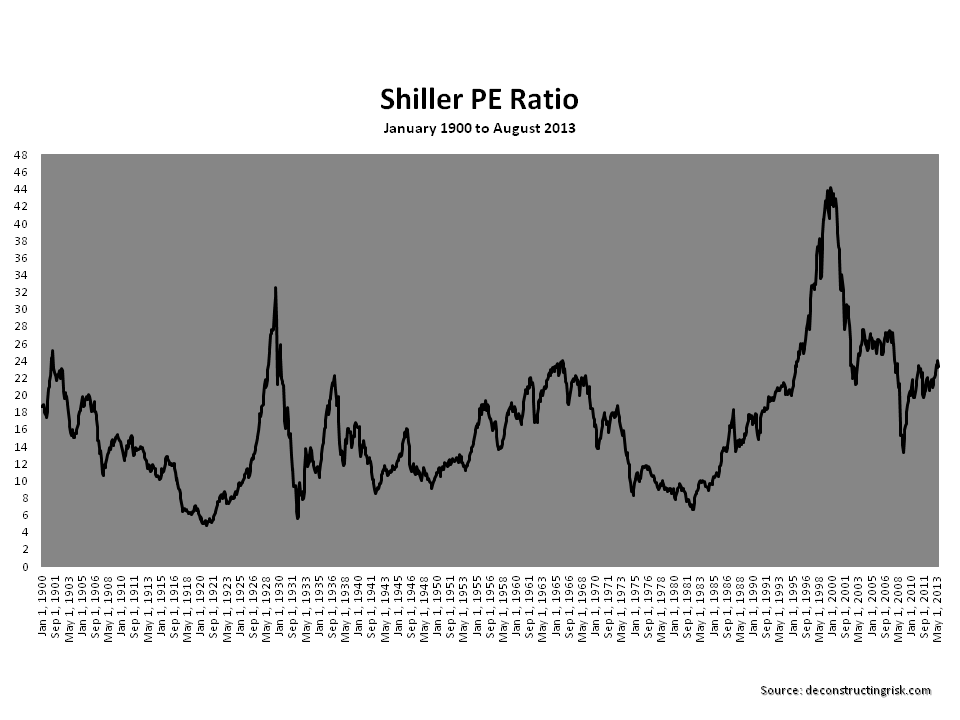

Following on from last week’s post citing the Shilling PE ratio, also called the cyclically adjusted price earnings ratio or CAPE, there was an interesting article in today’s FT referring to Jeremy Siegel’s previous critique of Robert Shiller’s bearish CAPE.

Siegel points to the current S&P500 level at a 15 to 16 times 2013 estimated earnings as being close to its historical average suggesting the CAPE is overtly negative. Siegel points out that the CAPE has been bearishly above its long term average for the past 22 years, except for a brief 9 month spell.

Siegel believes that the underlying earnings in the calculation need to be adjusted for accounting changes in the 1990s that required downward only adjustment to book values when asset prices are depressed without a rebalancing upwards when asset prices are rising. According to Siegel, using more appropriate National Income and Product (NIPA) profit data in the CAPE calculation results in a much more bullish CAPE indicator.

Another issue with the underlying data is the increase in profit margins over the past 15 years due to varying (and generally lower) global corporate tax rates, the rise of technology firms with fatter margins, and generally stronger corporate balance sheets.

Finally, Siegel points to the macroeconomic environment whereby periods of low interest and inflation rates justify higher PE ratios.

The FT article points to research by the London Business School that indicate the CAPE based upon data available at the time (“out of sample date”) is a poor historical indicator for timing entries and exits in the market. The research concludes there is no consistent relationship between forecasts and outcomes.

This research and Siegel’s criticism make valid points. Historical data does need to be viewed in the context of the reporting standards of the time. However, I would be sceptical about arguments about higher long term margins and that the current macro environment justifies higher multiples (as highlighted in a previous post). The fact is that we are in unchartered territory in terms of massive Central Bank market intervention and the macro environment across the globe presents considerable challenges in getting back to a normalised situation.

The fact that Shiller’s CAPE has been bearish for so long may make the case for some adjustment. The difficulty is that once we start making adjustments to fit the current situation the validity of the underlying metric is compromised. It is too simplistic to look at a single measure to justify investment decisions. Equally ignoring one measure over another when they indicate contrary views is naïve. Overall, I am more in the Shiller camp than the Siegel camp. Notwithstanding my expectation that we are due some Autumn volatility, I would purchase quality stocks on the dip if their valuation justified it. But the macroeconomic environment scares me so I am conscious of Andres Drobny’s advise that following the financial crisis one should always “change your views as facts change“. The difficulty, of course, is knowing when the facts are changing before its too obvious (and in all likelihood too late)!