My last post on AIG concluded that a target of $60-$70 per share over the medium term did not seem unreasonable. However, given the difficulty in predicting a number of moving items in their results and the competitive insurance market, AIG didn’t excite me enough to get involved. Based upon a quick review of the results over H1 2014, that remains my view.

Q2 results were flattered by a gain of over $2 billion on the aircraft leasing sale. Overall the operating results were steady for H1, as the graph below shows, trending towards an approximate $10 billion operating income for 2014. Core earnings from P&C and life & retirement have been steady at approximately $2.5 billion each for the year to date.

click to enlarge

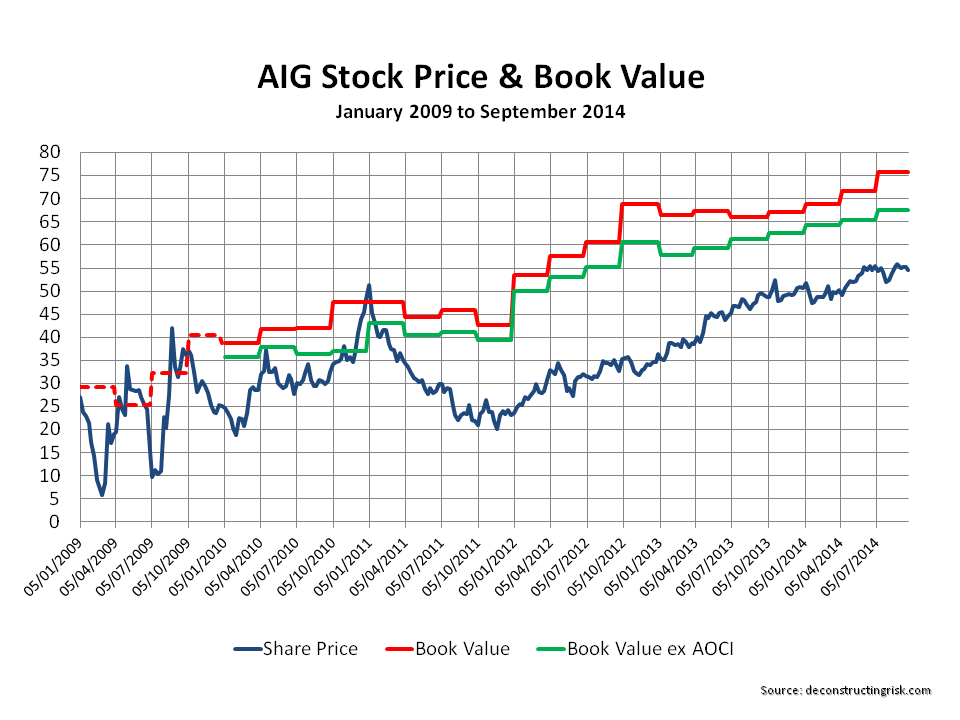

Analysts have an average EPS estimate of $4.62 for 2014, roughly the same as 2013, and $5.00 for 2015 which supports a target share price in the low to mid sixties. The AIG “discount” continues with the stock trading around 80% of book (excluding Accumulated Other Comprehensive Income), as per the graph below.

click to enlarge

Some may argue that this discount is harsh given how far AIG has come. I’m not yet convinced that AIG deserves to come off the naughty step and get a more normal valuation.