The results of the EBA stress tests on the largest European banks were released on Friday night. As expected, the Italian bank Monte Paschi performed badly. Rather than go into the results at a individual bank level, I thought it would be interesting to look at the results at a country level.

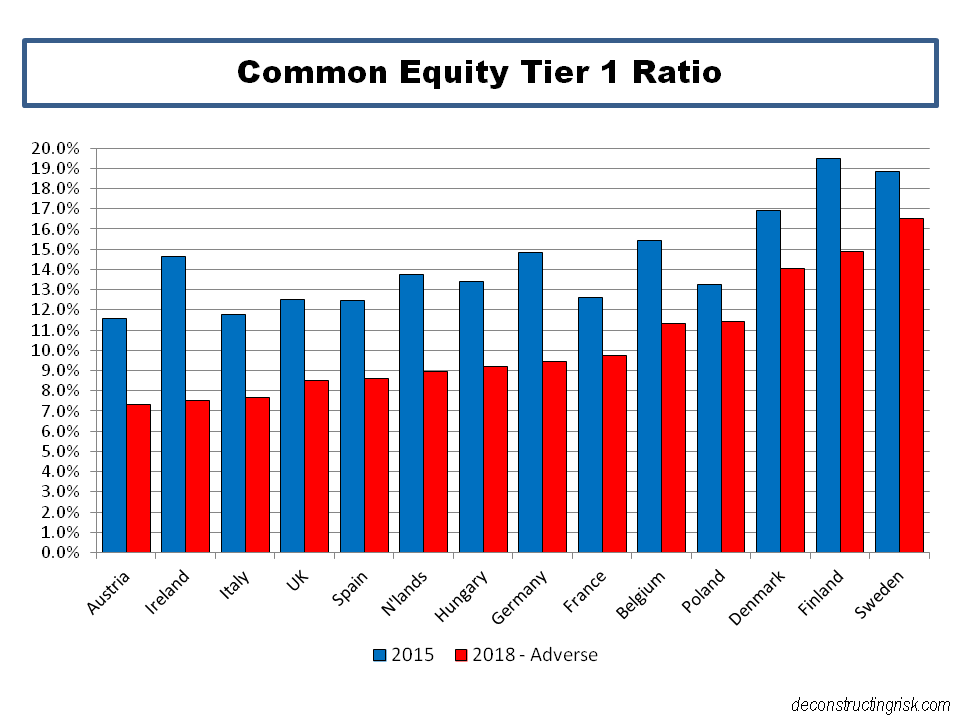

The first graph below shows the movement in the common equity tier 1 ratios under the adverse scenario by country.

click to enlarge

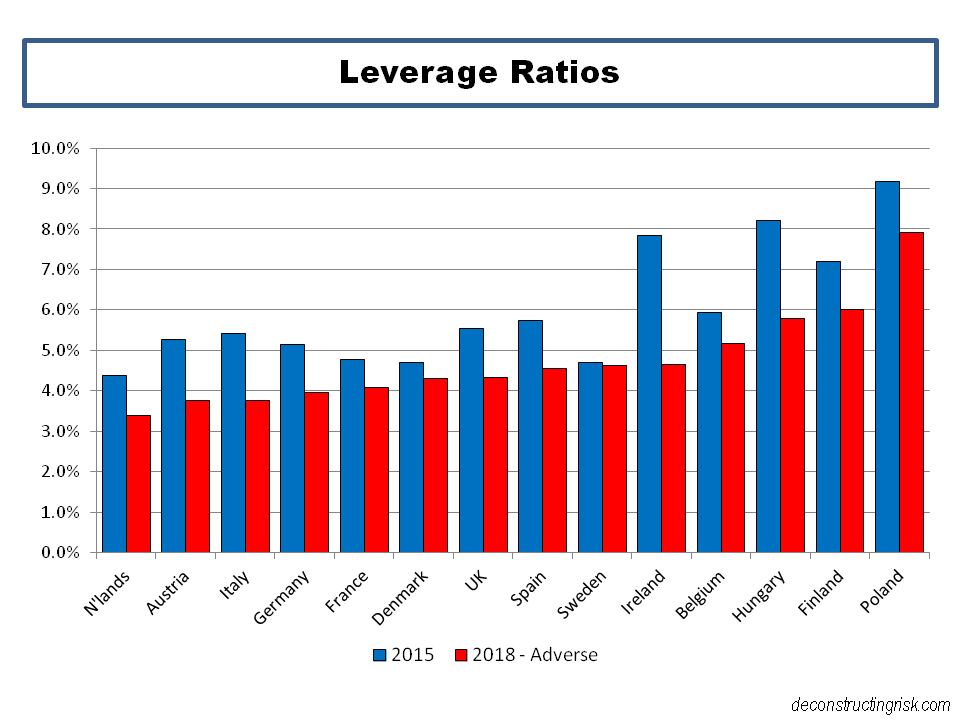

The next graph below shows the movement in the leverage ratios under the adverse scenario by country.

click to enlarge

On the CET1 ratios, Ireland and Austria join Italy as the countries with the lowest aggregate ratios. The fall in Ireland’s ratios is particularly noticeable. In terms of the leverage ratios, Italy and Austria again appear in the bottom of the list. Perhaps surprisingly, the Netherlands is the lowest with Germany and France around 4%.

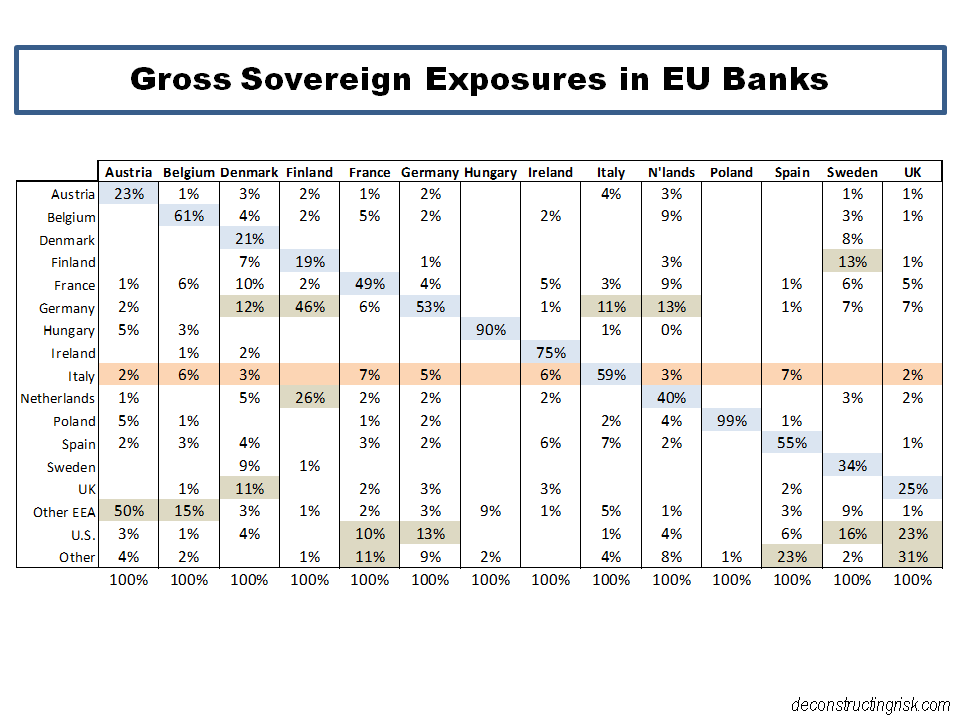

Another interesting piece of data from the EBA is the profile of sovereign exposures in the EU banks. In the exhibit below, I looked at these exposures to see if there is any insight that could be gained on risks from any potential breakup of the Euro (not a risk that’s talked about much these days but one that hasn’t gone away in my view).

click to enlarge

A few things come to mind from this exhibit. Germany bonds are not held in as high quantities as I would of expected (except for the weird 46% from Finland, with other concentrations in Denmark, Italy and the Netherlands), likely to be a function of their yield. The strongest capitalized countries – Denmark, Finland and Sweden – have the lowest holding in their own bonds, with Denmark and Sweden having a particularly diverse spread of holdings. Italian bonds are widely held across a number of countries but not in large concentrations. Ireland holds most of the Irish exposure.

There is likely more food for thought among the interesting data released by the EBA from these bank stress tests.