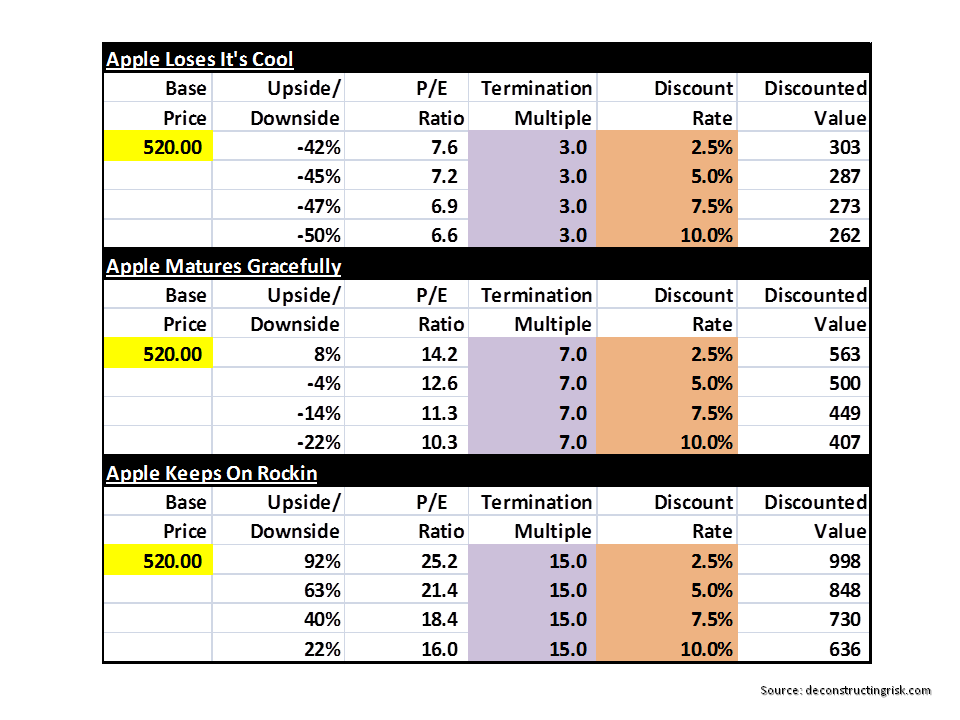

In my previous post on AAPL in April, when the stock was trading around $400, I presented an analysis of three possible scenarios – Apple loses it’s cool, Apple matures gracefully, and Apple keeps on rockin’. Each of these scenarios involved some fanciful assumptions on the trajectory of Apple’s products which I clearly highlighted as likely to prove well off the mark in reality. I did say however, that “the purpose here is not to predict the future but to get an idea of Apple’s valuation given the views prevalent today”.

Well, although a fair amount has happened to AAPL over the past 6 months in relation to an iPhone/iPad/Mac product refresh, a new music steaming service and a number of shareholder friendly actions on buybacks, the hoped for visibility into AAPL’s medium term future remains somewhat elusive and will likely remain so in the short term. The speculated China mobile deal remains a possible short term catalyst.

The three opening observations in my April post do, in my opinion, remain valid: namely, that the iPhone is core to Apple’s future with no new “product category” currently envisaged having the potential to replace the dominant contribution that iPhone makes to profits in the medium term, that gross margins are likely to continue to fall in the face of increased competition, and that a Nokia/Blackberry rapid fall from grace is unlikely given Apple’s ecosystem and loyal customer base (for now!).

There is little point trying to redo the scenarios by replacing one set of assumptions with another so I have simply updated the current share price in the exhibit below.

click to enlarge

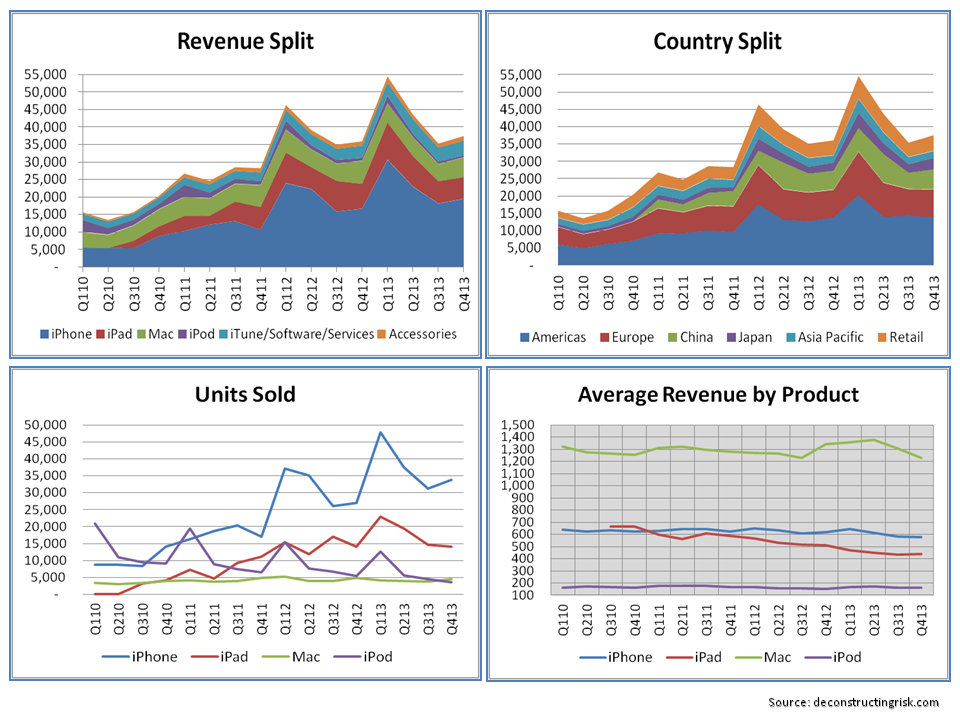

By way of disclosure, I did establish a small position in AAPL 6 months ago around $420, as my April post suggested. Against my expectations outlined in that post, market sentiment on AAPL has clearly moved around the “Apple matures gracefully” valuation from an “Apple loses its cool” bias firmly towards an “Apple keeps on rockin” bias. The exhibit below shows the most recent results from AAPL.

click to enlarge

The degree to which the change in market sentiment on AAPL over the past 6 months is due to underlying fundamentals or simply a function of general market bullishness is open to debate. One factor that cannot be underestimated is Apple’s own buyback programme with approx. 40 million shares repurchased over the past two quarters.

The iPhone and iPad product refreshes have no doubt had an impact on the short term perspective of AAPL. One factor that doesn’t seem to be discussed in the market is whether the product refreshes impact positively or negatively upon Apple’s brand or tests the loyalty of its customer over the longer term.

Market hype from the likes of Carl Icahn should be ignored (my view on the leech that is Mr Carl Icahn is expressed in a previous telecom post) and I don’t understand why Mr Cook is entertaining such distractions.

My own estimates for the holiday Q1 2014 quarter were blown away by Apple’s revenue projections. Based upon recent trends, I was coming up with revenue of $53-55 billion so the $55-58 billion suggest buoyant iPhone and iPad sales. If the China mobile deal comes through, Apple could also bring home a positive Q2.

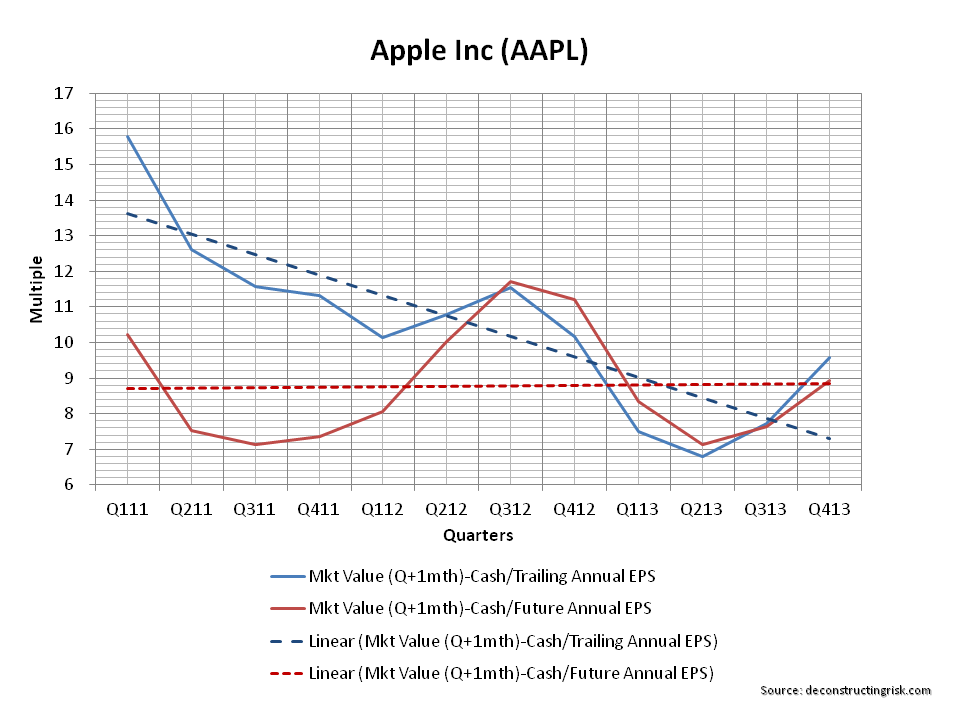

The valuation graph below uses brokers’ estimates on earnings for 2014.

click to enlarge

So, overall, I am content to sit on my limited AAPL position to see what happens in Q1. Adding to the position (or establishing a new position) in AAPL is not advisable, in my opinion, given the current fair valuation, the still uncertain medium term prospects and the overall frothiness in the market right now.