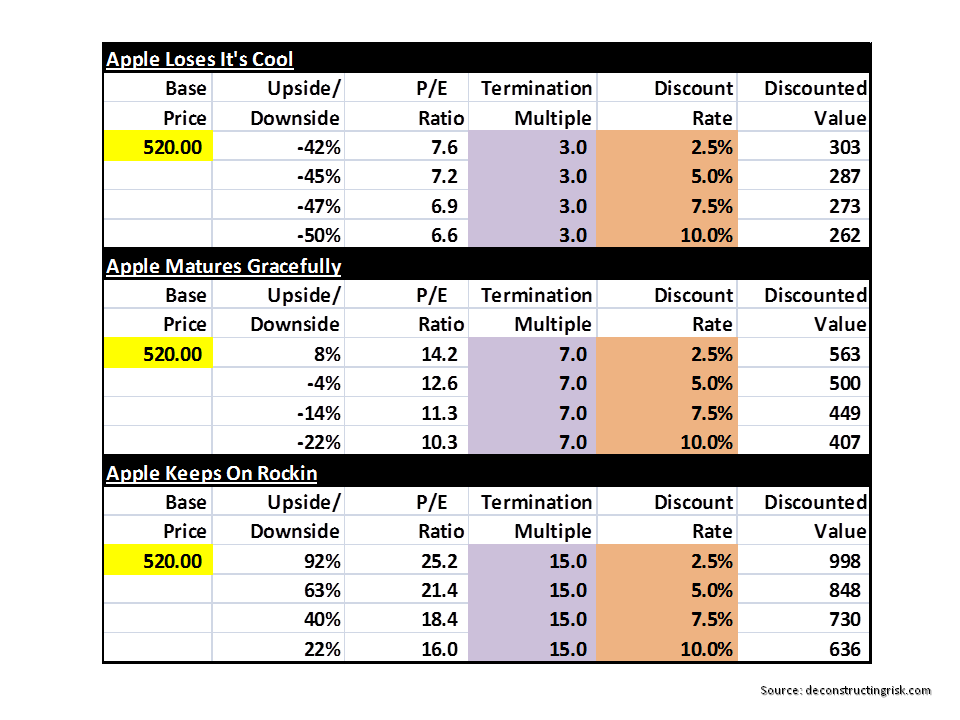

In my previous post on AAPL in April, when the stock was trading around $400, I presented an analysis of three possible scenarios – Apple loses it’s cool, Apple matures gracefully, and Apple keeps on rockin’. Each of these scenarios involved some fanciful assumptions on the trajectory of Apple’s products which I clearly highlighted as likely to prove well off the mark in reality. I did say however, that “the purpose here is not to predict the future but to get an idea of Apple’s valuation given the views prevalent today”.

Well, although a fair amount has happened to AAPL over the past 6 months in relation to an iPhone/iPad/Mac product refresh, a new music steaming service and a number of shareholder friendly actions on buybacks, the hoped for visibility into AAPL’s medium term future remains somewhat elusive and will likely remain so in the short term. The speculated China mobile deal remains a possible short term catalyst.

The three opening observations in my April post do, in my opinion, remain valid: namely, that the iPhone is core to Apple’s future with no new “product category” currently envisaged having the potential to replace the dominant contribution that iPhone makes to profits in the medium term, that gross margins are likely to continue to fall in the face of increased competition, and that a Nokia/Blackberry rapid fall from grace is unlikely given Apple’s ecosystem and loyal customer base (for now!).

There is little point trying to redo the scenarios by replacing one set of assumptions with another so I have simply updated the current share price in the exhibit below.

click to enlarge

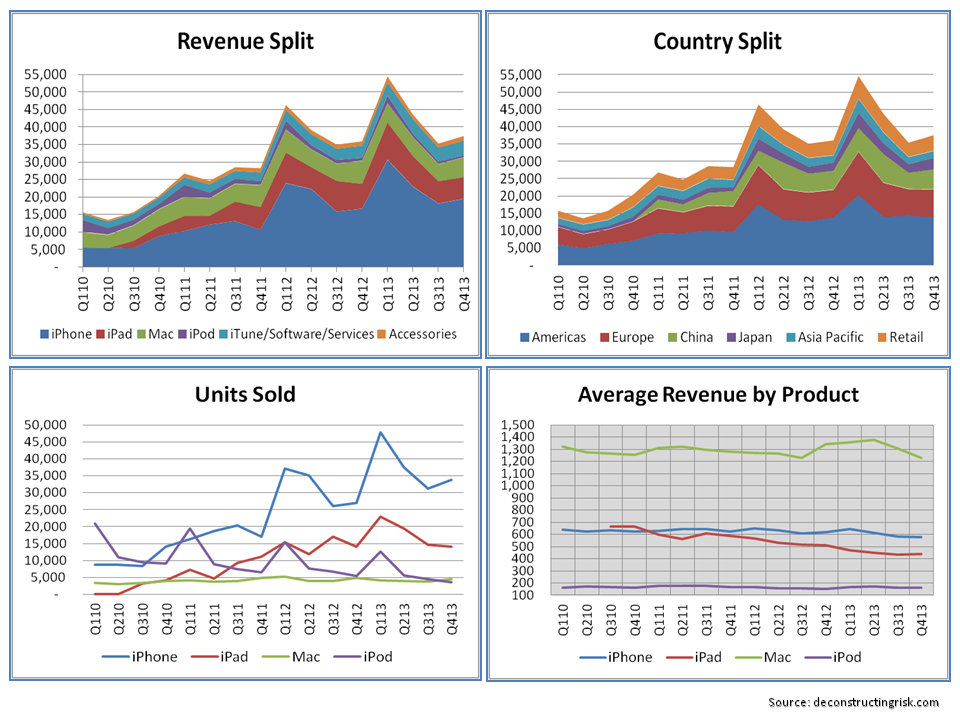

By way of disclosure, I did establish a small position in AAPL 6 months ago around $420, as my April post suggested. Against my expectations outlined in that post, market sentiment on AAPL has clearly moved around the “Apple matures gracefully” valuation from an “Apple loses its cool” bias firmly towards an “Apple keeps on rockin” bias. The exhibit below shows the most recent results from AAPL.

click to enlarge

The degree to which the change in market sentiment on AAPL over the past 6 months is due to underlying fundamentals or simply a function of general market bullishness is open to debate. One factor that cannot be underestimated is Apple’s own buyback programme with approx. 40 million shares repurchased over the past two quarters.

The iPhone and iPad product refreshes have no doubt had an impact on the short term perspective of AAPL. One factor that doesn’t seem to be discussed in the market is whether the product refreshes impact positively or negatively upon Apple’s brand or tests the loyalty of its customer over the longer term.

Market hype from the likes of Carl Icahn should be ignored (my view on the leech that is Mr Carl Icahn is expressed in a previous telecom post) and I don’t understand why Mr Cook is entertaining such distractions.

My own estimates for the holiday Q1 2014 quarter were blown away by Apple’s revenue projections. Based upon recent trends, I was coming up with revenue of $53-55 billion so the $55-58 billion suggest buoyant iPhone and iPad sales. If the China mobile deal comes through, Apple could also bring home a positive Q2.

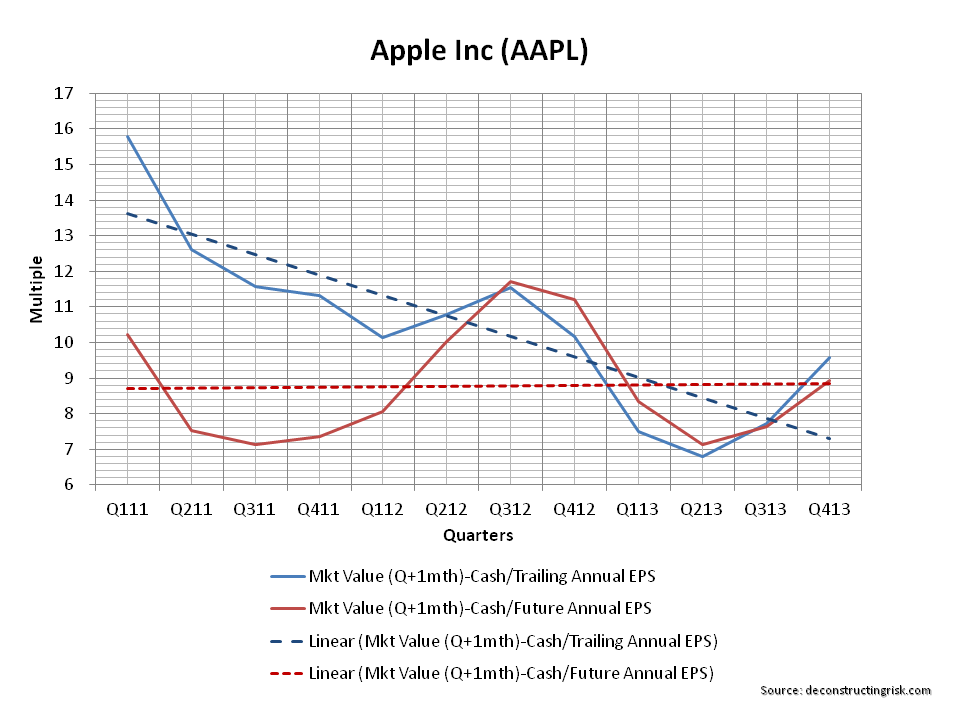

The valuation graph below uses brokers’ estimates on earnings for 2014.

click to enlarge

So, overall, I am content to sit on my limited AAPL position to see what happens in Q1. Adding to the position (or establishing a new position) in AAPL is not advisable, in my opinion, given the current fair valuation, the still uncertain medium term prospects and the overall frothiness in the market right now.

I had a short rendezvous with AAPL when it traded around USD 440. The one issue I finally had and couldn’t solve was Buffet’s question: where is the company in 10 years time ? Honestly, I have no clue…

Cheers,

Eddie

Hi eddie,

I know exactly what you mean, 12 months is a lifetime for AAPL, can’t see a whole lot of upside from here but hanging in there with a small position until new year & hopefully news of China mobile. Not something I plan to get too deep into.

What’s your take on market today? Time to get onto sidelines?

M

Honestly… I am shit-scared right now… No, I am not a perma bear, I just got nervous (and set up some shorts) when the S&P traded around 1400. Things haven’t got better since then. My impression is that the Fed (also the BoE and the BoJ, to some lesser extent the ECB) tries to solve the existing issue of too much debt with even larger amounts of debt. Which works fine as long as the USD behaves well and inflation expectations remain anchored. The issue I have is that there is basically no correlation (not even talking about causation) between short term rates, equity prices, GDP and unemployment. To me it looks like a great psychological stunt that works as long as everybody believes in it (or enough people believe in it which would be sufficient).

So, to put my money where my mouth is, I reduced the allocation to equities in my PA, set up some shorts some time ago and keep plenty of cash. I know I miss some of the party but I rather don’t take the last 10% to 20% gain if that enables me not to take the next 40% or so losses.

Based on some rule of thumb calculations (normalized PEs, average growth of earnings since the 1950s and average growth of divideds) the fair value for the S&P should be somewhere in the 1100 range, give or take. 50 points higher or lower maybe, dunno. Hussman and GMO come to similar conclusions so I guess I am not completly off. This means we either need some very decent profit growth going forward or some adjustment of PEs and prices. And no, I have not the slightest idea when this will happen and how long it takes (I still keep wondering how long it already worked) but I wouldn’t buy the index (same applies eg for the DAX) in size today.

Best,

Eddie

Thanks Eddie for the GMO and Hussman references, I had come across GMO before but hadn’t paid close attention. Both had excellent recent articles and good further reading references. I will put both on my reading list. Loved the “greed discovery” reference from Grantham, think I’ll use that again!

I wasn’t as bearish as you earlier this year but getting very uncomfortable now & can’t fault where you are coming from. Couple of things specifically recently have me nervous, some run-ups in long term fund & stock positions are acting as red flags on over-valuation. Others include recent article in Economist on down trend in core inflation. Really shows the cracks in current monetary policy! What do we do if deflation (particular in Europe) becomes a more credible risk – more QE? Can’t believe that the way out of the aftermath of a burst bubble brought about by over-leverage is to inflate another one! The market is like behaving like a teenager obsessed with the Fed as the saviour & ignoring fundamentals (again! and so soon).

Also noticed a telling statistic in today’s FT that undermines the strong earnings outlook built into valuations – average US family income less now than in 1989 in real terms. That’s the reality on the ground.

I had been reducing positions up until now and considering some insurance on the indices but am now thinking more radical action needed on risk management front. I was trying to hold out until year end to reduce tax on gains but now feel that is silly strategy. As you say, it may not be the top but better to stroll out the exit before the rush! A quote that’s the opposite of “only monkeys pick bottoms” is needed……

M

Be warned that Hussman has been warning about a decline in stocks since about 2011 based on historical data. So far he underestimated what the Fed can do resp is willing to do. Grantham is good stuff, he also published a bunch of papers about demography for example, but make sure you had a good breakfast before reading these :-).

Granted, I tend to err on the conservative side which means that I will miss quite a part of the late party (like right now). What the data tells me (and some smart people like the ones mentioned above confirmed this) however is that you can make significant gains if you don’t take all of the hefty losses that occur from time to time. Think about it: if you loose 25% (not a full blown bear market) you have to gain 33% to make up for the loss. Loose 40% (more or less an average bear market) you have to gain 67%. Loose 50% and we talk about 100% to go (50% would be a nasty bear market but one cannot tule that out). I tend to think that people underestimate the nitty gritty details of percentage calculation.

Feel free to have a look at FRED, the St. Louis Fed portal for economic data. Corporate profits are currently around 12% of GDP. 6% or so are the historical average. Since an economy is a closed system (profits circulate but don’t go in or out) someone has to pay the bill. My bet is that the workers take at least part of it. Which means less money for consumption going forward (which contributes a huge part to GDP).

My advice: forget the tax man… This could be a loosers game :-).

Eddie