As between clear blue and cloud,

Between haystack and sunset sky,

Between oak tree and slated roof,

I had my existence. I was there.

Me in place and the place in me.

Extract from “A Herbal”

As between clear blue and cloud,

Between haystack and sunset sky,

Between oak tree and slated roof,

I had my existence. I was there.

Me in place and the place in me.

Extract from “A Herbal”

Lancashire (LRE.L) is a London quoted specialty insurer that writes short tail (mainly insurance) business in aviation, marine, energy, property catastrophe and terrorism classes. Set up after Hurricane Katrina, the company operates a high risk high reward business model, tightly focussed by the experienced hand of CEO Richard Brindle, with an emphasis on disciplined underwriting, tight capital management and generous shareholder returns. Shareholder’s equity is managed within a range between $1 billion and $1.5 billion with numerous shareholder friendly actions such as special dividends resulting in a cumulative shareholder return of 177% since the company’s inception over 7 years ago.

I am a fan of the company and own some shares, although not as many as in the past. I like their straight forward approach and their difference in a sector full of firms that seem to read from each other’s scripts (increasingly peppered with the latest risk management speak). That said, it does have a higher risk profile than many of its peers, as a previous post on PMLs illustrated. That profile allows it to achieve such superior shareholder returns. The market has rewarded Lancashire with a premium valuation based upon the high returns achieved over its short history as a March post on valuations showed.

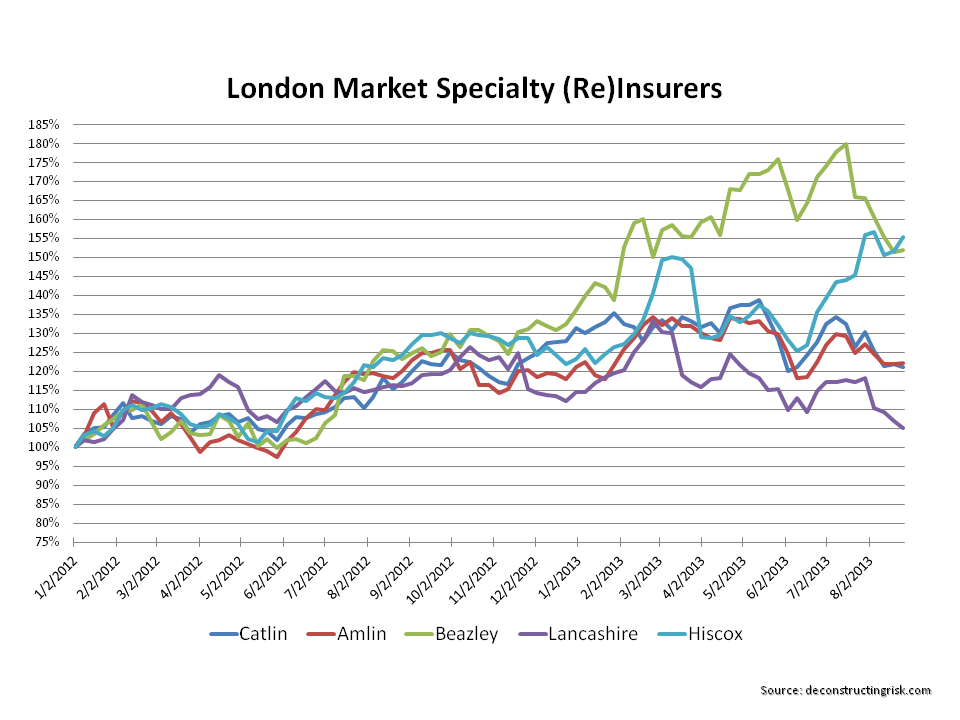

However, over the past 6 months, Lancashire’s share price has underperformed against its peers, initially due to concerns over property catastrophe pricing pressures and more recently it’s announcement of the purchase of Lloyds of London based Cathedral Capital.

click to enlarge

Cathedral’s results over the past 5 years have been good, if not in the same league as Lancashire’s, and the price paid by Lancashire at 160% of net tangible assets is not cheap. Given the financing needs of the acquisition, the lack of room for any of Lancashire’s usual special dividend treats in the near term has been a contributing factor to the recent share price declines in my opinion.

Based upon the proforma net tangible assets of Lancashire at end Q2 as per the Cathedral presentation and the circular for the share offering, the graph below shows the net tangible valuation multiples of a number of the London market insurers using net tangible asset values as at end Q2 with market values based upon todays’ closing prices.

click to enlarge

The multiples show that the market is now valuing Lancashire’s business at a level more akin to its peers rather than the premium valuation it previously enjoyed. Clearly, the acquisition of Cathedral raises questions over whether Lancashire will maintain its uniqueness in the future. That is certainly a concern. Also, integrating the firms and their cultures is an execution risk and heading into the peak of the US wind session could prove to be unwise timing.

Notwithstanding these issues, Brindle is an experienced operator and I would suspect that he is taking full advantage of the current arbitrage opportunities (as outlined in another post). It may take a quarter or two to fully understand the impact of the Cathedral acquisition on Lancashire’s risk/reward profile. I, for one, look forward to stalking the company to find an attractive entry point for increasing my position in anticipation of the return of Lancashire’s premium multiple.

Posted in Insurance Firms, Investing Ideas

Tagged Amlin, Cathedral Capital, Catlin, Hiscox, insurance price tangible book value, Lancashire, Lancashire specialty insurer, net tangible asset, price tangible book values, price to tangible book value, Richard Brindle, shareholder returns, special dividend, tangible book value, tangible book value multiples

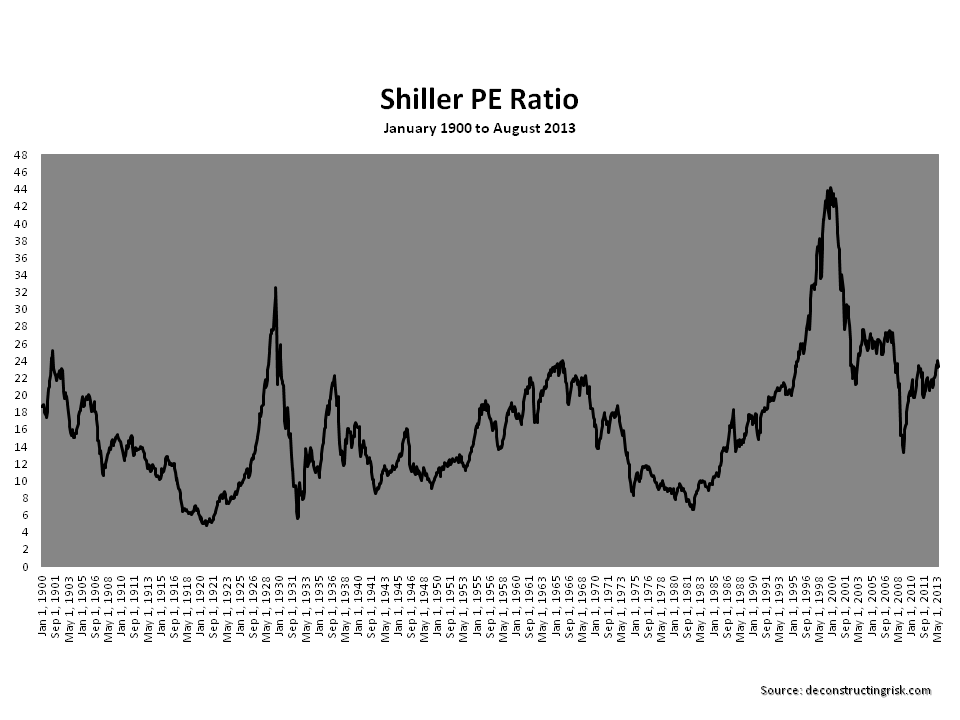

With stock valuations high and the market chatter nervously fixated on the great tapering debate, the bears claimed victory today with the S&P off 1.6% and the Dow down 170 points.

The impact of Central Bank liquidity has undeniably resulted in lofty stock valuations given the economic backdrop, as the graph of the historical Shiller PE ratio below illustrates.

Click to enlarge

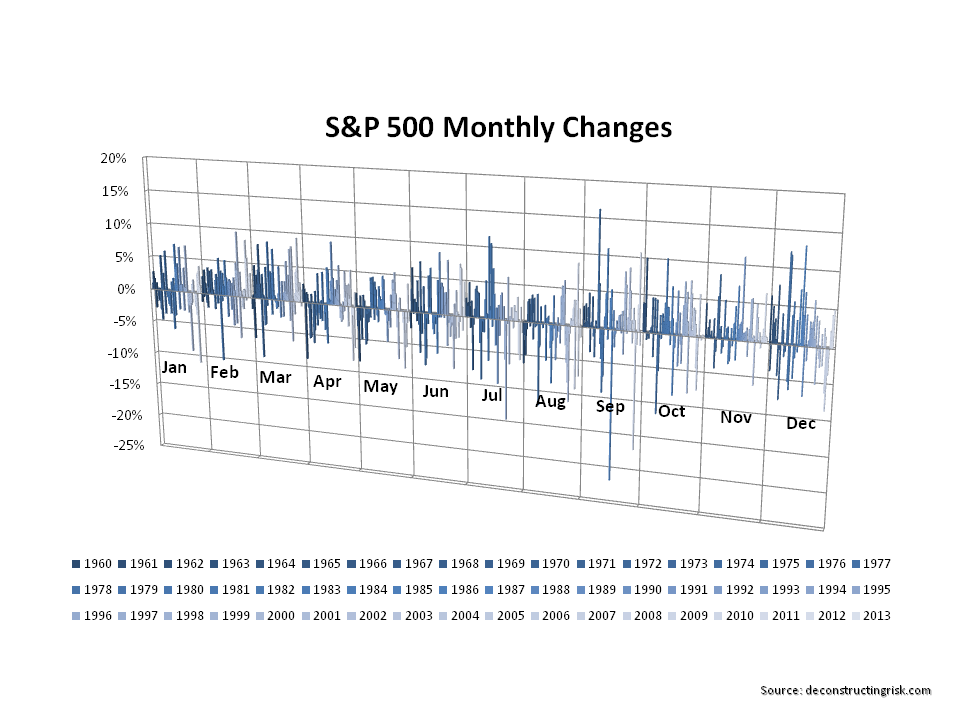

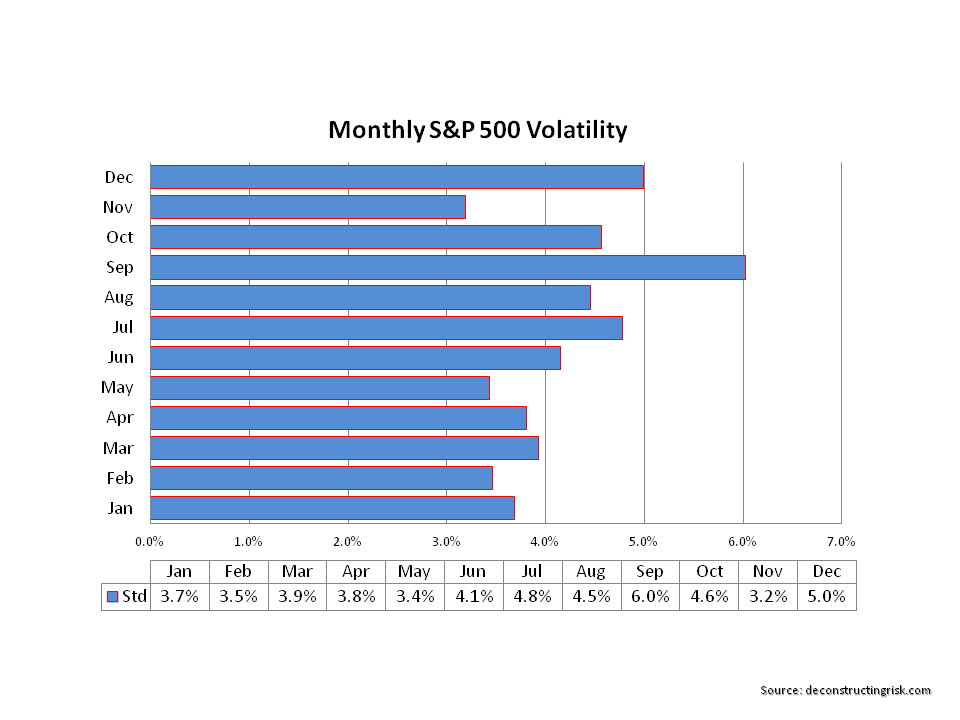

September is commonly viewed as the month when investors and traders, upon their return from sunning themselves, get nervous about year end results (read bonuses) and start to take money off the table. The statistics back this up as the graphs below on historical S&P 500 monthly returns illustrates.

Click to enlarge

So, today looks to me like the possible opening salvo for a September bear party. I wouldn’t get too worried though, despite the musings from Jackson Hole there is always a Central Bank around to scare the naughty bears away if they overstay their welcome.

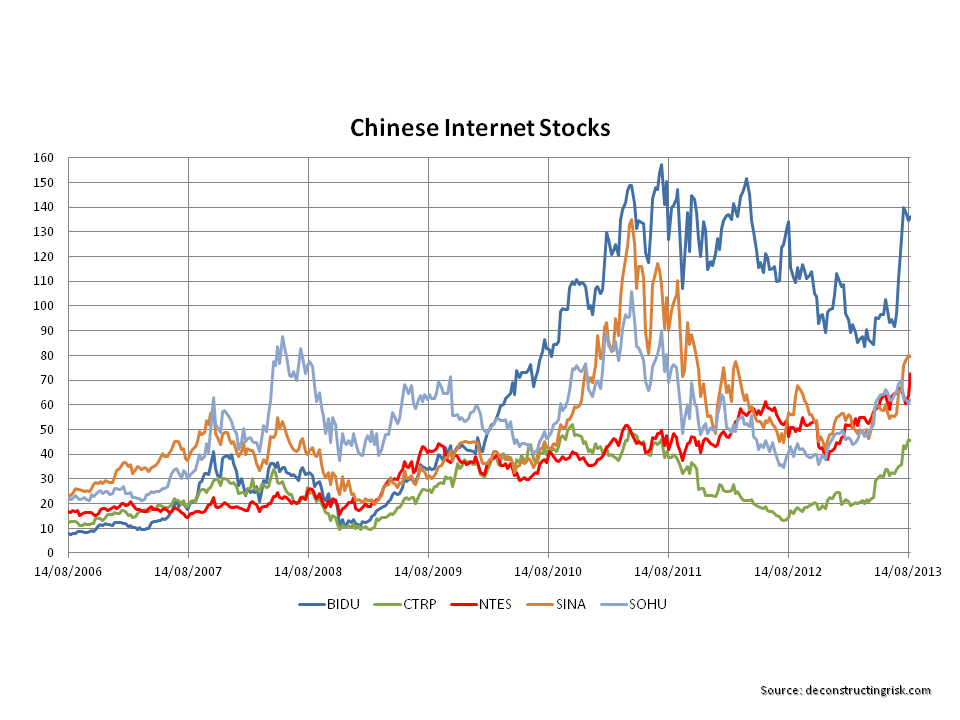

Every experienced investor, like a jaded poker player, has stories akin to bad beat tales – great investments that got away. This post is not one of those tales. Seven odd years ago I did have a look at a few of the then hot Chinese internet shares – SINA and SOHU in particular. Both were growing solidly and were valued with big future growth assumed. Given the heated valuations and the lack of a credible history at that time, I passed. I was also uncomfortable with the political risk factor.

It was therefore with interest that in recent months I noticed a few stories about stock increases in some familiar Chinese internet names. A quick look through the key statistics on Yahoo confirms that valuations remain aggressive with PEs based upon 2013 projected earnings in the 20 to 40 range across a sample of firms (albeit not as wild as in the past). Quarterly revenue, if not profit, growth also looks healthy at 20% to 30%. The graph below shows the share prices of some of the better known Chinese internet firms over the past seven years.

click to enlarge

Although I suspect my risk appetite will never be comfortable with valuations in this sector, at some stage, I’d like to dig deeper into the quality firms in this space to figure out if there is any appropriate risk/reward investment angle that I could live with (and at what entry level on valuation). If nothing else, the rise and fall over 2011 to 2012 of SINA and SOHU looks intriguing (for old time’s sake!).

Posted in Investing Ideas

Tagged aggressive valuation, Baidu, Chinese internet stocks, Ctrip.com, growth stocks, internet valuations, NetEase, SINA, SOHU, valuations

There was some interesting commentary from senior executives in the reinsurance and specialty insurance sector during the Q2 conference calls.

Evan Greenberg of ACE gave the media a nice sound-bite when he characterised the oversupply in the property catastrophe sector as “that pond with more drinking out of it”. He also highlighted, that following a number of good years, traditional reinsurers “are hungry” and that primary insurers are demanding better deals as their balance sheets have gotten stronger and more able to retain risk. Greenberg warns that, despite claims of discipline by many market participants, for some reinsurers “it’s all they do for a living and so they feel compelled” to compete against the new capacity.

Kevin O’Donnell of Renaissance Re put some interesting perspective on the new ILS capacity by highlighting that in the early days of the property catastrophe focused reinsurer business model, they “thought about taking risk on a single model”. These reinsurers developed into multi-model and some into proprietary model users. O’Donnell highlighted that the new capacity from capital markets “is somewhat similar to” earlier property catastrophe reinsurance business models and “that, but beyond relying in some instances, on just a single model, they are relying on a single point.” O’Donnell stressed that “it’s very important to understand the shape of the distribution, not just the mean.” Edward Noonan of Validus commented that “the ILS guys aren’t undisciplined; it’s just that they’ve got a lower cost of capital.”

Historically lax pricing in reinsurance has quickly trickled down into softer conditions in primary insurance markets. In the US, although commercial insurance rates have moderated from an average increase of 5% to 4% in recent months, the overall trend remains upwards and above loss trend. Greenberg believes that the reason why it could be different this time is “the size of balance sheet on the primary side on the large players” and that more intelligent data analytics means that primary insurers are “making different kinds of decisions about how to hold retentions” and “how to think about exposure”. Although Greenberg makes valid points, in my opinion if pricing pressures continue in the reinsurance sector, the knock-on impacts onto the primary sector will eventually start to emerge.

As always, the market in property catastrophe is dependent upon events, particularly from the current windstorm season. Noonan of Validus commented that the market can’t “sustain a couple more years of 15% off”, referring to the recent Florida rate reductions. Diversified reinsurers point to their ability to rebalance their portfolios in response to the current market. However the resulting impact on risk adjusted returns will be an issue the industry needs to address. The always insightful and ever direct John Charman, now at the helm of Endurance Specialty, highlights the need to contain expenses in the industry. Charman commented “when I look at the industry, it’s very mature.” He characterised some carriers as being “very cumbersome” and “over-expensed”.

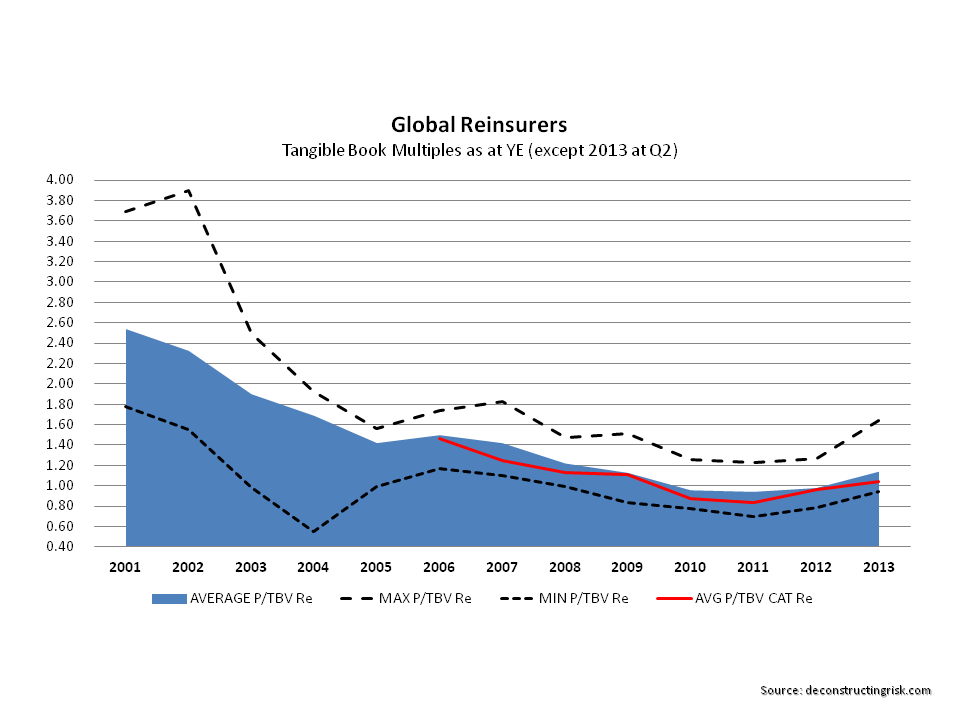

For the property catastrophe reinsurers, the shorter term impact on their business models will likely be that they will have to follow a capital management and shareholder strategy more compatible with the return profile of the ILS funds. In terms of valuations, the market is currently making little distinction between diversified reinsurers and catastrophe focussed reinsurers as the graph below of price to tangible book for pure reinsurers and catastrophe reinsurers show. Absent catastrophe events, that lack of distinction by the market could change in the near term.

click to enlarge

In the shorter term, the more seasoned and experienced players know how to react to an influx of new capacity. The conferences calls demonstrate those taking advantage of the arbitrage opportunities. Benchimol of AXIS commented that “we have actually started to hedge our reinsurance portfolio using ILWs and other transactions of that type.” O’Donnell commented that “we continue to look for attractive ways of ceding reinsurance risk as a means to optimizing our reinsurance portfolio.” Charman commented that “we also took advantage of the abundant capital by purchasing Florida retro protection”. Noonan commented that “we also found good value in the retrocession market and took the opportunity to purchase a significant amount of protection for our portfolio during the quarter.” Iordanou of Arch commented that “we did buy more this quarter” and that “we felt we were getting good deals.”

Right now, we are clearly in an arbitrage market and the reinsurers that will thrive in this market are those who are clever enough to use the current market dislocation to their advantage.

Posted in Insurance Firms, Insurance Market

Tagged arbitrage market, capital management and shareholder strategy, commercial insurance rates, discipline by market participants, diversified reinsurers, Edward Noonan, Endurance Specialty, Evan Greenberg, hedge reinsurance portfolio, higher ceding commissions, ILS funds, ILWs, intelligent data analytics, John Charman, Kevin O’Donnell Renaissance Re, multi-model, new ILS capacity, primary insurance markets, proprietary model, Q2 conference calls, reinsurance, reinsurance pricing

![]() This blog represents my personal views and is not reflective of the views or opinions held by any company or employer I work for currently or have worked for in the past. The views expressed herein are based solely upon publicly available data. No views expressed herein should be taken as an endorsement to take any particular course of action in the markets. The basis of this blog is that different views should be expressed and readers make up their own minds on the what they believe and act accordingly.

This blog represents my personal views and is not reflective of the views or opinions held by any company or employer I work for currently or have worked for in the past. The views expressed herein are based solely upon publicly available data. No views expressed herein should be taken as an endorsement to take any particular course of action in the markets. The basis of this blog is that different views should be expressed and readers make up their own minds on the what they believe and act accordingly.