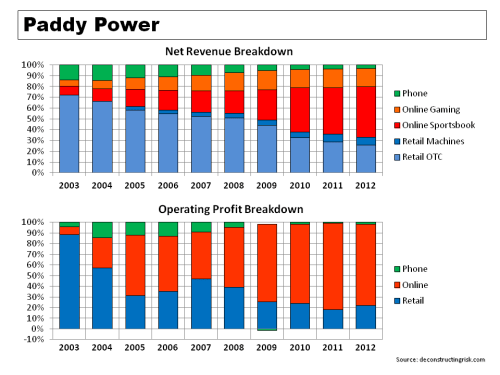

Revenue and operating profit breakdown for Paddy Power is below.

click to enlarge

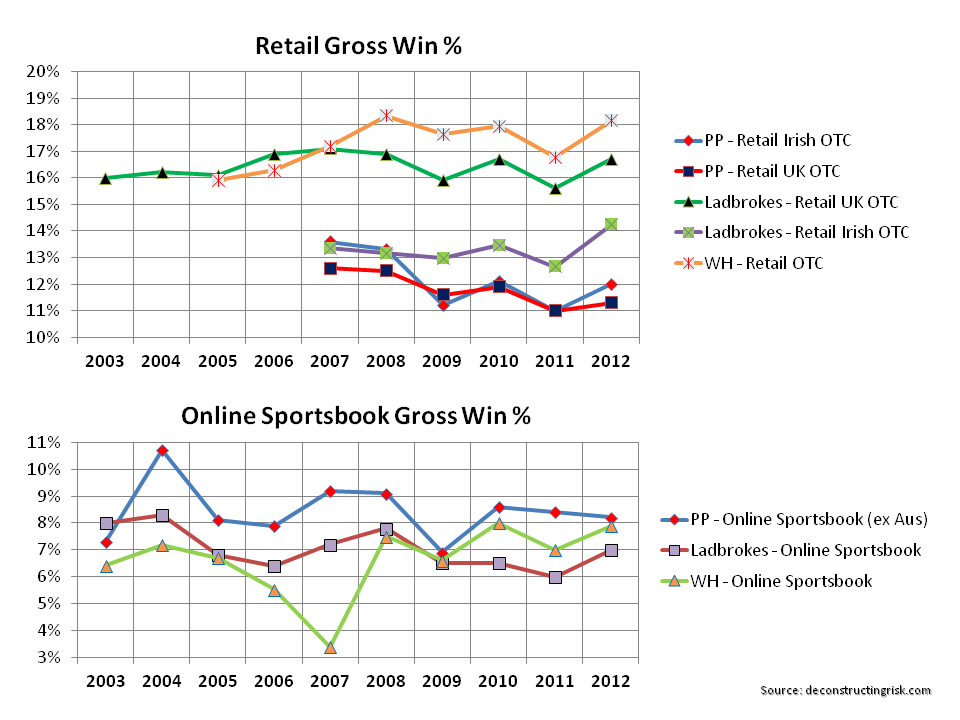

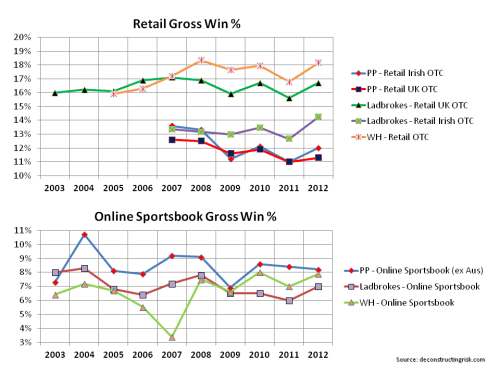

As mentioned above, the percentage that a bookmaker takes as a margin in each business is called the gross win (another commonly used term is the overround which refers to the excess above the sum of the odds). Net revenues are gross wins less VAT and fair-value adjustments for free bets, promotions and bonuses. Care needs to be taken when comparing gross win percentages (i.e. gross win divided by amounts staked) across firms as the make-up of the underlying books is important (gross wins varies by sport type such as football, horses, tennis, etc and by geography). Also items such as betting levies and charges vary and some are not deducted in the gross win to net revenue calculations but rather in operating expenses. Items such as the new UK point of consumption (POC) tax that is due to be introduced later this year also need to be understood in their potential accounting treatment. The graph below compares the reported gross win percentages amongst the firms in the retail over the counter (OTC) business and in the online Sportsbook businesses for the firms.

click to enlarge

I have found it difficult to get metrics for the profitability of both the retail and the online gaming businesses. As discussed above on the FOBT business, the operating profit contribution from gaming can be significant. I suspect that online gaming also contributes significantly to the online operating profit although not as high as the 70% to 80% contribution that I estimated for the retail business

Online gaming is also a more cross border business and is the fastest growing segment of the gambling industry. H2 Gambling Capital, a leading supplier of data and market intelligence on the global gambling industry, puts the size of the global online gaming market at approx $30 billion. Large markets such as the US are seen as ultimately providing a massive opportunity for growth once regulatory issues are resolved. Although firms withdrew from the US in 2006 after the passing of the Unlawful Internet Gambling Enforcement Act (UIGEA), individual States such as Nevada and New Jersey are looking at ways that they can approve online gaming and challenge federal restrictions.

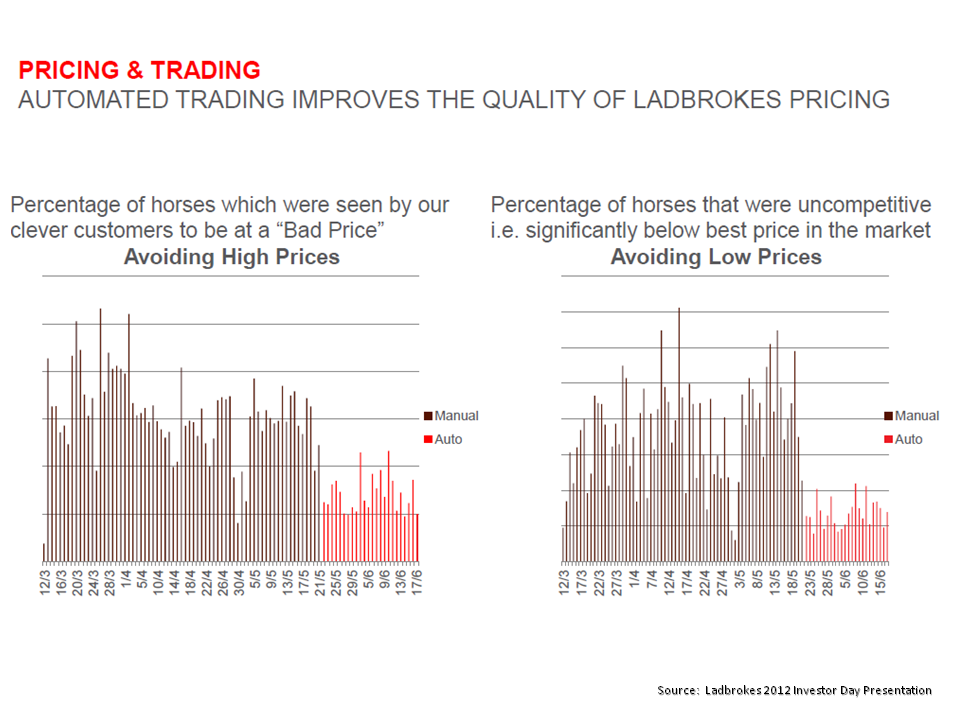

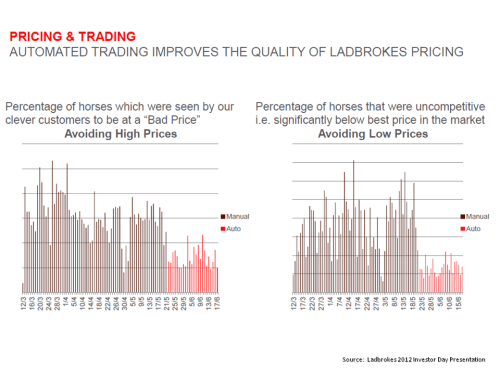

Although the established firms like William Hill and Ladbrokes are facing headwinds in their business with significant competition from online upstarts like Paddy Power, Bet365 and Betfair, they have size and powerful brands on their side. Both have made significant investments in IT infrastructure to support their business. The area of liability management is one that is particularly interesting. Ladbrokes, for example, has made significant investment in enhancing their trading abilities through the development of Morse, their own algorithmic robot. They cite the use of Morse in improving pricing which is particular important in the growing bet in play (BIP) market, as the exhibit shows.

click to enlarge

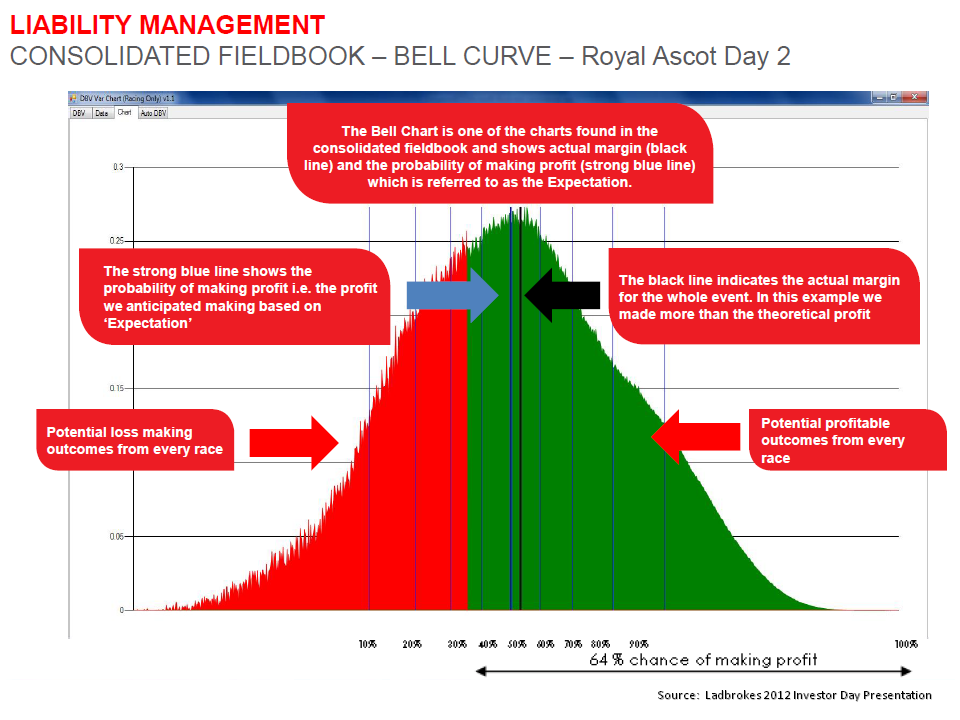

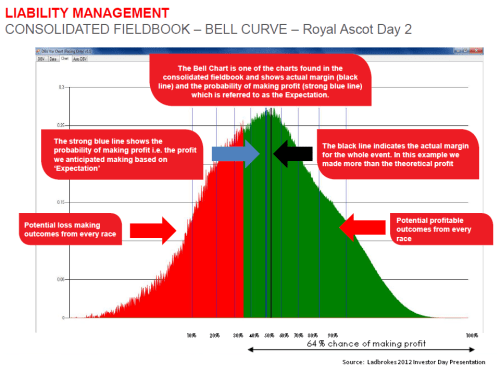

They also cite the use of such active liability management tools in improving outcomes such as the Royal Ascot results below.

click to enlarge

Changes in the whole betting and gaming sector have been rapidly evolving over recent years. These changes and the impact of betting exchanges will be the subject of a follow on post with some further musings in the coming weeks.