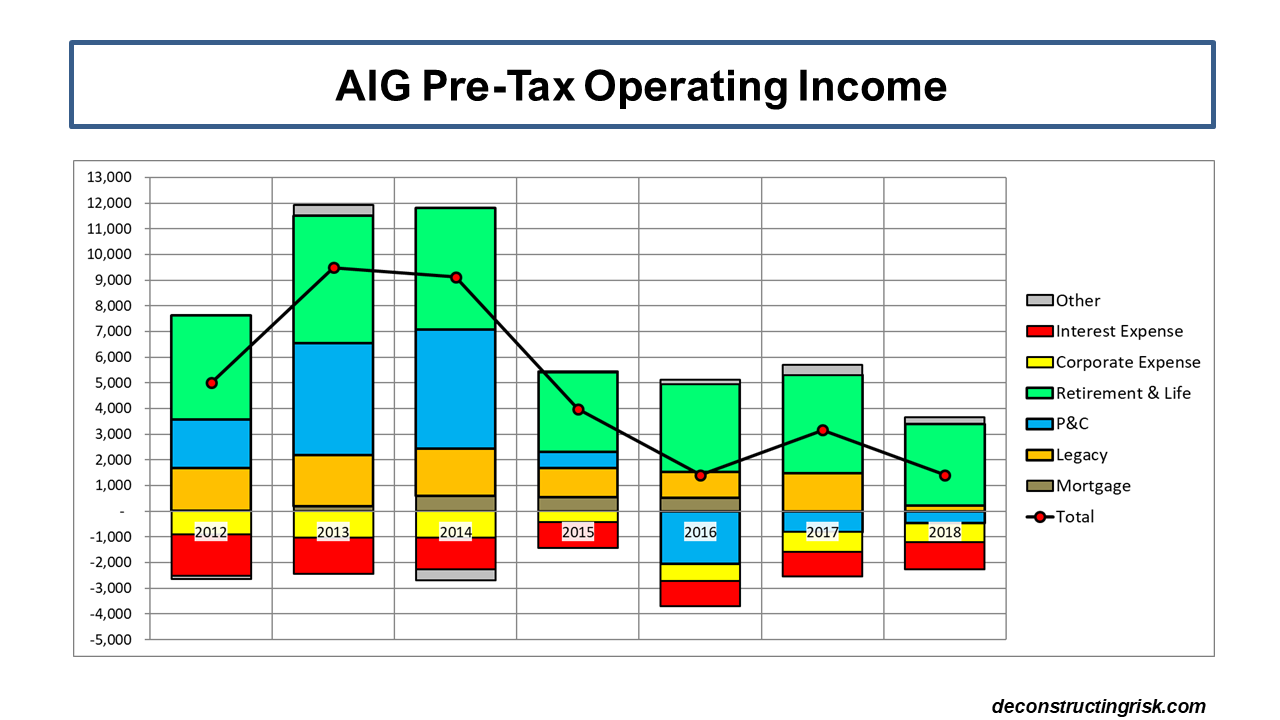

It’s been 2 years since I posted on AIG and it has been an eventful 2 years. A new management team (again) has been installed, led by industry veteran Brian Duperreault, to try to turn this stubborn ship around. The results, as below, show the scale of the task. Reduced investment returns, reducing legacy and asset balances, and poor reinsurance protections are just a few of the reasons behind the results, in addition to the obvious poor underwriting results.

click to enlarge

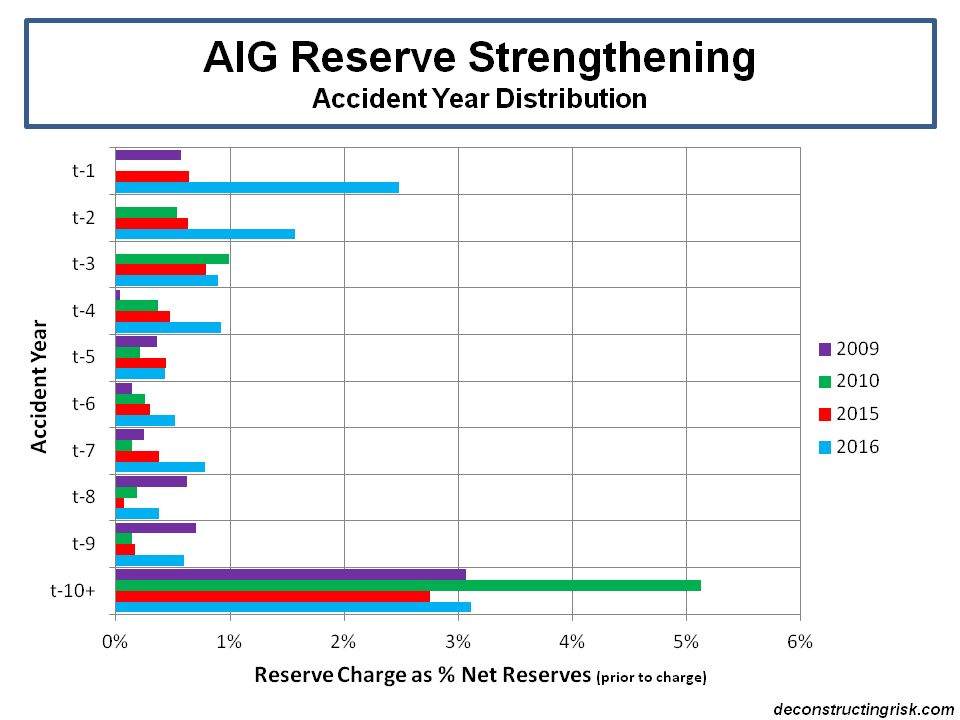

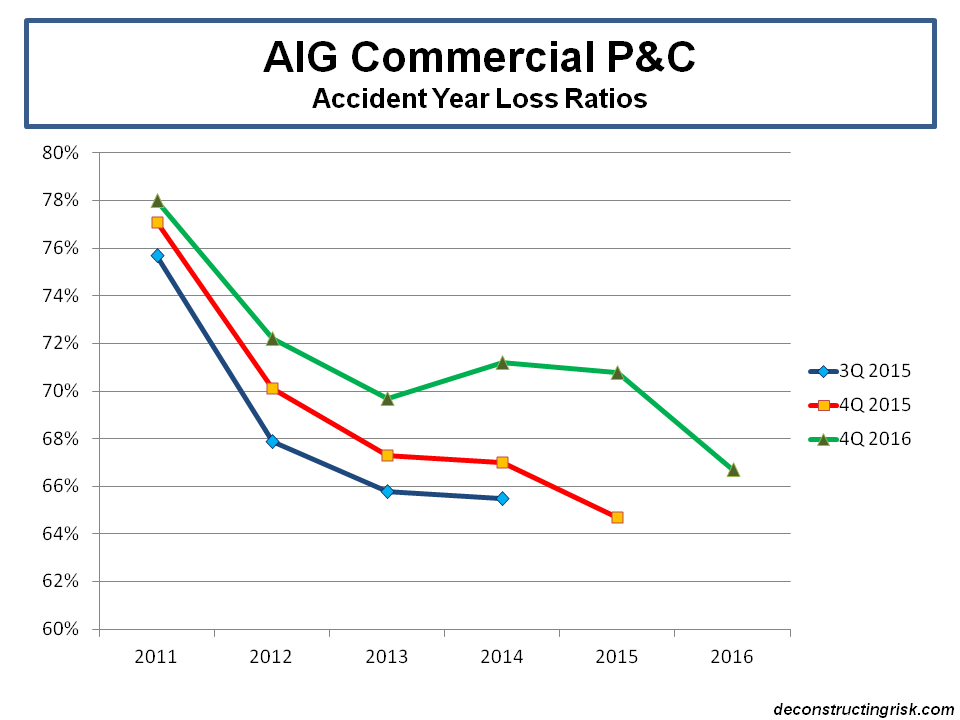

Oversize risks from the previous Go Large strategy have been disastrous for both the catastrophic losses and reserve strengthening on the commercial P&C business, as the results below show. Duperreault and his team have been busy working on refocusing the underwriting philosophy, modernizing systems and analytics, bringing in talent (including buying Validus), redesigning reinsurance protections and reshaping the portfolio.

click to enlarge

In their latest quarterly call, the new management team is boldly predicting an underwriting profit on the general insurance business (commercial and consumer) in 2019, assuming a catastrophe load of less than 5% and reductions in loss and expense ratios, which will require a +10% improvement in the 2018 result. In a sector where competitors have long since evolved (some use AI to optimise their portfolios and returns) and the alchemy of low return capital providers is ever present, they have set themselves an aggressive target.

click to enlarge

Given the current share price just below $42, its trading around 76% of the adjusted book value. If all things go well, and some recent headwinds (e.g. reserve strengthening) are tamed, I can see how a pre-tax income target of $3.5 billion to $4 billion and an adjusted income diluted EPS of $4.00 to $4.50 is achievable. These targets are roughly where analysts are for 2019, returning to EPS results achieved over 5 years ago. I concur on the targets but think the time-frame may be optimistic, another year of clean-up looks more likely.

It will be interesting to see how the year progresses.