It has been over 6 months since I have posted on the prospects for the telecommunications firm Level3 (LVLT) following its merger with TW Telecom (TWTC). I had previously posted on the strength of TW Telecom’s business model and its admirable operating history so I am extremely positive on the combination. At the time of the last post, LVLT was trading around $45 a share, a five year high. Since that time, the stock fell to a low of $38 in October 2014 before reaching a new high in recent weeks around $54.

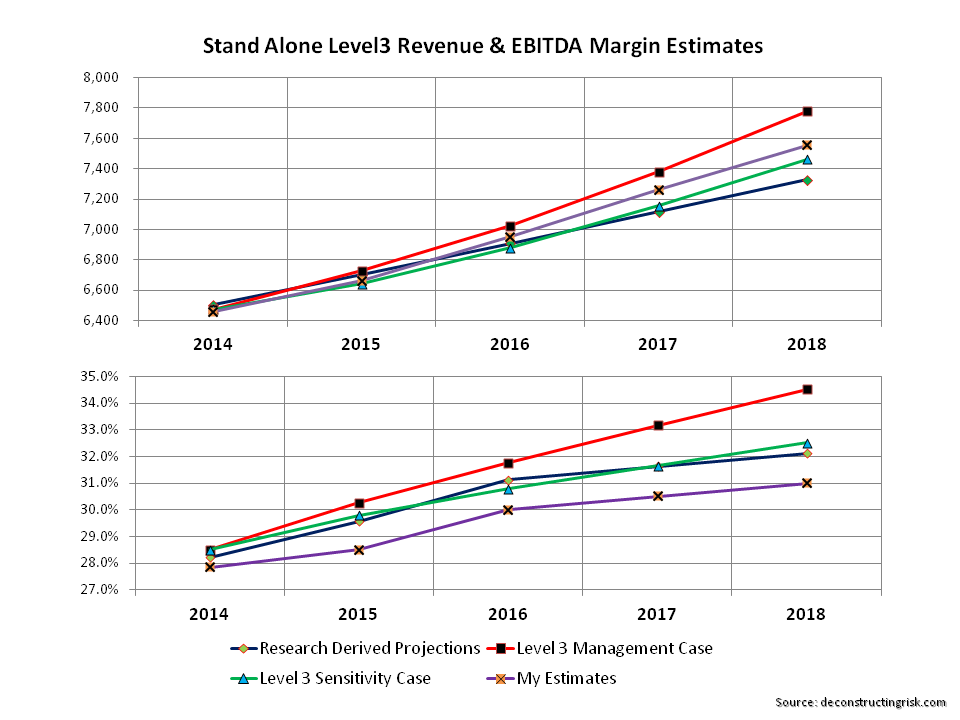

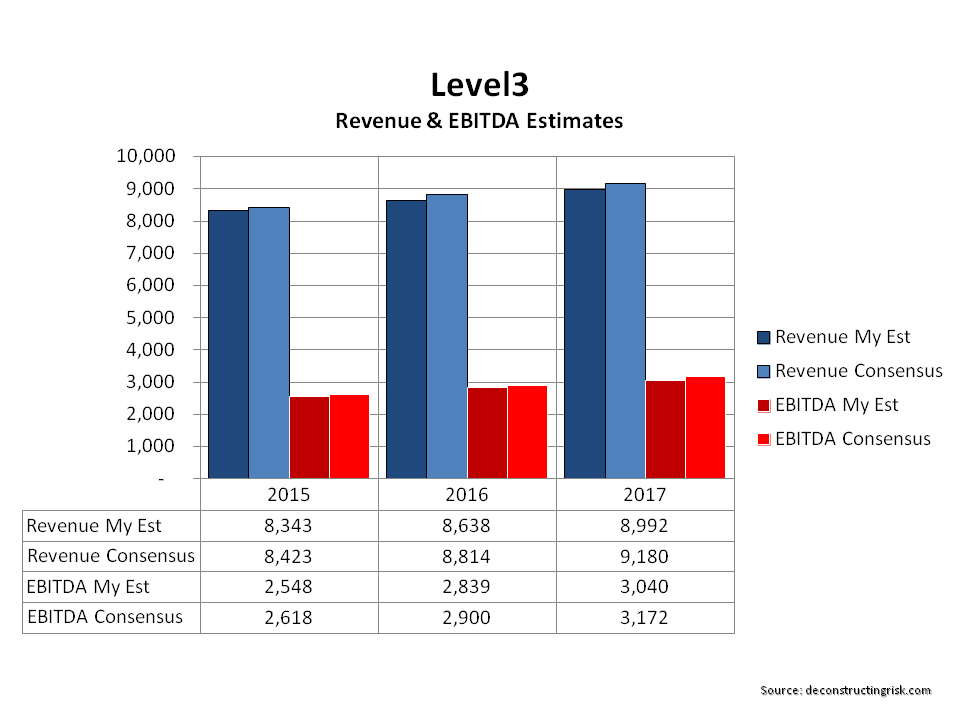

My previous post, using figures disclosed in a S-4 filing on the merger negotiations, made a projection that the combined entity could get to $9 billion of revenue and $3 billion of EBITDA by 2016. Based upon the Q4 figures, the firm’s guidance, and the recently filed 10K, I did some more detailed figures and now estimate that the $9B/$3B revenue/EBITDA threshold will more likely be in 2017 rather than 2016. My estimates for each against the consensus from analysts are below.

click to enlarge

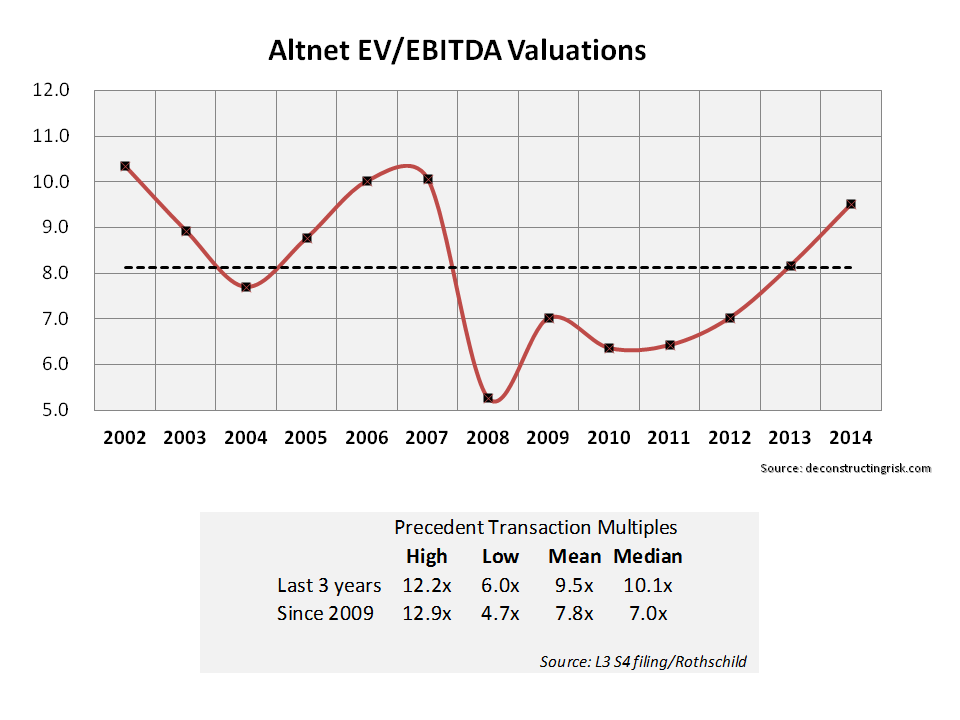

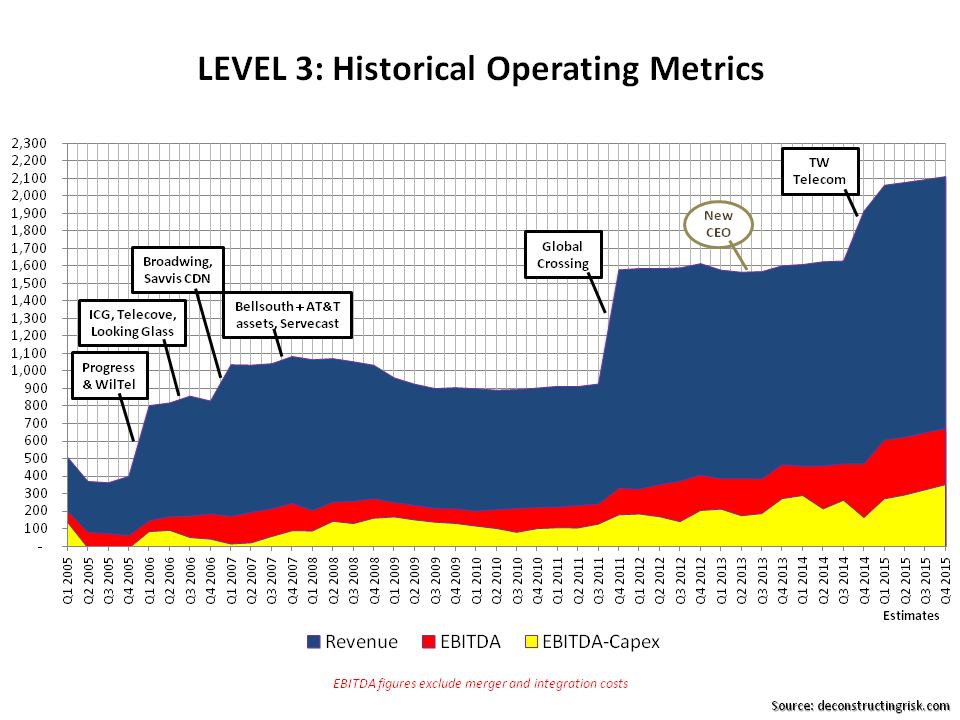

LVLT is an acquisitive firm and has learned through multiple deals the optimal way of integrating new firms through a shape focus on the customer experience whilst prudently integrating operations and reducing costs. Taking the Global Crossing integration as a template, the graphic below illustrates how my estimates fit in the past.

click to enlarge

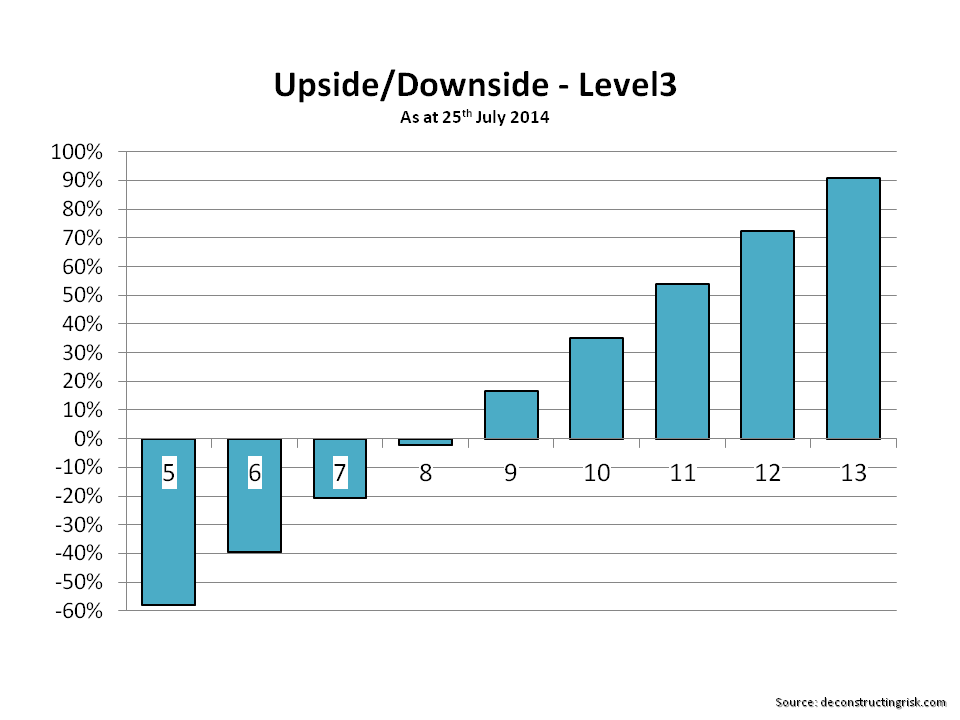

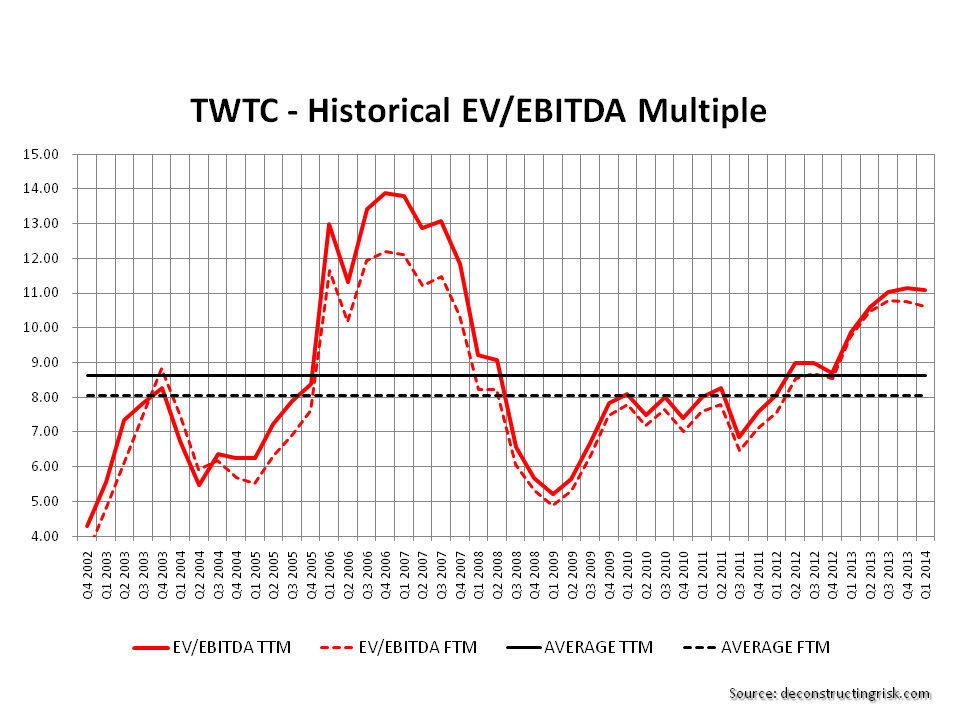

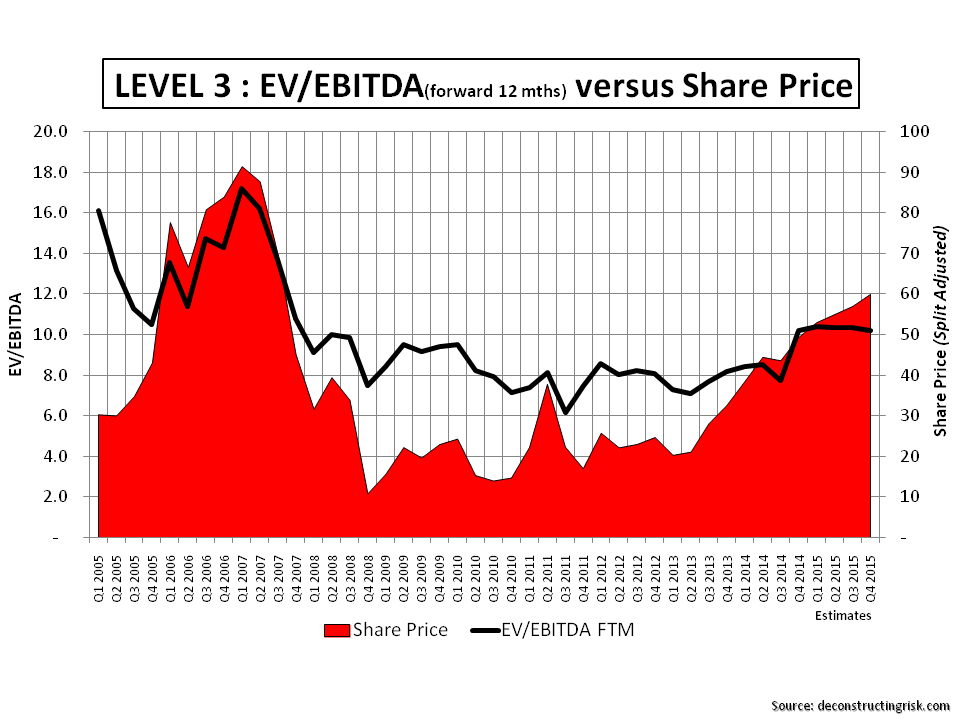

So, the question now is whether a share price in the mid to high 50s is justified (the average consensus is around $57 with the highest being Canaccord’s recent target of $63). Using an enterprise value to EBITDA multiple based upon a forward 12 month EBITDA figures (actual where relevant and my estimates from Q1-2015), I think a target between $50 and $60 is justified assuming a forward multiple of 10 to reflect growth prospects, as the graphic below illustrates. My DCF analysis also supports a target in the low 60s.

click to enlarge

Such a target range assumes operating results show positive momentum and that the overall market remains relatively stable with expectations on interest rate increases in the US within current estimates. Due to LVLT’s net debt load of just under $11 billion and a proforma leverage ratio of 4.4 to EBITDA, the stock is historically exposed to macro-economic volatility. A mitigant against such volatility is the increasing level of free cash that the business will generate (I estimate $600/$900/ $1,000 million over 2015 to 2017). Also, about $6.5 billion of its debt is fixed (current blended rate is 7.2%) and LVLT’s CFO has shown considerable skill in recent years at managing the interest rate down in this yield hungry environment. Its remaining floating debt (blended rate of 4.2%) has a minimum LIBOR rate of 1% and therefore offers headroom against movements in current LIBOR rates

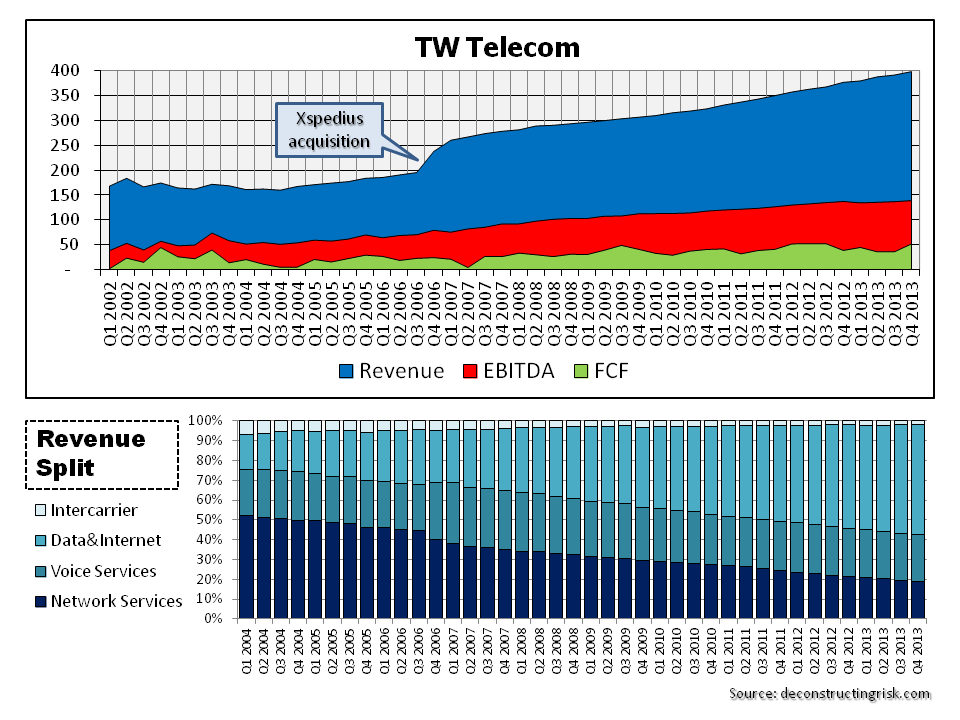

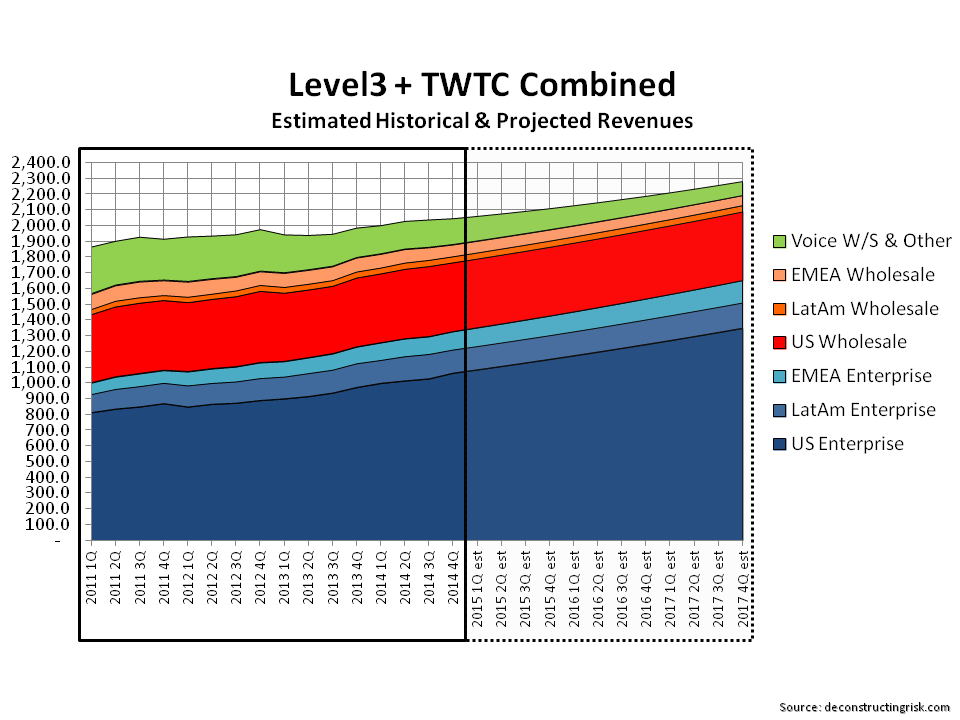

In my view, the key in terms of valuation is that the integration goes smoothly and that revenue growth in the enterprise market is maintained. One of the principal reasons for my optimism on LVLT is the operational leverage the business has as the mix of its business moves more towards the higher margin and stickier enterprise market, as the pro-forma revenue split shows.

click to enlarge

As always with LVLT, I recommend using options to protect downside and waiting for a pull-back from current highs for any new investment. This stock has historically not been one for the faint hearted. I do believe however that they are on the path to a more stable future and it remains a core holding for me.