The last time I posted on Paddy Power Betfair (PPB.L), I highlighted it was looking pricey in the mid-to high 90s. It has since traded down to the eighties and recently dipped below £83 after the full year results. Although it has now quickly recovered up around £88, the initial disappointment over the online revenue in Q4 sent the stock down 6%.

The graph below shows quarterly revenues, which met expectations largely due to the favourable A$ rate with Australia revenue up 34% in sterling but only 18% in the underlying currency. Management make a point of stating that “approximately 70% of our profits are sterling denominated, and accordingly, we are not exposed to FX translation fluctuation”. Events such as the summer 2016 Euros contribute to the revenue spike in Q2 2016.

click to enlarge

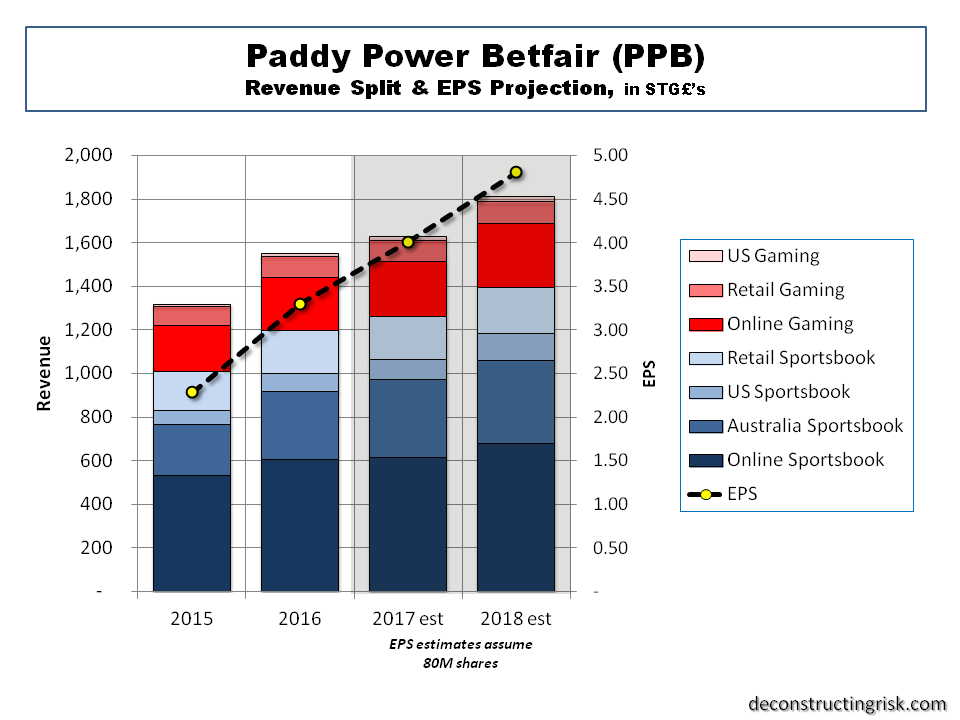

They exceeded my expectations on the bottom line with an operating profit of £182 million for H2 over my expectation of £160 million, with the merger expense and intangible write-off impacts of £300 million for the full year stripped out. The EPS of £3.30 for 2016 on average 80 million shares was impressive. I messed up on the average share count (again!) in my previous EPS estimate.

PPB stated that they “expect to complete the integration of our European online platforms by the end of 2017” and “until then, new product releases on the Paddy Power brand will be relatively limited, but on completion customers will see immediate benefits”. Despite their market beating margins on their dominant online segment, they caution that “a lot of the sportsbook operators acknowledge that gaming got harder in the second half of last year” and they always emphasis that they operate in a very very competitive market. It looks to me like PPB management are trying to carefully manage expectations for 2017 and are likely nervous that large competitors like William Hill and Ladbrokes could possibly recover from recent online slumps and (just maybe) finally get their act together online.

There is an ongoing regulatory headwind in this business and 2016 bought items such as the online gaming point of consumption tax, the statutory Horserace Betting Levy, and the UK Competition and Markets Authority (CMA) investigation into UK online gambling (update due in April) to the fore. In addition, South Australia announced a 15% consumption tax effective from July 2017. The UK Government’s Review of Gaming Machines is a much bigger deal for PPB’s larger competitors as it only makes up 6% of their revenue.

PPB have substantially completed the integration of risk and trading functions which means that Paddy Power proprietary pricing and risk management tools are now used for over 85% of the bets on the Betfair sportsbook across 19 sports. They stated that “operating two individual brands on an integrated shared function is also proving to be beneficial for efficiency” and that the “pooling of analytics data has improved our econometric modelling, giving us greater insight into the effectiveness of marketing activity and leading to improved optimisation of spend”. These are critical factors in why PPB is differentiating itself operationally from its peers and are important to the success of the business model envisaged by the merger.

So, although I have likely got the share count wrong again (I am assuming an average of 85 million this time across 2017 and 2018), my new projections are below. I estimate growth of 5% and 11% for revenue in 2017 and 2018 respectively and EPS growth of 14% and 20% respectively. I factored in a degree of topline and bottom line upside in 2018 from the soccer world cup in Russia (assuming politics hasn’t messed up the world order by then!). That represents a PE multiple of 19.4 on an 2018 EPS estimate at a share price of £88 (2017 PE of 23.3). Not bargain basement cheap but not crazy mad either. With a targeted payout rate of 50%, my estimates could mean a dividend yield of 2% and 3.5% for 2017 and 2018 (again at a £88 share price).

click to enlarge

That looks like a better dynamic that the one at a share price in the mid to high 90’s, as per my post in August. If only I wasn’t so negative about overall valuations across the market, I would have added to my PPB position on the dip after the results last week. [Customary caution: PPB is not for the faint hearted, it is the gambling business after all!]. My instinct tells me markets will be bumpy in the coming months, valuation wise (e.g. rising interest rates, politics!). That may prove an opportune time to get more of PPB at a good price. After all, the game of speculation it is all about getting the best odds!