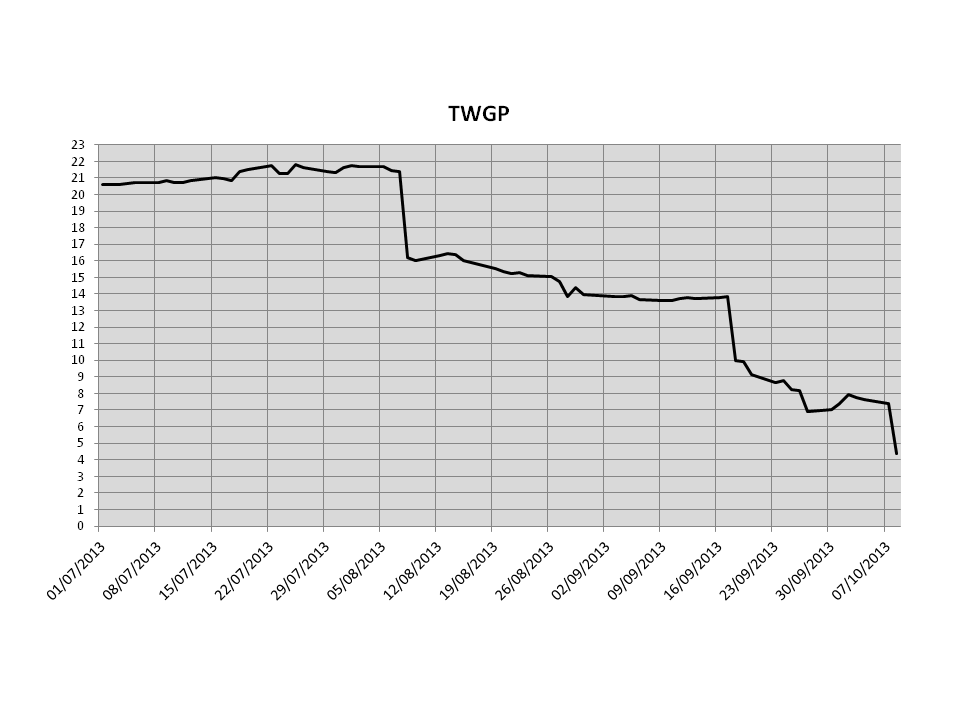

The news from Tower Group International Ltd (TWGP) today has been disastrous. A $365 million reserve hit from commercial lines business and a $215 goodwill impairment charge resulted in a Fitch downgrade to below investment grade. The impact can be seen below in the recent share price collapse.

click to enlarge

Difficulties at the firm were first signalled in the postponement of its quarterly results in early August and despite some hurriedly arranged new reinsurance coverages; the future for the firm looks bleak. It yet again highlights that once confidence in an insurer’s reserves is lost, it is difficult to recover (unless like AIG you get purchased by the US government!). It also shows that intangible assets provide little comfort in distress scenarios. There are cases, such as XL Capital, where a recovery of sorts has occurred but such firms rarely recover their past glories and often end up been sold at a discount or going into run-off. It is always important to remember that insurance is a risk business where you sell a product whose cost of goods sold is not known with certainty for sometime after the point of sale.

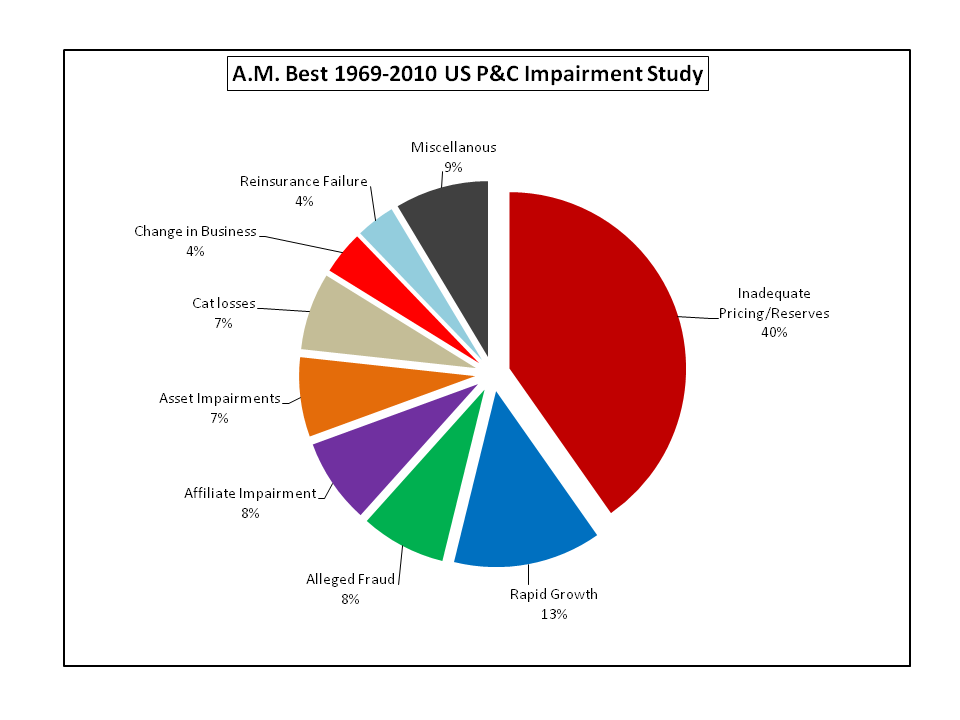

AM Best publishes statistics on US insurance impairments, where an impairment is defined as an insurer who has been the subject of a regulatory action taken by an insurance supervisory department and can be used as a good proxy for a default. As can be seen by the pie graph below, the largest cause of impairment, by quite a distance, is inadequate pricing and reserving.

click to enlarge

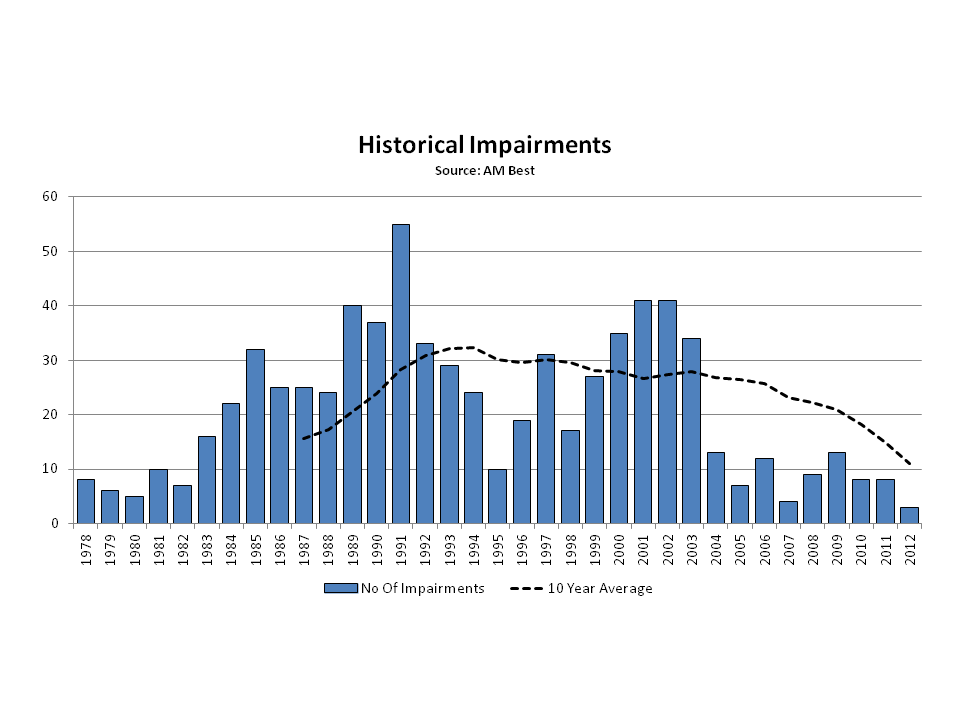

What the exhibit above likely misses is the changing profile of the US insurance sector over the past 20 years with less small to medium sized firms and improving risk management practices. The number of impairments has being decreasing in recent years as a result of changes in the sector’s profile.

click to enlarge

Let’s hope that TWGP is an exception rather than the start of a new trend.

Do you have an idea how big TWGP is / was in terms of market share in the respective markets where it is / was active ? Would be interesting to get a feeling for the overall impact.

Cheers,

Eddie

Hi Eddie

I know very little about them, they really weren’t on the radar before this. They did a deal with the Lloyds entity Canapious for their Bermuda reinsurer but I don’t think that was material.

I think I read that the reserve hit is coming from 2009 to 2011 commercial lines. They write about $2B premium split about a third each between SME commercial, niche specialty and consumer.

They call themselves a top 50 US P&C insurer which I suspect means they are closer to the 50th than otherwise!

The reserve figures of over $300M sound big compared to about $600M of annual premium on commercial lines.

All the best.

M

Eddie,

On TWGP this guy seems to know what he is talking about:

http://seekingalpha.com/article/1735962-on-tower-group?source=yahoo

Looks like they have being growing rapidly & reserves didn’t keep up.

This guy on the other hand is a muppet, mind boggles that he is a professor at Yale! School boy rationale

http://seekingalpha.com/article/1710492-tower-group-a-classic-overreaction-story

M

50+% growth per year… Wow ! This alone should have been a harbinger of things to come since they put top-line growth above balance sheet quality.

Agreed, this Zhang guy is an idiot. It might be that I saw him before in connection with AIG. The quality of his post was about the same.

Thanks for the effort !

Best,

Eddie