Insurers and industry participants have reacted with the expected bemusement to the announcement on the 18th of July from the Financial Stability Board (FSB) on the list of “too big to fail” insurers, aka G-SIIs or Global Systemically Important Insurers. To be fair, the list of nine – three US, five European and one Chinese – does look inconsistent. No Japanese for example or the inclusion of Aviva but the exclusion of Zurich.

Industry groups such as the Geneva Association and Insurance Europe have asked for clarity on the criteria and more disclosure on the impact. The timetable released by the FSB includes announcing the reinsurers to be designated as G-SIIs by mid 2014 (now that will be interesting given the global focus of a reinsurer’s business model) and the finalization of the additional loss absorption measures for G-SIIs by the end of 2015 with an implementation date of the start of 2019.

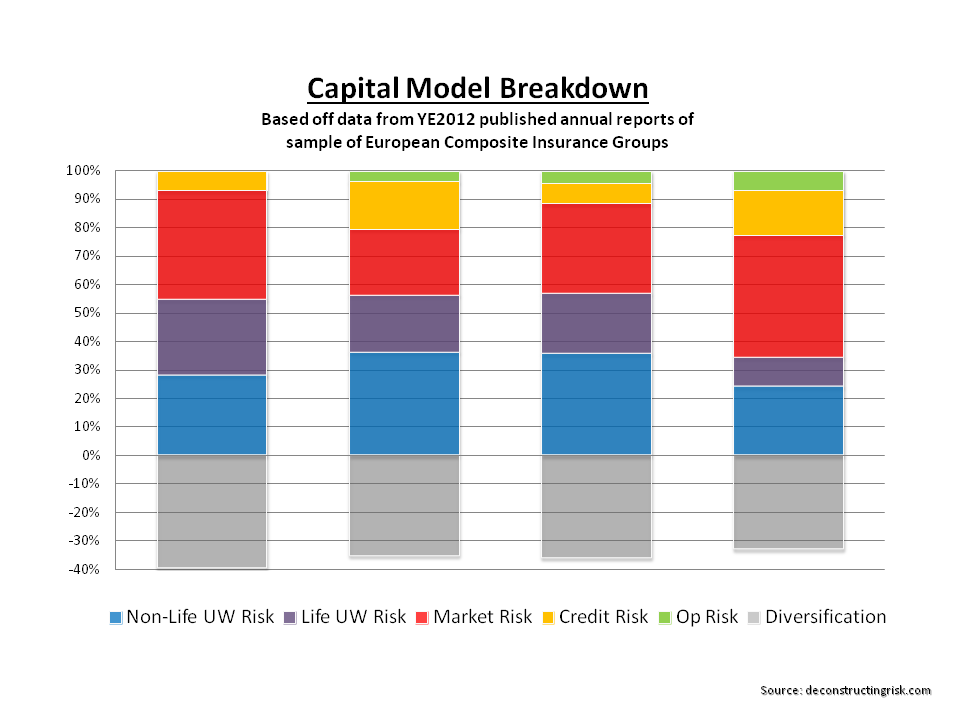

The generous diversification credits that large insurers have calculated using economic capital models (likely to be used under Solvency II) can be seen in the graph below based upon data from a sample of published results from 2012 annual reports of a number of European insurance groups.

click to enlarge

The graph shows assumed diversification across risk modules of 30% to 40% but does not show the significant diversification assumed by insurers within risk modules, particularly for the larger firms with a wide spread of business classes. Munich Re, for example, highlights a further 30% and 50% discount in their non-life underwriting risk and market risk modules respectively. Aviva is perhaps startlingly open when it revealed, in its year end results presentation, a diversification discount within its business unit of 45% and a further diversification discount across business units and jurisdictions of 40%. Their gross undiversified capital of £31 billion reduced by 68% to £10 billion after been sprinkled with the diversification magic dust.

Given the competitive advantage that size and diversity brings under the risk based regulatory capital systems being introduced or planned for introduction across the globe, the large insurance groups just named as G-SIIs will likely step up their lobbying efforts to a new level in the next few years against any costly or detrimental measures by the FSB that could impact their hard won competitive advantage. Another avenue for the G-SII to negate any capital impact is to sharper their pencils further on the diversification effects calculated in their economic capital models!