In a previous post on AIG I tried to unpick each of the main drivers of the business and predict a “normalised” net income for 2014. Well, my estimate of $7.25 billion of net income for 2013 was blown out of the water by over $4 billion for H2 bringing the 2013 total to $9 billion. This is a massive increase on the $3.4 billion from 2012. A follow-on post in October outlined how I was surprised by a $1 billion tax benefit in Q3.

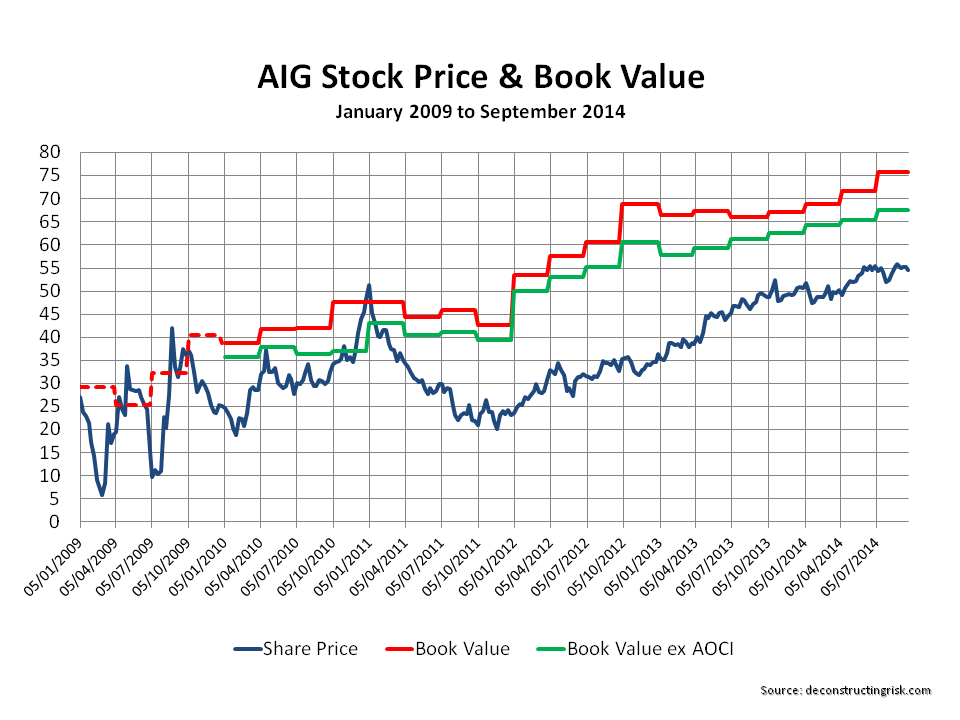

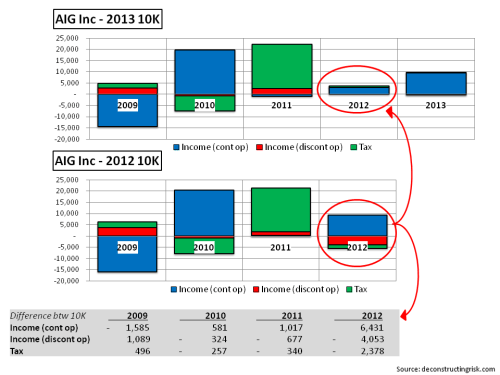

At $49, the stock currently trades at a discount of 71% to book value (incl AOCI) and 76% to book value (excl AOCI). Given the 2013 results and the successful sale of the aircraft leasing business, why is AIG not trading well above $50? Well, one reason may be that outlined in the graphic below.

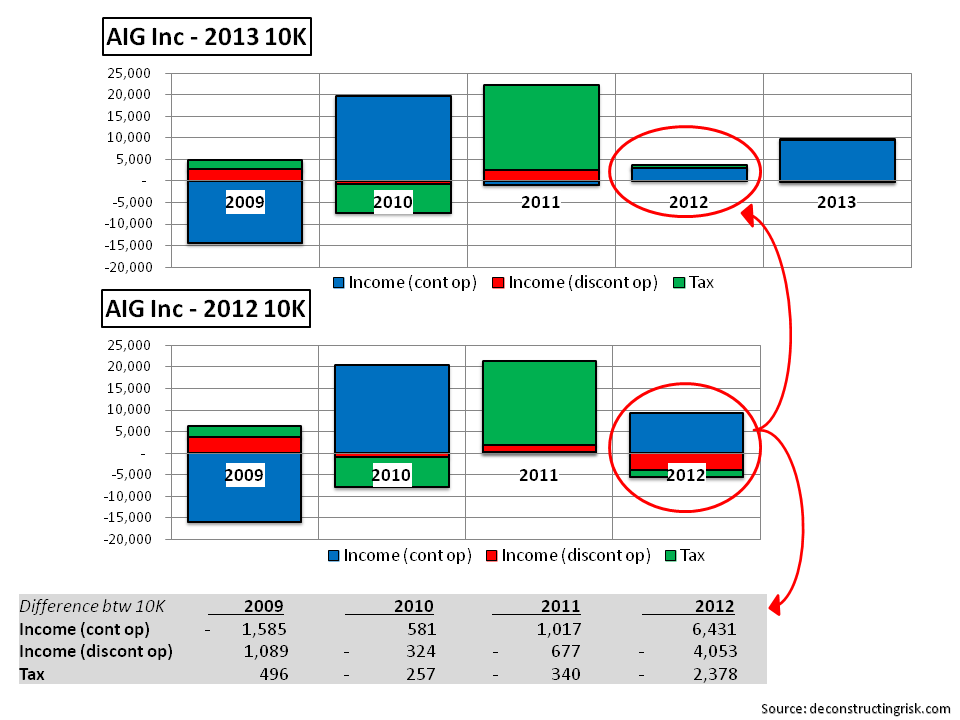

click to enlarge

After the amount of change that AIG has gone through, reinstatements were to be expected. However, you should expect AIGs’ numbers to have stabilized by now and to be more consistent than movements of between $1.6, $0.6 & $1 billion for 2009, 2010, and 2011 as reported between the 2012 and 2013 10Ks. And a staggering $6.4 billion for 2012! How can that be? To be honest, my desire to dig deeper and find an explanation evaporated by the simple fact that it should not happen and my conviction in AIG has dropped commensurate with by disbelief.

If you believe that the movements are for rational reasons and can be taken into account in future estimates, then good luck to you. The exhibits below represents what the latest 10K figures show.

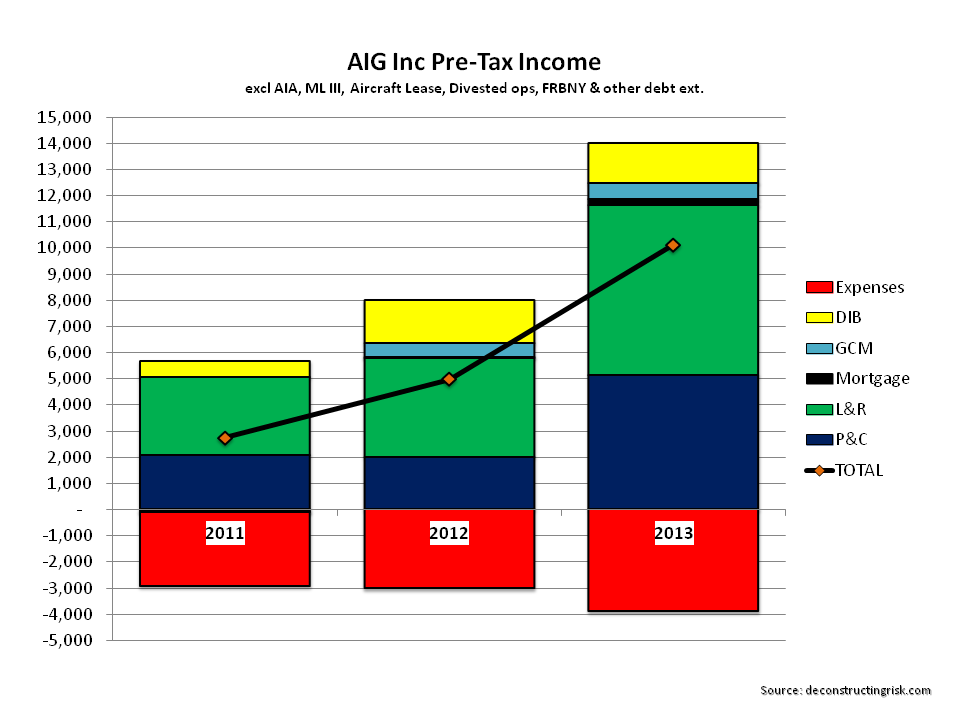

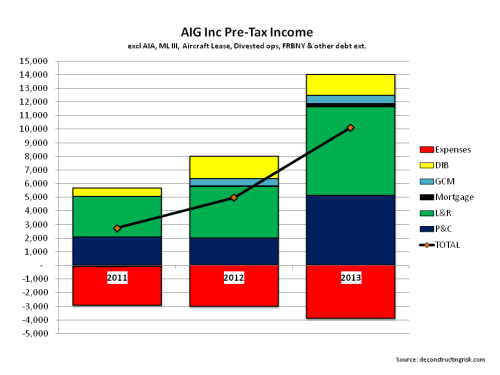

The breakdown of “normalised” pre-tax income below (excluding items from AIA, ML III, aircraft leasing & debt restructures) shows consistent contributions from the “hodge-podge” of the mortgage business, GCM and DIB (combined up to $2.4 billion in 2013 from $2.2 billion in 2012). The P&C contribution is up considerably from 2011 & 2012 around $2 billion to over $5 billion. Life & retirement is also up to $6.5 billion in 2013 from under $4 billion in 2012 and approx $3 billion in 2011

click to enlarge

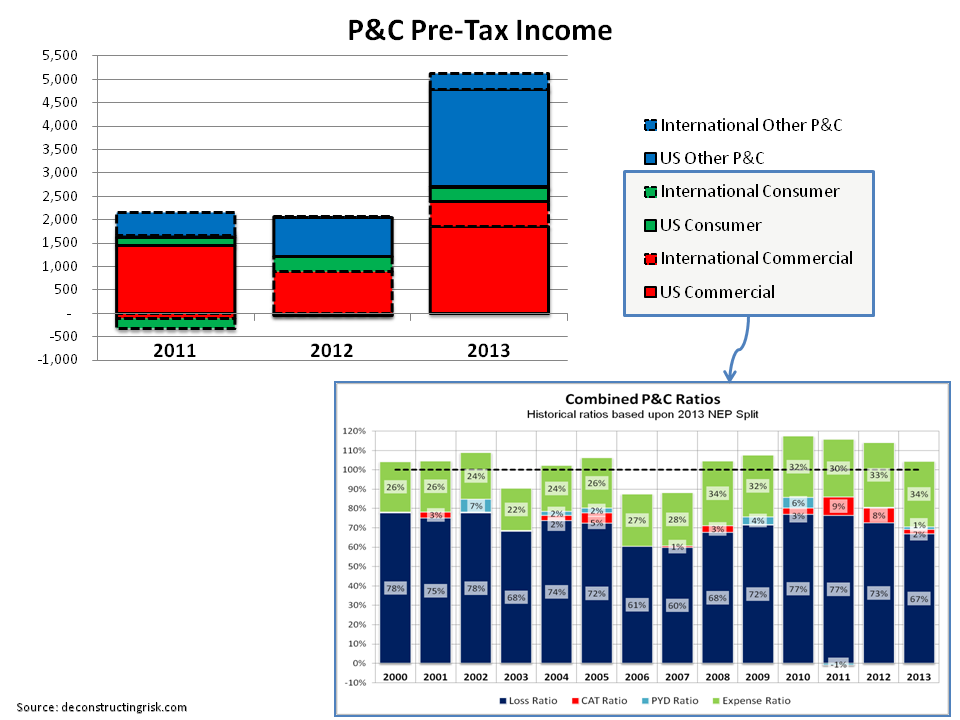

The P&C improvement in pre-tax income is primarily due to improvements in the US commercial & other business lines. The US commercial business benefited from a light 2013 catastrophe year whilst the other business segment had a lower underwriting loss and high investment income. The expense ratio, particularly in the international segment, remains high.

click to enlarge

Life & retirement benefited from good top-line growth, a $1 billion legal settlement, and $2 billion of realized capital gains.

After taking the 2013 trends into account and taking out some 2013 one-offs and including an average US catastrophe year, my previous estimate of a “normalised” $6.5 billion of net income for 2014 and a $60-$70 price target over 12-18 months does not seem unreasonable. That’s if you have confidence in the reported 2013 figures. Which, based upon the first exhibit above, I don’t.