My bearishness on the reinsurance and specialty insurance sector is based upon my view of a lack of operating income upside due to the growing pricing pressures and poor investment income. I have posted many times (most recently here) on the book value multiple expansion that has driven valuations over the past few years. With operating income under pressure, further multiple expansion represents the only upside in valuations from here and that’s not a very attractive risk/reward profile in my view. So I am happy to go to the sidelines to observe from here.

So, what does this mean for my previously disclosed weak spot for Lancashire, one the richest valued names in the sector? Lancashire posted YE2013 results last week and disappointed the market on the size of its special dividend. As previously highlighted, its Cathedral acquisition marked a change in direction for Lancashire, one which has confused observers as to its future. During the conference call, in response to anxious analysts, management assured the market that M&A is behind it and that its remains a nimble lead specialist high risk/high return underwriter dedicated to maximising shareholder returns from a fixed capital base, despite the lower than expected final special dividend announced for 2013.

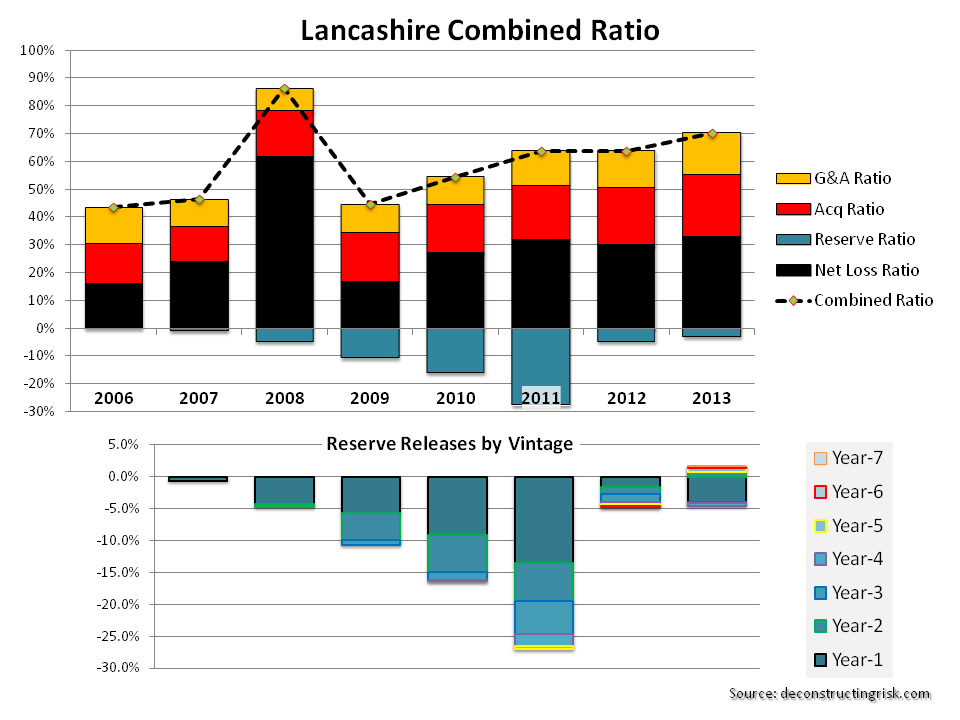

The graph below illustrates the past success of Lancashire. Writing large lead lines on property, energy, marine and aviation business has resulted in some astonishingly good underwriting returns for Lancashire in the past. The slowly increasing calendar year combined ratios for the past 5 years and the lack of meaningful reserve releases for the past two year (2013 even saw some reserve deterioration on old years) show the competitive pressures that have been building on Lancashire’s business model.

click to enlarge

The Cathedral acquisition offers Lancashire access to another block of specialist business (which does look stickier than some of Lancashire’s business, particularly on the property side). It also offers Lancashire access to Lloyds which could have some capital arbitrage advantages if Lancashire starts to write the energy and terrorism business through the Lloyds’ platform (as indicated by CEO Richard Brindle on the call). Including the impact of drastically reducing the property retrocession book for 2014, I estimate that the Cathedral deal will add approx 25% to GWP and NEP for 2014. Based upon indications during the call, I estimate that GWP breakdown for 2014 as per the graph below.

click to enlarge

One attractive feature of Lancashire is that it has gone from a net seller of retrocession to a net buyer. Management highlighted the purchase of an additional $100 million in aggregate protection. This is reflected in the January 1 PML figures. Although both Lancashire and Cathedral write over 40% of their business in Q1, I have taken the January 1 PML figures as a percentage of the average earned premium figures from the prior and current year in the exhibit below.

click to enlarge

The graphs above clearly show that Lancashire is derisking its portfolio compared to the higher risk profile of the past two years (notably in relation to Japan). This is a clever way to play the current market. Notwithstanding this de-risking, the portfolio remains a high risk one with significant natural catastrophic exposure.

It is hard to factor in the Cathedral results without more historical data than the quarterly 2013 figures provided in the recent supplement (another presentation does provide historical ultimate loss ratio figures, which have steadily decreased over time for the acquired portfolio) and lsome of the CFO comments on the call referring to attritional loss ratios & 2013 reserve releases. I estimate a 68% combined ratio in 2014, absent significant catastrophe losses, which means an increase in the 2013 underwriting profit of $170 million to $220 million. With other income, such as investment income and fee income from the sidecar, 2014 could offer a return of the higher special dividend.

So, do I make an exception for Lancashire? First, even though the share price hasn’t performed well and currently trades around Stg7.30, the stock remains highly valued around 180% tangible book. Second, pricing pressures mean that Lancashire will find it hard to make combined ratios for the combined entities significantly lower than the 70% achieved in 2013, in my view. So overall, although Lancashire is tempting (and will be more so if it falls further towards Stg7.00), my stance remains that the upside over the medium term does not compensate for the potential downside. Sometimes it is hard to remain disciplined……

Is it just my eyes or are those guys pretty quick with their reserve releases ? It looks like they build reserves just to release them (at least a significant part of it) the other year. But even without those releases the combined ratios are freakin’ good… On the other hand P/TB around 180% ??? I think there are some better plays out there… Even P/B is hovering around 155%. Maybe that’s why they call me scrooge…

Eddie

Yep, some amazing ratios in the early years. They have a very short tail book so the releases are event driven although it does look like they have been more aggressive of late. Business mix is also a factor.

This is not a ma & pa stock, big risks & big returns ~ dividend yields over yearly average share price of approx 6%, 17%, 9% & 20% from 2013 to 2010. Returned 190% of original capital raised in 2005! That’s why the big valuation. High-risk stuff buttery have delivered.

Not sure if it’s best days are behind it though

I see. From the outside it looks like they might be running some significant risks but got away with it so far. Think about writing deep otm puts. It works until it stops but when it stops you loose everything you collected so far plus a little extra. I don’t know the management so I could be way off but this is something I would check first. Their track record is not thaaaat looooong either…

Throw in the hefty price tag and it looks like you take a lot of risk (maybe those guys are good and can pull off that stunt for a few more years but you just don’t know) that provides a nice but not great return if it works out and I dunno what if it doesn’t. Not my cup of tea, I’m afraid.

Eddie

Eddie,

I think you have got the measure of Lancashire, they sure divide opinion, I know industry guys who think they are an accident waiting to happen and guys who think they are God’s gift!!!

I think my profitable past experiences with them may have corrupted my bias – I just can’t help but remember the girls I has a good time with though rose tinted glasses – a historic fault of mine!

Unfortunately these type of firms are too small for options (at least that I can find). Options on the big European reinsurers are silly expensive.

I have thought about ways of hedging firms with large CAT exposures (particularly those with peak US exposures) – CDS on debt or on CAT bonds, long/short pairs, ect but haven’t found anything that makes sense for a risk management point of view and/or from an economic point of view for a small time guy like me. Welcome any thoughts you may have….

M

So you are aware of your own cognitive biases. This is good news since this is the first step to avoid them.

I have seen similar stuff in hedge fund space. Of course all guys out there claim that they have the ultimate secret sauce. When you have a closer look it is usually Heinz ketchup in a new fancy looking bottle. Same story here: Lancashire is a black box, you don’t know precisely how they make money and you have to trust that management does the right thing. Since their track record is rather short this is a tricky exercise. I use Markel as a comparsion; these guys show you a track record of 20+ years with all ups and downs. This is something that gives me confidence.

We had the hedging topic a while ago already. The problem is that you don’t know exactly how they make money so you don’t know what to hedge. Not to mention basis risk and the fact that you don’t have access to a lot of instruments as retail investor. Even if you had access to everything out there the basis risk still could kill you.

Instead of buying a potentially crappy risk and trying to hedge the dangerous stuff I would rather look for a good risk to go along with. This approach is less accident-prone and thus less like to loose money. Which is the main risk I for myself care about… Making money by not loosing money… 🙂

Hope that helps.

Eddie

Thanks for the analysis.

Can you elaborate on your above comment that “I know industry guys who think they are an accident waiting to happen”? I’m keen to hear the specifics of the Lancashire bear case? Or is it perhaps a case of disbelief, without having done much fundamental work on the company, the people, the process, the culture etc. etc.?

I note that Odey Asset Management is short the stock — do you happen to know their thesis (I imagine they’ve done some fundamental work on the company)?

Thanks.

Thanks David for your comment.

First off, as I am sure you know, insurers always bitch about each other, especially in the London market.

LRE write big lines on high-risks on excess layers in a subscription market. You don’t average a 59% COR without taking a lot of risk. Some year they will be unlucky, maybe a big energy loss on top of a run of Nat cats. It’s part of the package.

To be fair to them, they don’t represent themselves as anything else!!

Also they have being derisking & doing some smart retro purchasing.

Hope that helps.

M

Thanks for replying.

I see. So you might say the negative case boils down to “base rate fallacy” — your average insurer doesn’t get a 59% combined ratio, so don’t assume any individual one will!

It’s a powerful argument for sure……especially as Lancashire is only in existence since late 2005. However, I think it’s important to take into account CEO Brindle’s very impressive 15-year pre-Lancashire Lloyd’s record (no year of loss).

Also — and this is company line to an extent — almost every insurer in the world is set up to grow, be it as a result of a corporate dictat, or the need to cover a minimum but high level of expenses, or simply down fiefdom-building on the part of underwriters or managers. As a result, risks that shouldn’t be written….are! Lancashire’s is set up to avoid these “institutional imperatives” (no silos, tight cost base). I believe it may be these factors that make it possible for Lancashire to do better than the “base rate”.

And it appears — from the outside at least — that this narrative is true. Lancashire exited D&F lines in 2011/12 and changed from being a writer to a buyer of commoditised retro, both times because of a deterioration in pricing / T&Cs. And, as you mentioned, they’ve been reducing their PMLs…..because they’re not being paid appropriately.

And I’m not so sure that Lancashire would “represent” themselves as being a high return / high risk company. Yes, they could get hit by a large individual event, but it would seem to me that this would a year of modest (or at least, containable) hit: 250-year estimated net loss of 25-30% of equity, 100-year event less than 20% of equity…..which would likely be offset by earnings elsewhere. I take some amount of comfort from Brindle’s Lloyd’s experience.

Well, that’s the bull argument. I’m keen to hear the negative story, so please pick apart my arguments! 🙂

Good points, David happy to debate.

I agree about Brindle, I’m a fan & I really like the business model of moving in and out of specialist sectors combined with strict capital management (no egomania driven empire building with fingers in every pie approach).

I would classify LRE as high risk though, they focus on a limited number of specialist lines and as such are not as diversified as many of their competitors. That’s not to say the portfolio is unbalanced, clearly Brindle has shown how he can balance risks within a portfolio but it is not as diversified as many & therefore is, imo, higher risk.

So here’s the bear arguments – My concern is really about structural changes in the market. This underwriting cycle will be very different that previous ones (each cycle has its own forces), risk management is at a level not seen before, discipline is good (believe me compared to the late 1990s its amazing)

The forces gathering are new capacity & buyer changes. The ILS market are moving into specialty short-tail sectors like marine/energy (e.g. funds like CATCo who just announced they are hiring traditional underwriters illustrates the point – plus the fact that CATCO had a loss from Costa Cordia, unusual for a propCAT book!!), hedge fund backed re/insurers who can operate at CORs above 100% (see Third Point results), and global insurers who have a full suite of products across many jurisdictions (e.g. firms like Allianz/Zurich can offer energy firms bundles of insurance cover from D&O to pollution).

All of these forces make operating as a small focussed specialist all the harder. Not impossible & I think buying Cathedral for such a high multiple to get its more sticky business means that LRE know they need to change.

With all that said, I still think Brindle can do it although I think expectations on underwriting returns for the next phase of the cycle need to be adjusted downward & that get’s to the core of the risk/reward profile of LRE.

For me, as a small time investor, the risk/reward profile is at the extreme of my risk appetite (then again, after such a good 2013, my risk appetite is moving to mainly cash on the sidelines!!).

Hope some of that makes sense.

M

Thank you M, these are great comments. I suppose none of this is provable either way, but it’s surely great to discuss.

You are most certainly right that there are new structural changes to consider.

The traditional market claims that the ILS market can augment — but cannot replace it. By definition, ILS’ are structured and so are much less flexible than traditional underwriters – clients may want multi-year deals with reinstatements, across multiple perils, for example. I understand this is far from easy to replicate for alternatives, primarily because of the fully-collateralised nature of the products. Also, it’s unclear how fairly alternative insurers will deal with future claims? The more specialised and unique the insurance contract, the more nuanced is the claims situation and requires the underwriter handle things with “sensitivity”. [On a recent conference call, Brindle talked about about claims disputes and litigation in the third-party capital space.]

One could also make the argument that the low interest rate environment has encouraged an abundance of capital to seek meagre (or worse) returns — in effect, pulling forward supply of capital to the point where we are closer to the end game than we might think. [Maybe that’s just wishful thinking….].

And besides, Lancashire is looking to capitalise on third party money, which they estimate will add 2-3% to group RoE (my hunch is they’re being conservative, but then again I am bullish on the company).

The Cathedral acquisition could be considered expensive (though the headline P/B multiple paid was higher than actual, after adjustments). Moreover, Cathedral’s Lloyd’s platform will serve to enhance the core Lancashire business, through capital efficiency and a broader global reach. So there are genuine synergies (I hate that word!) here — and who would know better about exploiting this than Brindle.

Interesting comment about Third Point’s ability to underwrite at a loss, presumably because Dan Loeb feels he’ll deliver great investment returns. Greenlight Re is in the same boat and Pine River is rumoured to be doing the same. However, I’m not sure just how many of these superstar investors are out there, so I would think this is a far lesser risk than the alternative capital risk discussed above.

I am not familiar with buyers changes in specialty lines through bundling. Can we be certain that clients are getting like-for-like products through the bundle? I would hazard a guess that in most walks of life, specialists just do things better (typically charging a higher price), appealing to more discerning clients. Would that be a fair comment in the specialist insurance world?

At the end of the day, I don’t think our opinions are too far removed. You see some dark clouds which makes you reluctant to invest at the current 1.5x P/B. I’m invested but am hopeful I’ll get the chance to buy more at much lower prices (as a result of large losses or a general market sell-off!).

Appreciate there’s a lot in this, but would be delighted with whatever feedback / push-back you can give.

David

I think you have hit the nail on the head, we are of similar views here & definitely if price continues to drop I will be very tempted. I just don’t see any urgent need to get in, upside here to me is purely multiple driven by the sector. I’d like to see a quarter or two of results to see how the merged entity looks, particularly the reserve releases from Cathedral going forward (the CFO say $20M for 2013 but didn’t, as far as I could here, give any 201 indication).

It will be interesting to watch how this phase of the cycle develops.

M

Thanks. If you’ve any further thoughts, I’d be delighted to read them.