The book “Capital in the Twenty-First Century” by Thomas Piketty is unquestioningly one of the books of 2014. This blogger is currently reading Piketty’s book after finding it in his Santa sock this Christmas. There were not many other books from 2014 that caught my attention. One book that I am very much looking forward to in 2015 is the new Steven Drobny book “The New House of Money” with detailed interviews of money managers. On his website, Drobny has already released the first two chapters – one on Kyle Bass and the other with Jim Chanos.

The views of Kyle Bass, in particular, on Japan got me thinking again about demographics and the ability to withstand large debt loads. The views of Bass are also articulated in a piece on the investor perspectives website. For example, Bass states that currently in Japan debt repayments take up 25% of government tax revenues but that a 100bps rise in interest rates in Japan would mean that 100% of tax revenues would go to repayments. That leaves very little room for error!

This week, Buttonwood also has an article on the restrictions that large debt loads places on the effectiveness of monetary policy.

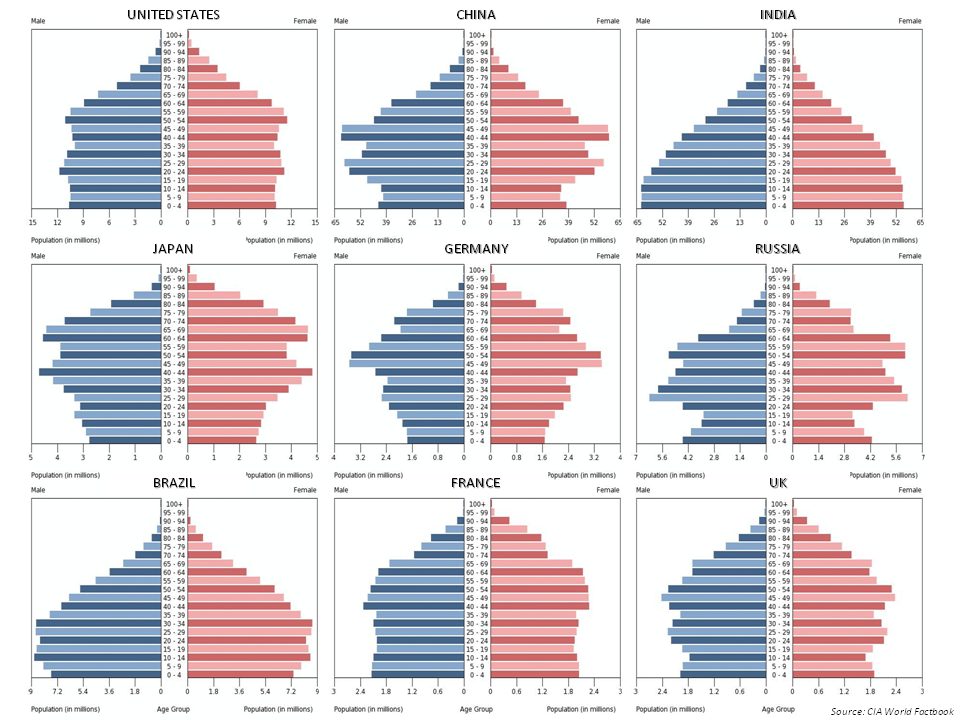

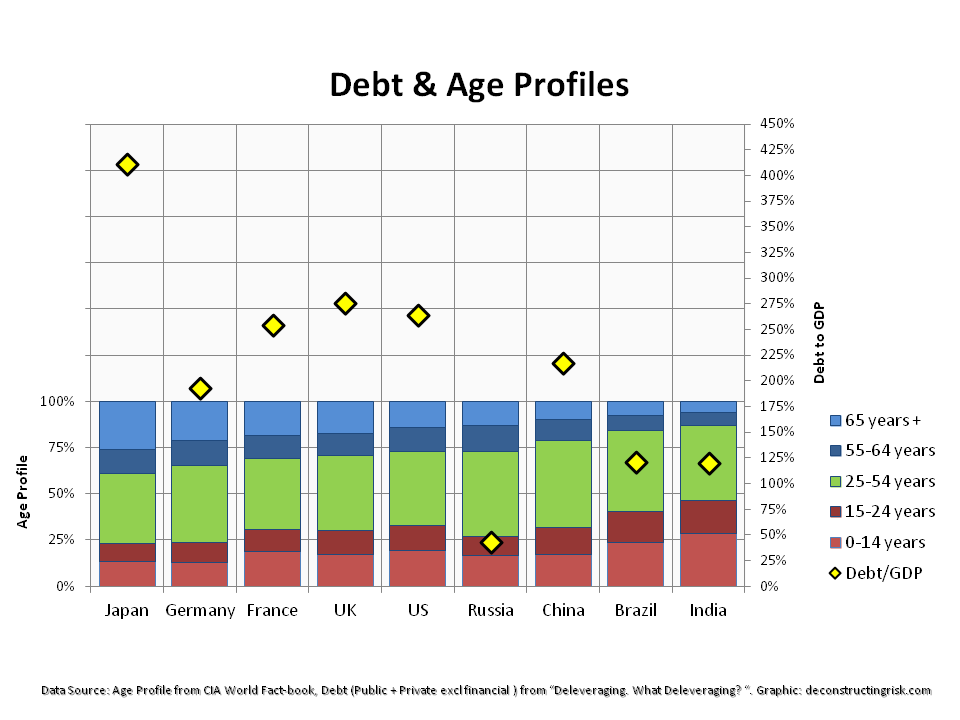

In terms of age profiles, the graphic below shows the profiles of the 9 largest economies (according to the World Bank).

click to enlarge

Japan and Germany clearly stand out as countries with an aging population, currently with 26% and 21% of their populations over 65 respectively. I also compared the age profiles against the public and private debt figures (excluding that from banking and other financial service firms) from the “Deleveraging. What Deleveraging?” report (see previous post on that report), as per the graph below.

click to enlarge

The graph does show that there is a clear relationship between debt loads and age profiles, particularly the percentages for the over 55s. However, the outliers of Germany and Russia on the low debt side and indeed Japan on the high debt side show that there are many other factors at play, not least the historic cultural characteristics of each country. The burden that high debt loads places on future generations is clearly an important policy issue for the global economy, one that will become ever more important if interest rates are to return to anyway close to normality.

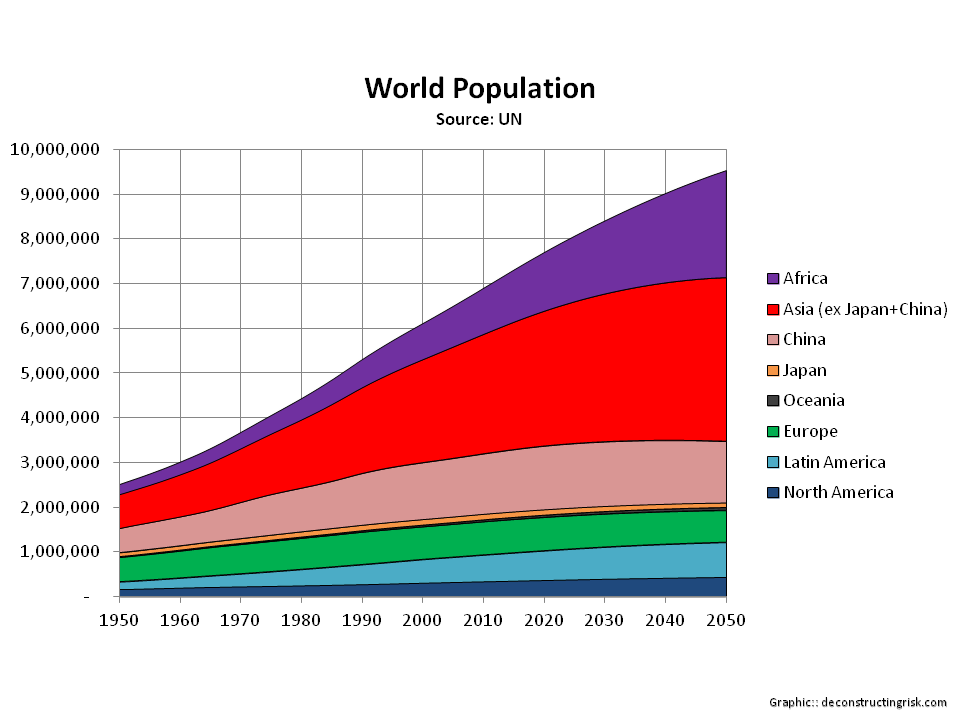

As a follow-on to this post, I have been looking through the UN population projections and the following graphs represent population profiles I found interesting. The first is the world population historical figures and projections by age profile.

click to enlarge

The next graph is the world population split by continent (with Japan and China split out of Asia).

click to enlarge

And finally, a graph of the world population aged over 60 and aged under 15 split by continent.

click to enlarge