Are you so blind that you cannot see?

Are you so deaf that you cannot hear?

Are you so dumb that you cannot speak?

Jerry Dammers

Are you so blind that you cannot see?

Are you so deaf that you cannot hear?

Are you so dumb that you cannot speak?

Jerry Dammers

Posted in General

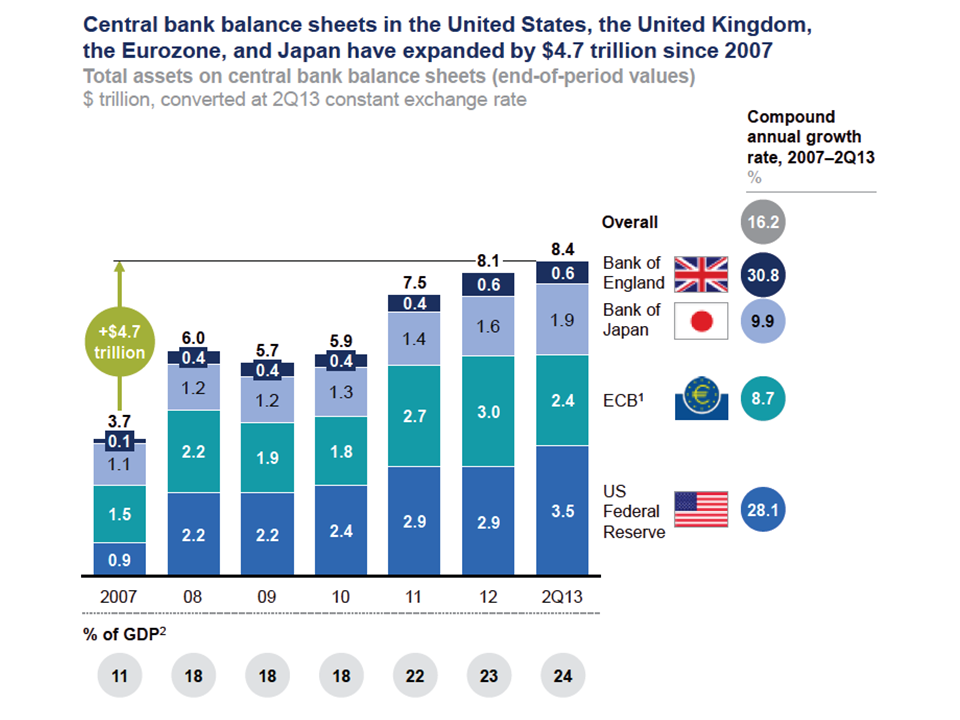

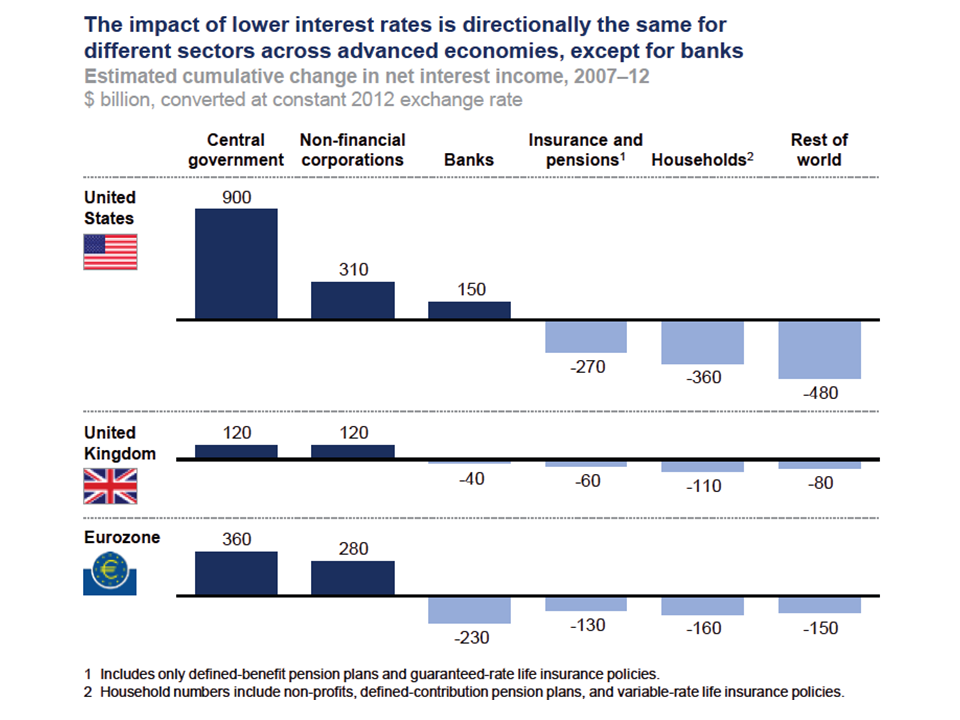

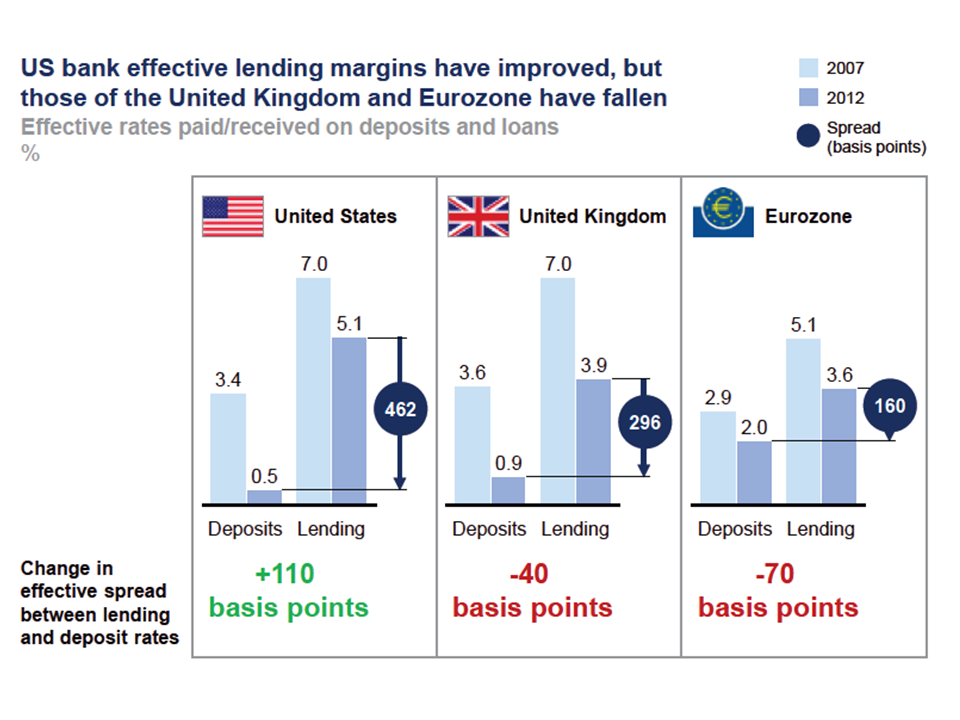

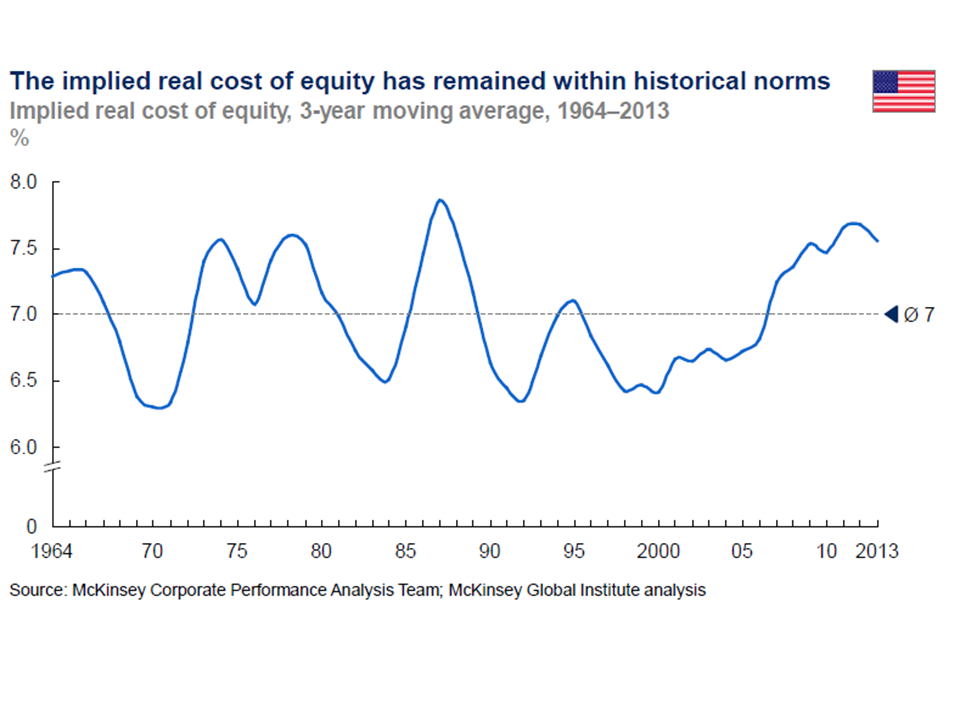

McKinsey had an interesting report on the impact of QE and ultra low interest rates. There was nothing particularly earth shattering about what they said but the report has some interesting graphs and commentary on the risks of the current global monetary policies.

The main points highlighted included:

Some interesting graphs from the report are reproduced below:

click to enlarge

click to enlarge

click to enlarge

click to enlarge

If the current low rate environment were to continue, McKinsey highlight European life insurers and banks as being under stress and believe that each will need to change their business models to survive. Defined-benefit pension schemes would be another area under continuing stress. A continuation of the search for yield for investors may lead to increased leverage (and we know how that ends!).

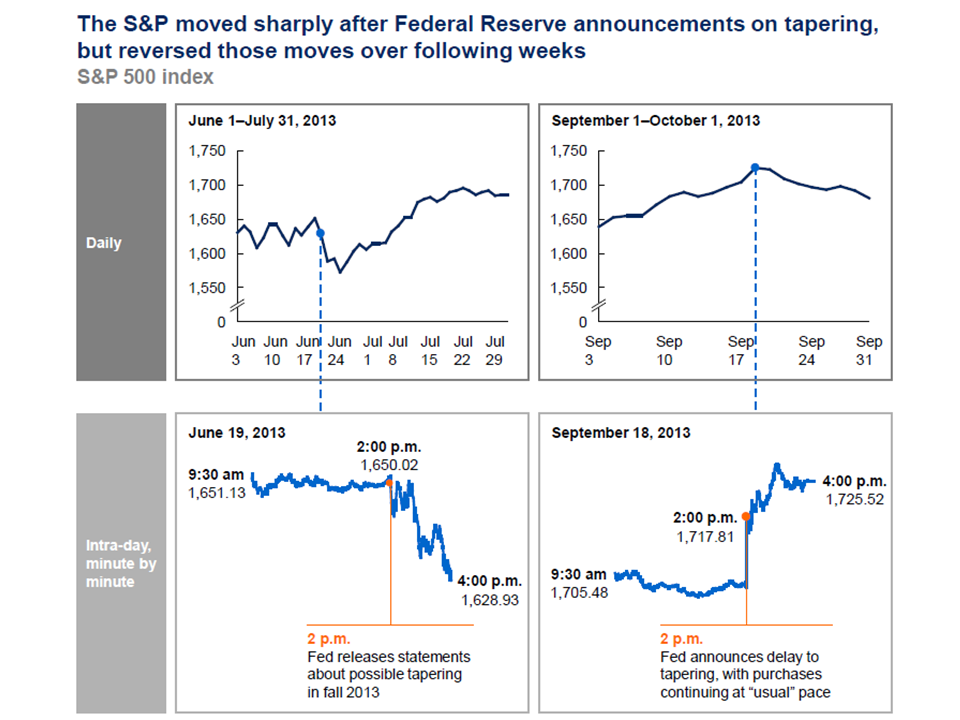

Increases in interest rate would have “important implications for different sectors in advanced economies and for the dynamics of the global capital market.” Not least, many working in investment firms and banks will never have experienced an era of increased rates in their careers to date! The first impact is likely to be an increase in volatility. Such volatility combined with market price reductions in interest sensitive assets may have an impact across the market and asset classes. McKinsey state that “a risk that volatility could prove to be a headwind for broader economic growth as households and corporations react to uncertainty by curtailing their spending on durable goods and capital investment.”

click to enlarge

The report highlight the average maturity on sovereign debt has lengthened with 5.4 years, 6.5 years, 6 years and 14.6 years for the US, Germany, Eurozone and the UK. Higher interest rates will obviously mean higher interest payments for governments. A 3% increase in US 10 year rates would mean $75 billion more in repayments or 23% higher than 2012. If, as seems likely, rates increase in the US first, the impact of capital outflows on other governments could be material, particularly in the Eurozone. A resulting Euro depreciation is highlighted (although I am not sure this would be too unwelcome currently in Europe).

click to enlarge

Mark to market losses on fixed income portfolios will follow. Some, such as many non-life insurers have purposely run a short asset:liability mismatch in anticipation of rates increasing. Others such as life insurers or banks may not be in such a fortunate position. Hopefully, the impact of improved economies which is assumed to have accommodated the rise in interest rates will solve all ills.

Posted in Economics, Equity Market

Tagged asset liability mismatch, average maturity on sovereign debt, capital outflows, central bank profits, corporate profits, defined-benefit pension schemes, Effective net interest margin, equity markets, Euro depreciation, fixed income returns, guaranteed returns, impact of QE, interest sensitive assets, Life insurance, lower debt service costs, market to market, McKinsey, ultra low interest rates, ultra-low rate monetary policies, uncertainty, volatility

![]() This blog represents my personal views and is not reflective of the views or opinions held by any company or employer I work for currently or have worked for in the past. The views expressed herein are based solely upon publicly available data. No views expressed herein should be taken as an endorsement to take any particular course of action in the markets. The basis of this blog is that different views should be expressed and readers make up their own minds on the what they believe and act accordingly.

This blog represents my personal views and is not reflective of the views or opinions held by any company or employer I work for currently or have worked for in the past. The views expressed herein are based solely upon publicly available data. No views expressed herein should be taken as an endorsement to take any particular course of action in the markets. The basis of this blog is that different views should be expressed and readers make up their own minds on the what they believe and act accordingly.