In my last post on AIG, I expressed my doubts about the P&C targets outlined in their plan. After first announcing a $20 billion retroactive reinsurance deal with Berkshire covering long tail commercial P&C reserves for accident years prior to 2015 in January, AIG just announced another large commercial lines reserve charge of $5.6 billion principally from their US business. The graph below shows the impact upon their 2016 pre-tax operating income.

click to enlarge

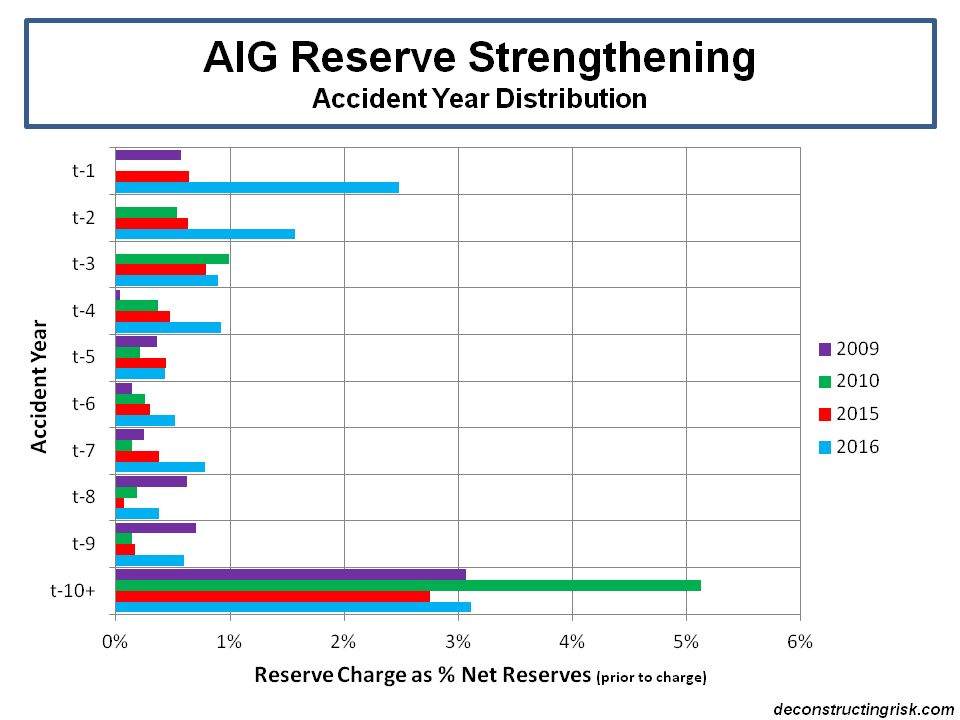

The latest reserve hit amounts to 12% of net commercial reserves at end Q3 2016 and compares to 7%, 8% and 6% for previous 2015, 2010, and 2009 commercial reserve charges. Whereas previously reserve strengthening related primarily to excess casualty and workers compensation (WC) business (plus an asbestos charge in 2010), this charge also covers primary casualty and WC business. The accident year vintage of the releases is also worryingly immature, as the graph below shows. After the 2016 charge, AIG have approx $7 billion of cover left on the Berkshire coverage.

click to enlarge

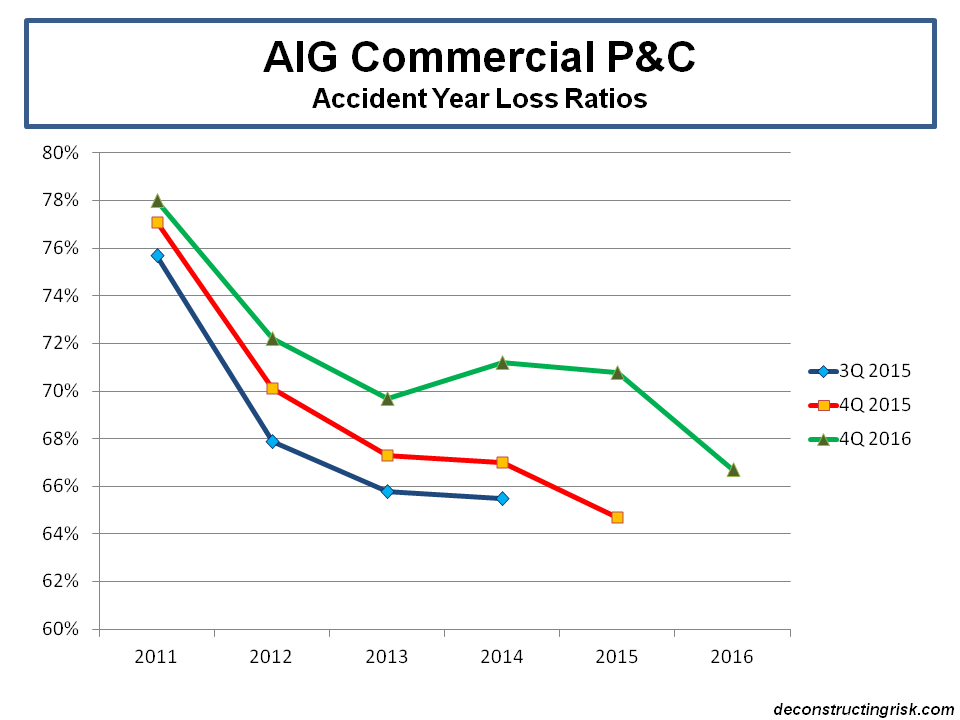

Although AIG have yet again made adjustments to business classifications, the graph below shows near enough the development of the accident year loss ratios on the commercial book over recent times.

click to enlarge

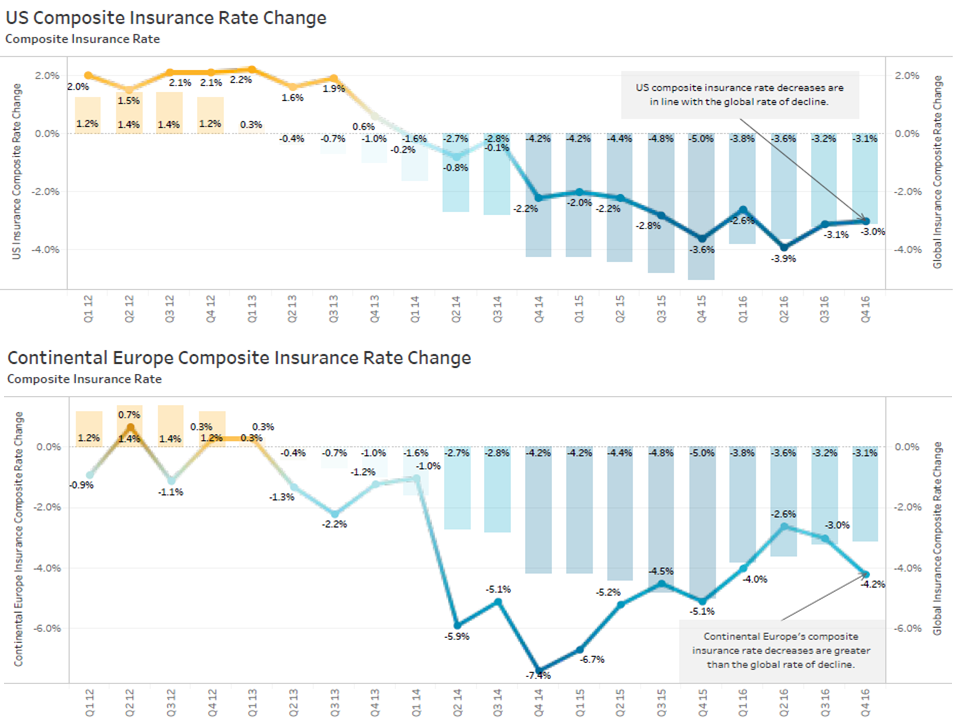

It is understandable that AIG missed their aggressive target against the pricing background of the past few years as illustrated by the latest Marsh report, as the exhibits below on global commercial rates and the US and European subsets show.

click to enlarge

click to enlarge

All of these factors would make me very skeptical on the targeted 62% exit run rate for the 2017 accident year loss ratio on the commercial book. And no big reinsurance deal with Berkshire (or with Swiss Re for that matter) or $5 billion of share buybacks (AIG shares outstanding is down nearly a third since the beginning of 2014 due to buybacks whilst the share price is up roughly 25% over that period), can impact the reality which AIG has now to achieve. No small ask.

Some may argue that AIG have kitchen-sinked the reserves to make the target of accident year loss ratios in the low 60’s more achievable. I hope for the firm’s sake that turns out to be true (against the odds). The alternative may be more disposals of profitable (life) businesses, possibly eventually leading to a sale of the rump and maybe the disappearance of AIG altogether.

I can remember Hancock saying that their P&C reserves are adequate and that they will adjust them over time as new facts emerge (what I remember, didn’t find the original quote). I scratched my head back then since it sounded like „we don’t have enough make to properly strengthen our reserves so we go ahead and hope for the best“. Berkshire probably made a good deal… 25bn cushion/subordination, beyond that they cover 80% of the next 25bn… and all at their usual price of 50% of covered future losses. Plus that AIG has to pay 4% interest on the amount held in trust. I haven’t looked at those term sheets in the past, can you tell me whether this is a common feature (my understanding so far was that Berkshire would pocket the money and go ahead and do funny things with it like buying companies, not that the money would be put into a trust)?

Honestly, I don’t like this. Seth Klarman (Baupost) doesn’t have AIG warrants in his portfolio as of 3Q 2016 (he still had them as of 2Q 2016), so one of the deep value guys I follow is out. Bruce Berkowitz (Fairholme Funds) is still in, I wonder what his position will look like in one or two quarters.

Eddie

Hi Eddie,

I haven’t seen the fine detail of the Berkshire deal. On face value it looks like a typical float deal, $10B of premium for the current cession of $13B. IF the reserves deteriorate by another $5B (the accident year loss ratio picks for the more recent years still look optimistic to me given the rating environment at the time), that’s another $4B ceded to Berkshire or $17B in total. Assuming a 15 year average maturity (obviously these are excess the attachment so the time to paid is long) that’s an annual return rate of 3.5% Berkshire needs to make. They only need a 5% return if the total $20B limit is hit.

It can be common practice to assume a interest rate (by either reinsurer or cedant) for the sake of some notional profit sharing account. In AIG’s case, I don’t think a profit commission is on the cards with this deal!!! Holding assets in trust is also common but as you say generally Berkshire gets the investment mandate to do what it wants. Again, I haven’t seen the detail in the term sheet – where did you see it, in a SEC filing?

To me the biggest issue with the deal is who maintains control over claim settlement. As I understand it that stays with AIG (contrary to other Berkshire deals). That’s a big issue for AIG as what Fortune500 company is going to take them seriously going forward if they don’t control the claim settlements on the back book (and these are generally the large high profile claims in the tail).

Overall, I share you concerns on AIG, doesn’t look to me like a firm that’s in control of its future. Selling off your prime assets while you get you poor performing businesses under control is not confidence generating, particularly if the future is the P&C business which I think faces years of sub-par performance. The issue is capacity and AIG’s competitors are in much better shape reserve strength wise (Berkshire increasingly being one of their competitors!!). Until there is real blood on the streets that is not going away. I have no insurance investments currently, upside to downside just isn’t there IMO.

Hope all good with you.

M

Wow, thanks for the comprehensive answer. Thanks, everything is fine on my end. A lil’ busy right now but that doesn’t hurt.

I got the information from AIG’s 8-K as of 14 Feb 2017. Regarding settlement it says

“The Reinsured shall retain sole responsibility for its claims handling and reinsurance on the Covered Business, including Ceded Reinsurance, and for the pursuit and collection of any Salvage And Subrogation with respect thereto.” (5.1).

So basically exactly what you said. Regarding the investment of the proceeds, Buffet mentioned in his latest latter that Berkshire’s float is not USD 91bn, but rather above USD 100bn due to a big ticket they wrote. So he views it as investable.

I couldn’t agree more regarding AIG’s control of its future. I mean, they just admitted (my interpretation) that half of their P&C book is kinda crappy, so why should the other half be in better shape? Especially given their history of increasing reserves retroactively.

Full disclosure, I am long BRK and MKL, but then those are not typical insurance cos imho.

In case you are interested, their is an older (2014) presentation regarding Lancashire at ValueXVail (http://valuexvail.com/presentations/#!mg_cd=47).

All the best,

Eddie