Well, I’d put AIG’s Q3 results firmly in the trick basket. The big surprise for me was the nearly $1 billion income tax benefit item in Q3. I wasn’t expecting that.

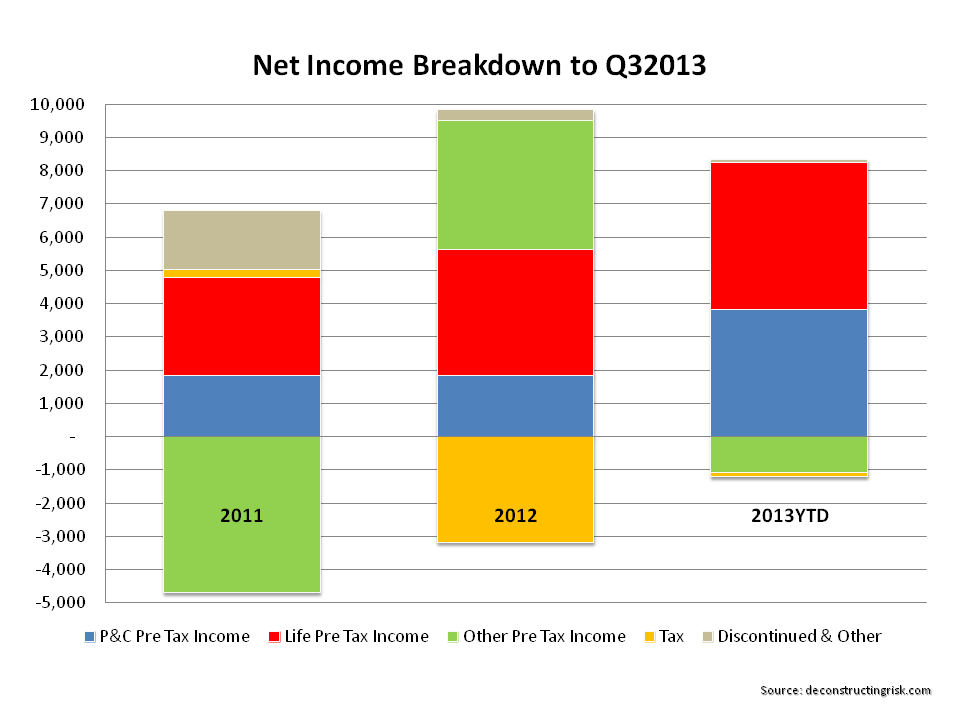

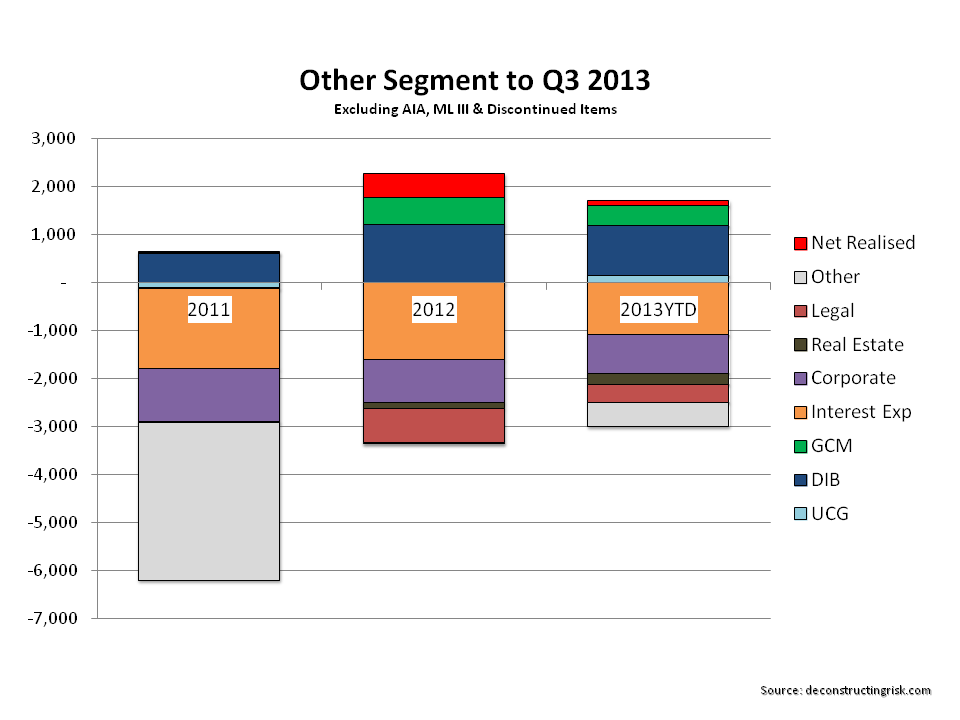

Income before tax was distinctly lacklustre. The P&C technical result was only marginally worse whilst P&C investment income added just over $1 billion of incremental income before tax. Life & retirement only added $400 million of incremental delivered income before tax. The hodgepodge of the other segment had a negative impact of over $1 billion of incremental income before tax due to the marginal increases in GCM and DIB lagging interest, corporate & legal expenses. Updated graphs for net income and the other segment for YTD to Q3 are below.

click to enlarge click to enlarge

click to enlarge

Overall then, I wouldn’t materially change my estimates for a “normal” 2014 (although I may need to reconsider my tax assumptions) and would stick to a book value target of $70 by year end 2014 as being achievable, save any large catastrophes or unexploded bombs. One small treat from the results was the reduction in share count which should continue.

Although the risk/reward is getting more attractive after the price drop to just above $48, I will stay on the side-line as the overall market looks very frothy to me and, as a result, I am currently in risk reduction mode. The uncertainty around the other segment and the lack of clear improvement in the P&C segment may justify the AIG book multiple discount for a while yet.