There have been some interesting articles published over the past week or so to mark the five year anniversary of the Lehman collapse.

Hank Paulson remembered the events of that chaotic time in a BusinessWeek interview. He concluded that despite having a hand in increasing the size of the US banks like JP Morgan and Bank of America (currently the 2nd and 3rd largest global banks by tier 1 capital) “too big to fail is an unacceptable phenomenon”. He also highlighted the risk of incoherence amongst the numerous US and global regulators and that “more still needs to be done with the shadow-banking markets, which I define to be the money-market funds and the so-called repo market, which supplies wholesale funding to banks”.

Another player on the regulatory side, the former chairman of the UK FSA Adair Turner, continued to develop his thoughts on what lessons need to be learnt from the crisis in the article “The Failure of Free Market Finance”, available on the Project Syndicate website. Turner has been talking about these issues in Sweden and London this week (which essentially follow on from his February paper “Debt, Money and Mephistopheles: How Do We Get Out Of This Mess?”). where he argues that there are two key issues which need to be addressed to avert future instability.

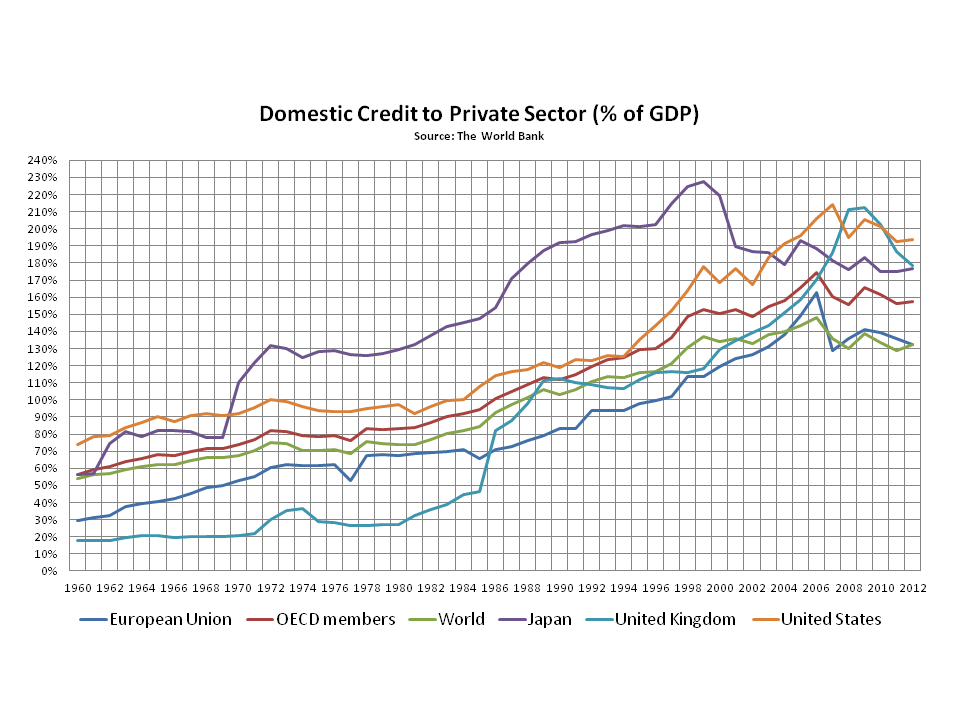

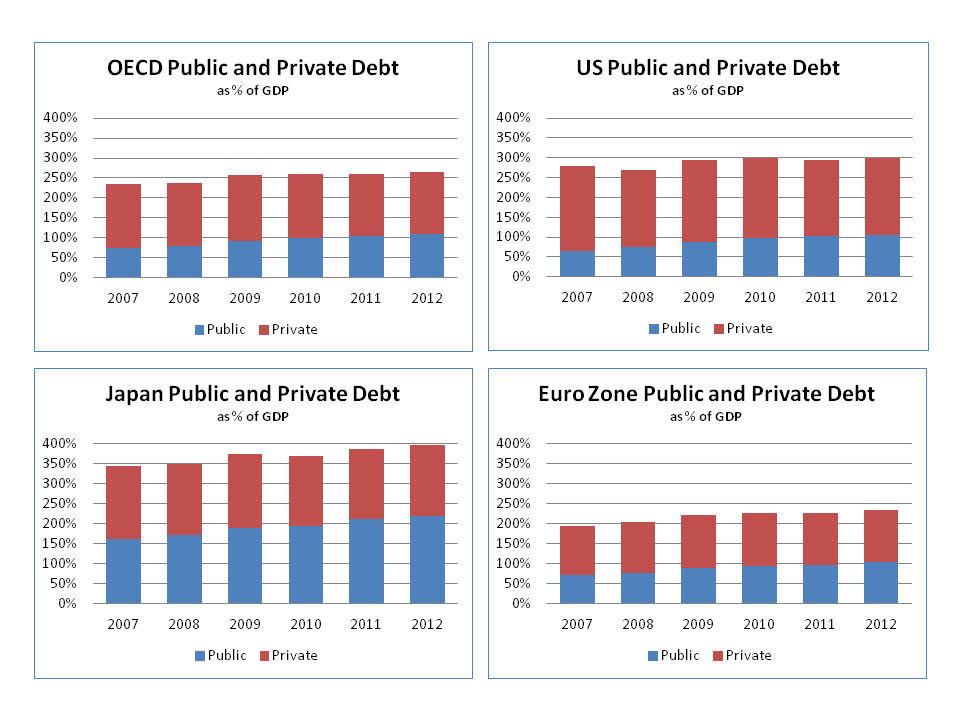

The first is how to continue to delever and reduce both private and public debt. Turner believes that “some combination of debt restructuring and permanent debt monetization (quantitative easing that is never reversed) will in some countries be unavoidable and appropriate”. He says that realistic actions need to taken such as writing off Greek debt and a restructuring of Japanese debt. The two graphs below show where we were in terms of private debt in a number of jurisdictions as at the end of 2012 and show that reducing levels of private debt in many developed countries have been offset by increases in public debt over recent years.

click to enlarge

The second issue that Turner highlights is the need for global measures to ensure we all live in a less credit fuelled world in the future. He states that “what is required is a wide-ranging policy response that combines more powerful countercyclical capital tools than currently planned under Basel 3, the restoration of quantitative reserve requirements to advanced-country central banks’ policy toolkits, and direct borrower constraints, such as maximum loan-to-income or loan-to-value limits, in residential and commercial real-estate lending”.

Turner is arguing for powerful actions. He admits that they effectively mean “a rejection of the pre-crisis orthodoxy that free markets are as valuable in finance as they are in other economic sectors”. I do not see an appetite for such radical actions amongst the political classes nor a consensus amongst policy makers that such a rejection is required. Indeed debt provision outside of the traditional banking systems by way of new distribution channels such as peer to peer lending is an interesting development (see Economist article “Filling the Bank Shaped Hole”)

Indeed the current frothiness in the equity markets, itself a direct result of the on-going (and never ending if the market’s response to the Fed’s decisions this week is anything to go by) loose monetary policy, is showing no signs of abating. Market gurus such as Buffet and Icahn have both come out this week and said the markets are looking overvalued. My post on a possible pullback in September is looking ever more unlikely as the month develops (S&P 500 up 4% so far this month!).

Maybe, just maybe, the 5th anniversary of Lehman’s collapse will allow some of the voices on the need for fundamental structural change in the way we run our economies to be heard. Unfortunately, I doubt it.