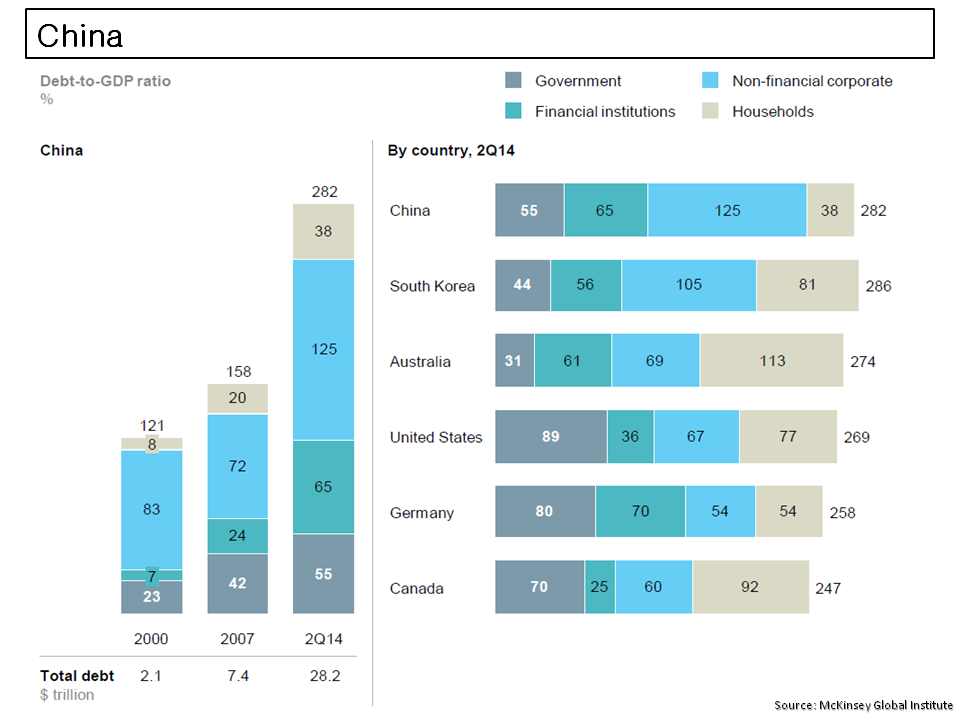

McKinsey released their third report on global debt levels recently, entitled “Debt and (not much) Deleveraging”. Covering much of the same ground as the Geneva report in September (see previous post), the highlights of the report include detail behind the rise in public sector and household debt, the growth rates needed to start real deleveraging, the higher capital levels in the banking sector, the detail behind China’s rising debt, and some suggestions to live with high debt levels in the future. I would recommend the report to anybody interested in the macroeconomics.

The report is the subject of the Buttonwood piece this week where he also talks about the challenges that higher global debt brings. A recent post on changes to global demographic profiles is also relevant when thinking about servicing future public and private debt.

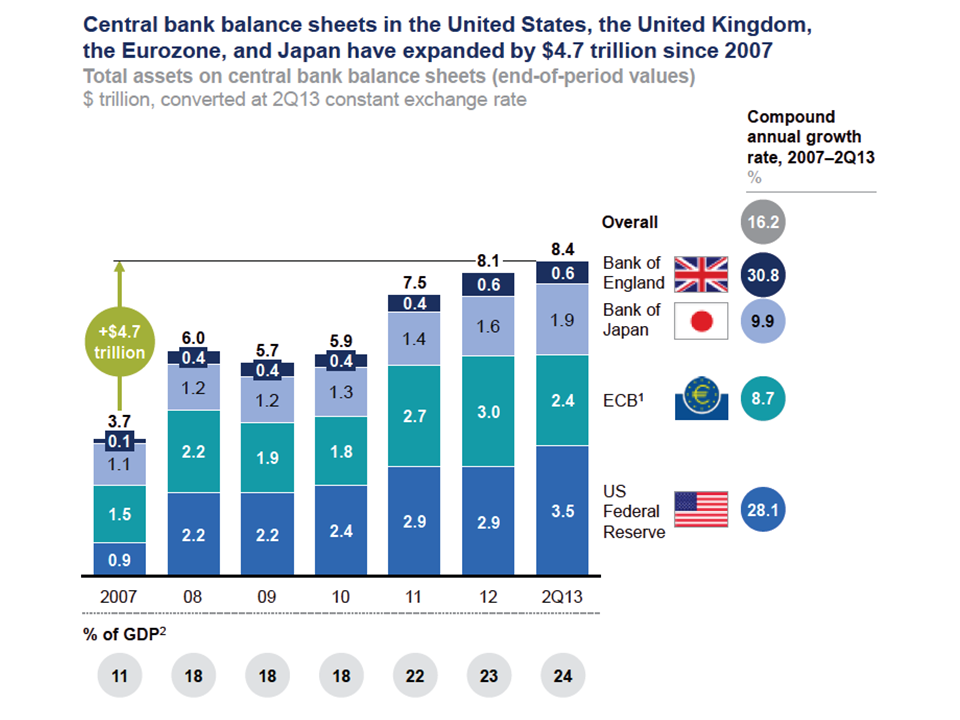

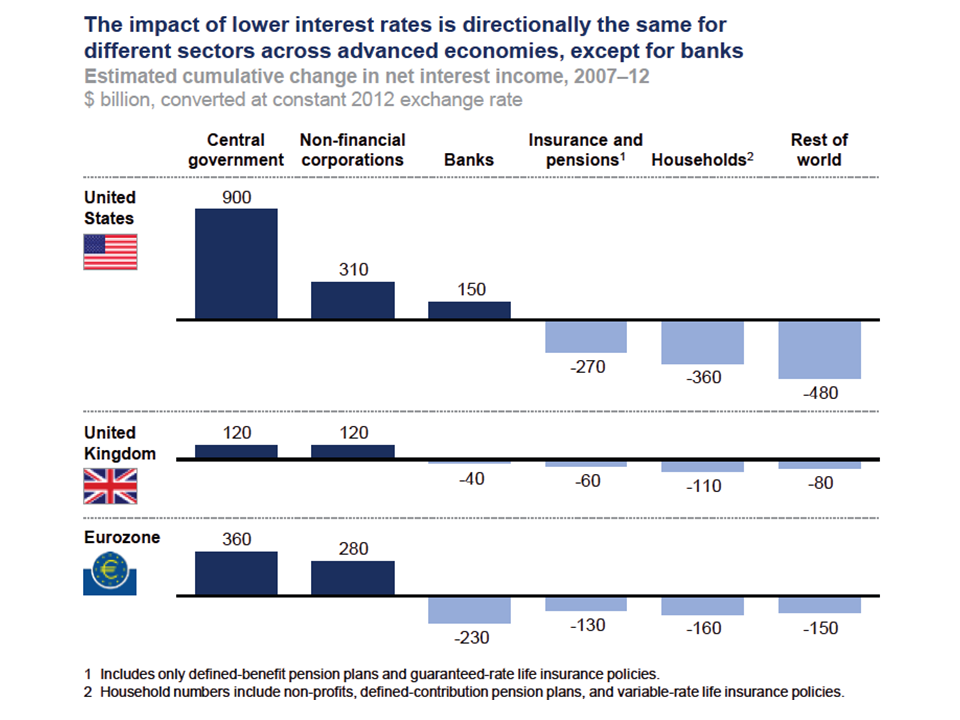

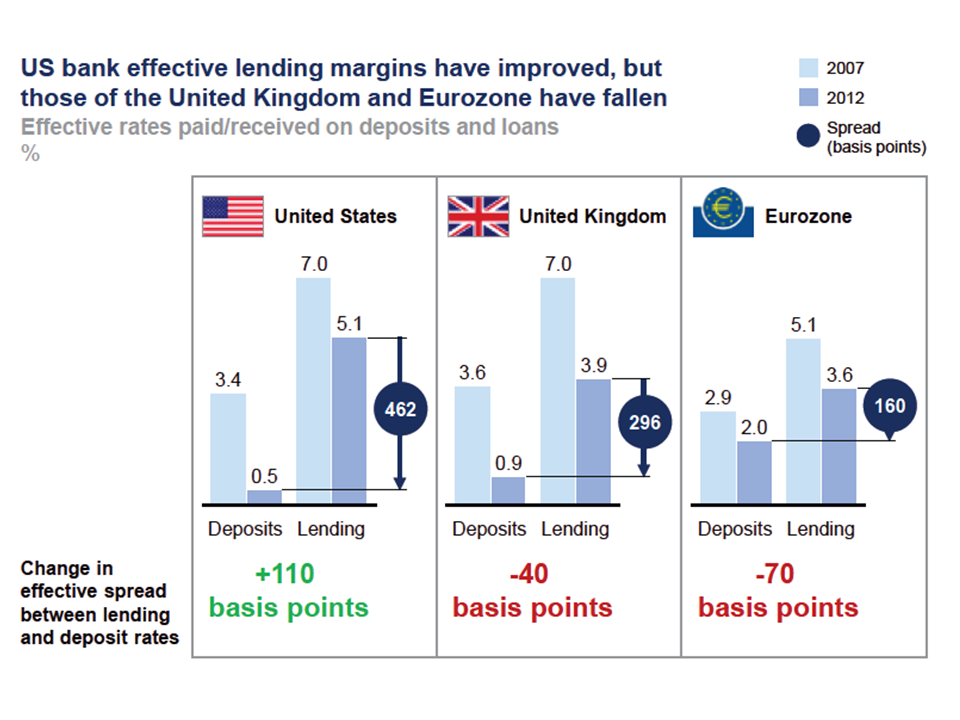

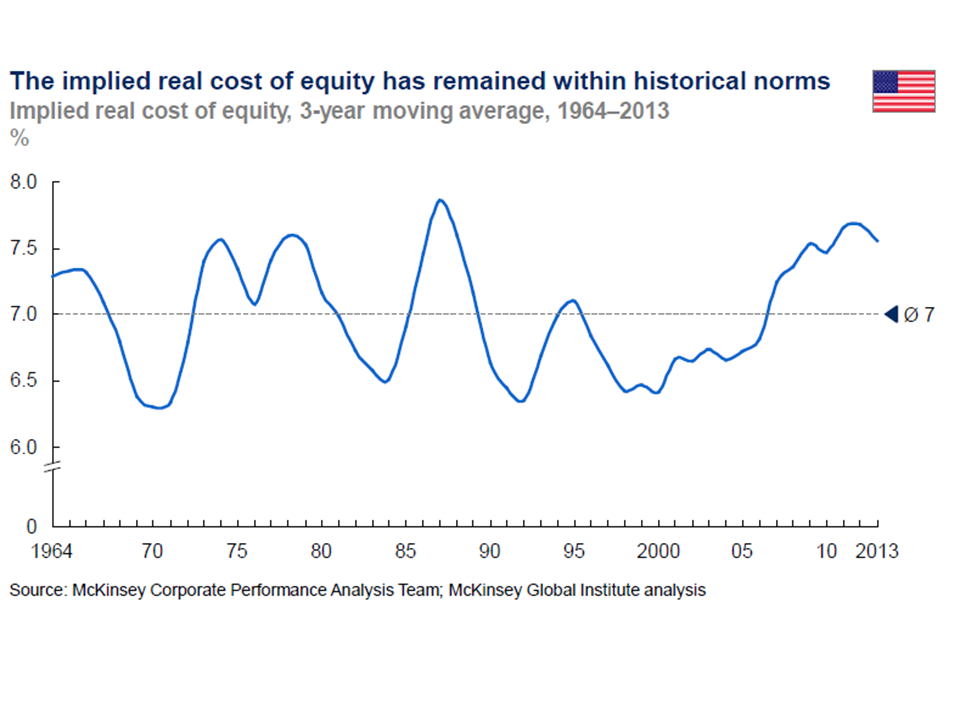

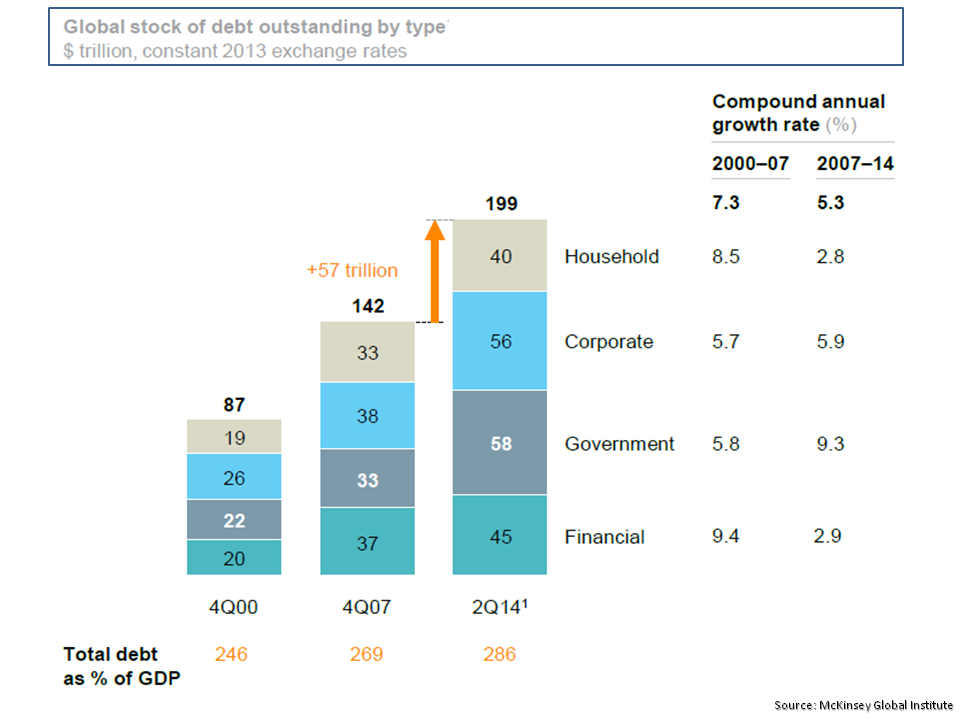

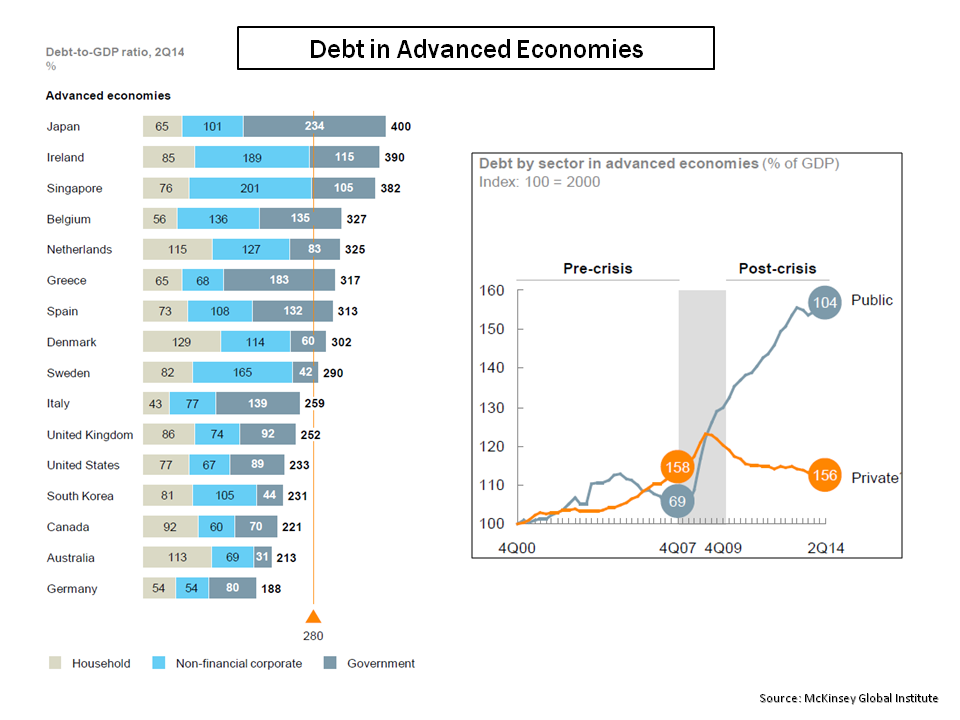

Below are a few of the graphics of interest from the report on the size and split of global debt, the mix between private and public debt in developed countries and the growth rate needed to start deleveraging, and the debt in China.

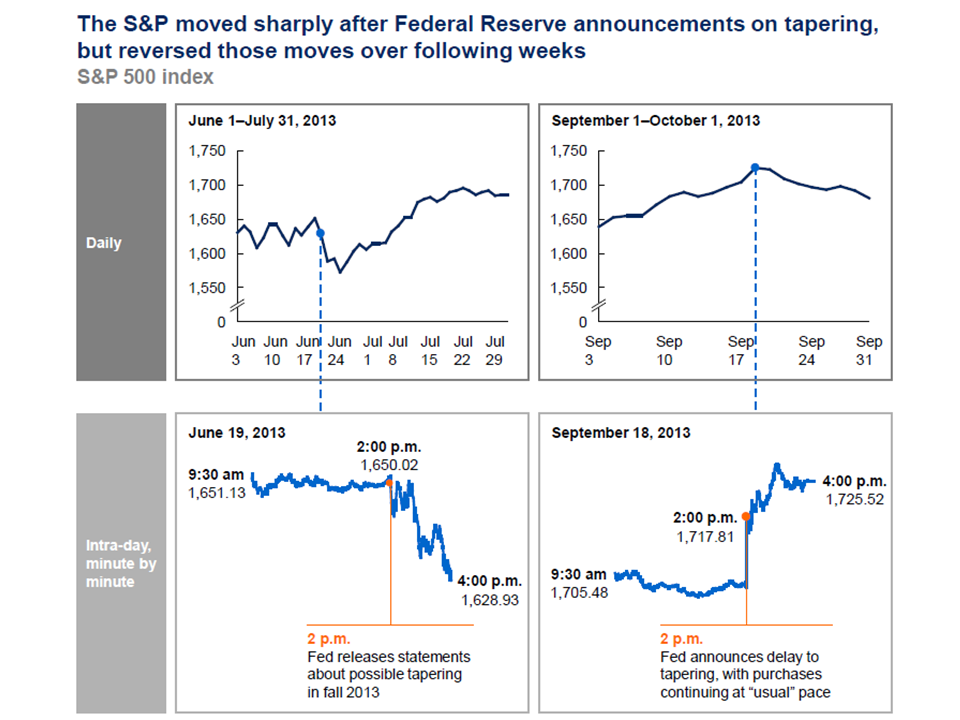

click to enlarge

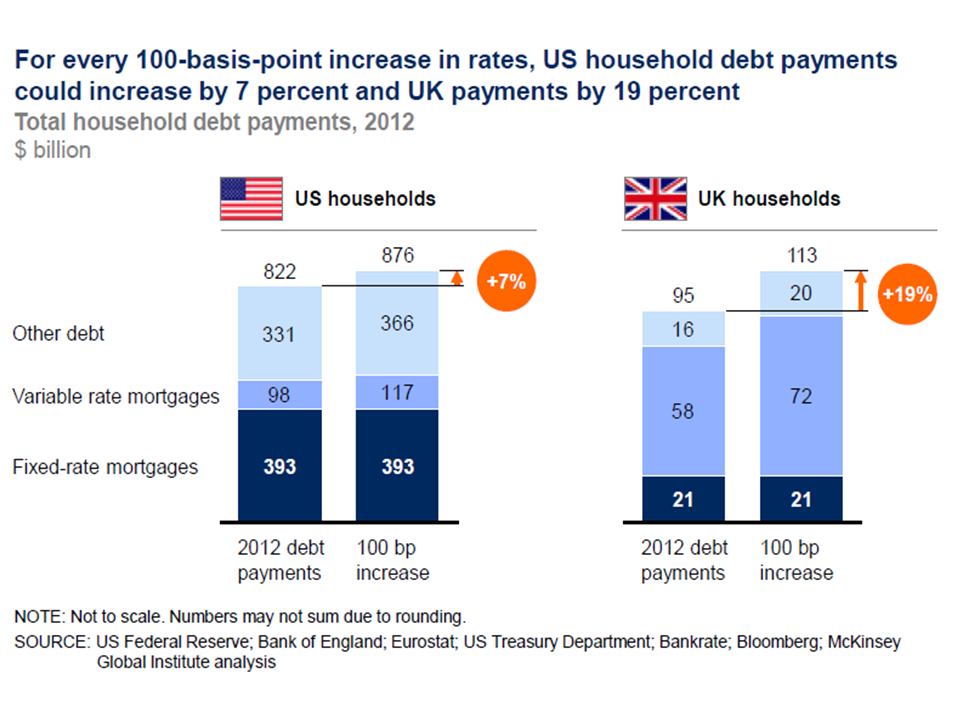

click to enlarge

click to enlarge

click to enlarge