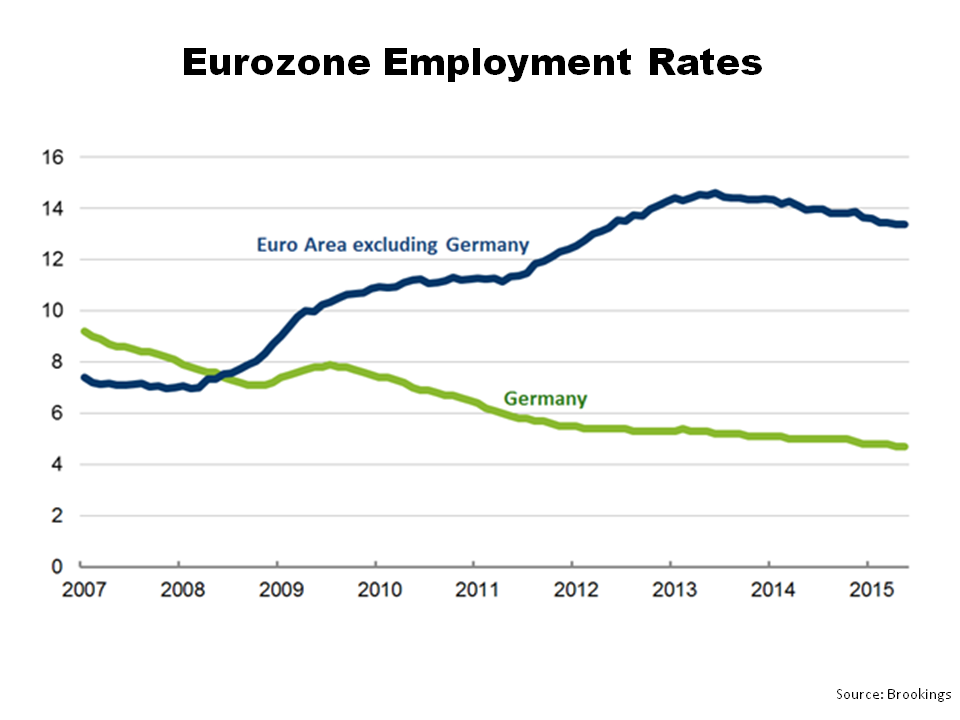

One of the consequences of the Greek tragedy that has played out over the last few months is a growing realisation that Europe can no longer paper over the design faults at the heart of the Euro project. As Ben Bernanke points out in a recent blog, the “promise of the euro was both to increase prosperity and to foster closer European integration” and suggests what is needed now to fulfil that dream is an official European mechanism to ensure “that creditor as well as debtor countries have an obligation to adjust over time (through fiscal and structural measures, for example)”. The reality of the European positions played out over Greece, particularly from Germany, is that the prospect of any agreement on such a fiscal mechanism is pure fantasy. A striking graph from Bernanke’s post illustrates how beneficial the Euro has been to Germany compared to the rest of the Eurozone.

click to enlarge

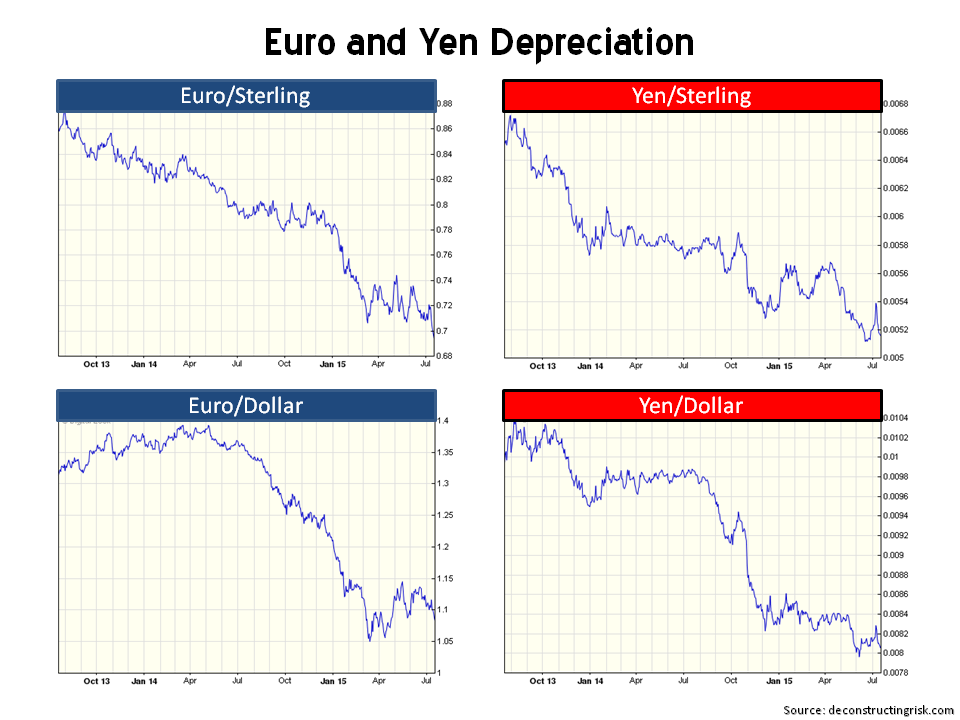

The Euro has been exposed as a fixed exchange rate system, only marginally stronger than those that came before it, which has inflated Germany’s large trade surplus and placed the burden of real wage adjustment on countries with trade deficits. Mario Draghi’s QE programme is inflating Germany’s trade account surplus further, now estimated at 7%, through the competitive devaluation of the Euro. With the negative impacts of the Euro’s fall being countered by falling commodity prices, you would think that Germany would appreciate the economic benefits of the Euro it bestows on them even more now than ever. The graph below shows the fall of the Euro against the dollar and sterling compared to the QE daddy of them all Japan (which has failed miserably to raise workers real earnings).

click to enlarge

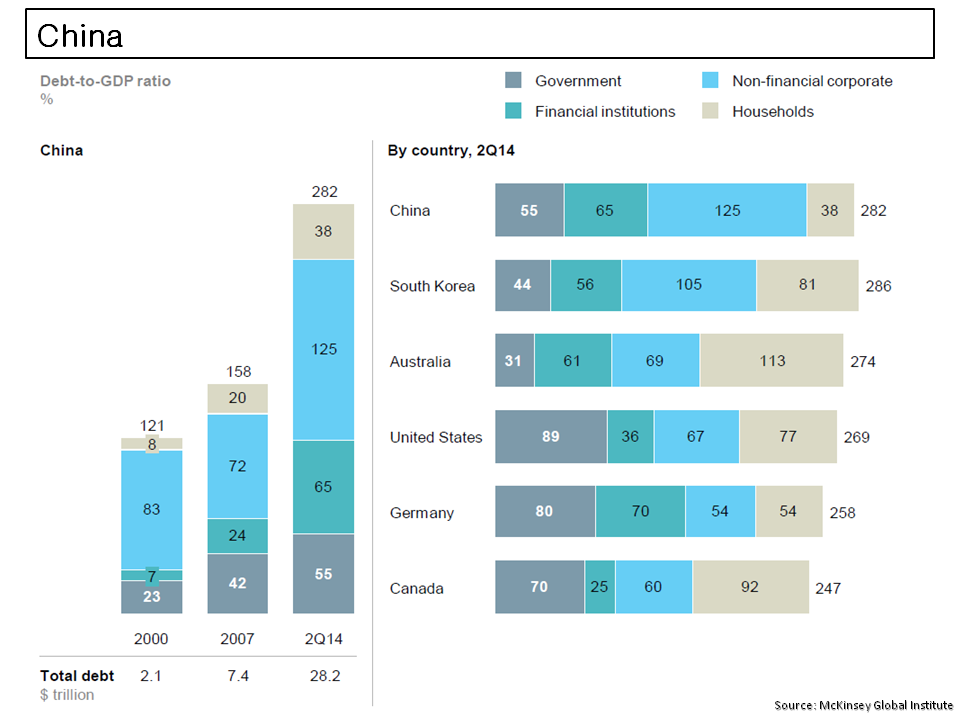

The extraordinary (and rather crude) acts of the Chinese in recent months to counter the latest bubble, this time in the stock market, illustrates too well the dangers of over-leverage to China’s developing experiment with capitalism. State sponsored championing of stock market rises, particularly through additional leverage, smacks of folly. Colin Powell’s quote “if you break it, you own it” comes to mind. The McKinsey deleveraging report (see previous post) from last year detailed the rise in Chinese debt, as per the graph below.

click to enlarge

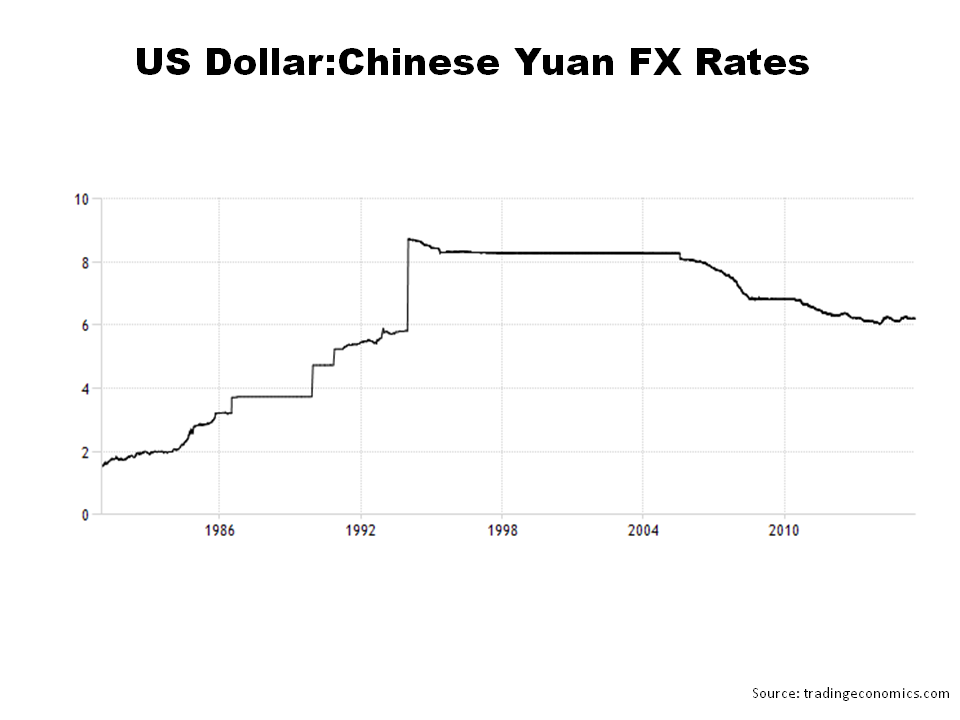

Some analysts speculate that China may join the currency wars and turn to the competitive devaluation game later this year to inflate business profits, although any such move will likely not be considered until after the IMF decides on whether to include the Chinese currency in the special drawing rights basket used for holding their reserves. A rise in US interest rates later this year will likely further strengthen the dollar and may prove too much for the Chinese. By widening the fixed trading bands at which the yuan is allowed to trade against the dollar, Chinese authorities may try to counter the competitive impacts of the yen and Euro depreciation. The historical exchange rate of the dollar:yuan is depicted below.

click to enlarge

Were China to join the currency wars to boost their economy, the beggar thy neighbour strategy may get increasing dicey for the developed economics currently embracing competitive devaluation as a means of curing their ills. Germany may have to rethink its dependence on export led growth after all and may come to regret their recent actions in exasperating the underlying fault lines in the Euro.