This week has been a volatile one on the markets with much of the week’s losses being regained after a “goldilocks” jobs number on Friday. Janet Yellen chipped in with the statement that “equity market values at this point generally are quite high” which resulted in the debates about market valuation been rehashed on the airwaves through the week.

My thoughts on the arguments were last aired in this post. I believe there is merit to the arguments that historical data needs to be normalized to take into account changes in business models within the S&P500 and the impact of changes in profit margins. Yield hungry investors and the lack of alternatives remain strong supports to the market, particularly given the current thinking on when US interest rate rises will begin. Adjustments on historical data such as those proposed by Philosophical Economics in this post make sense to me (although it’s noteworthy he concludes that the market is overvalued despite such adjustments).

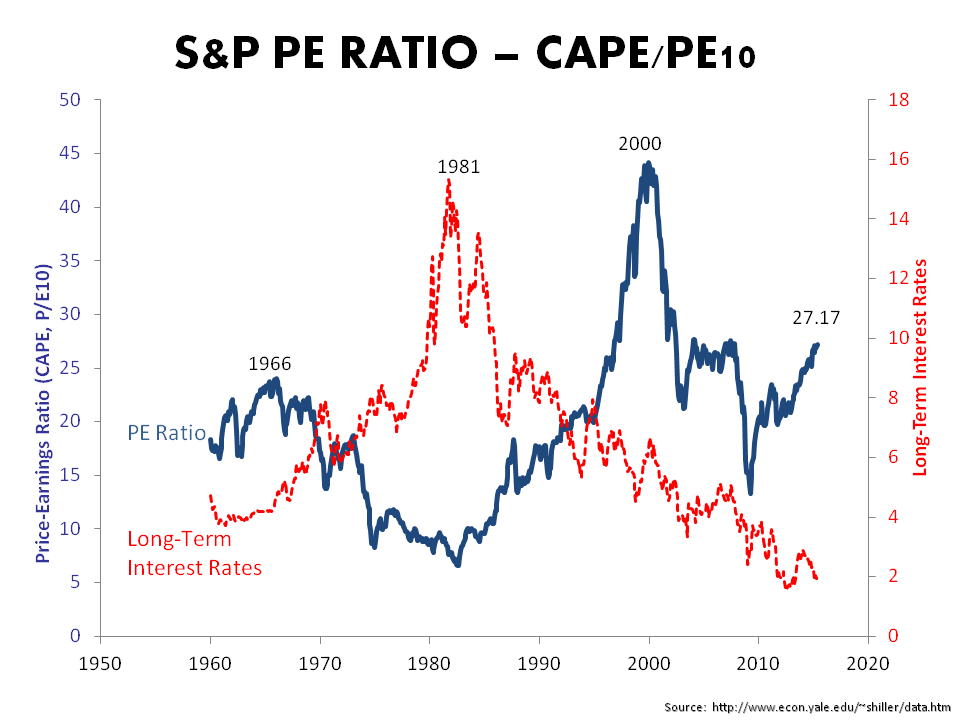

Shiller’s latest PE10 metric (adjusted for inflation by the CPI) is currently over 27, about 38% above the average since 1960, as per the graph below.

click to enlarge

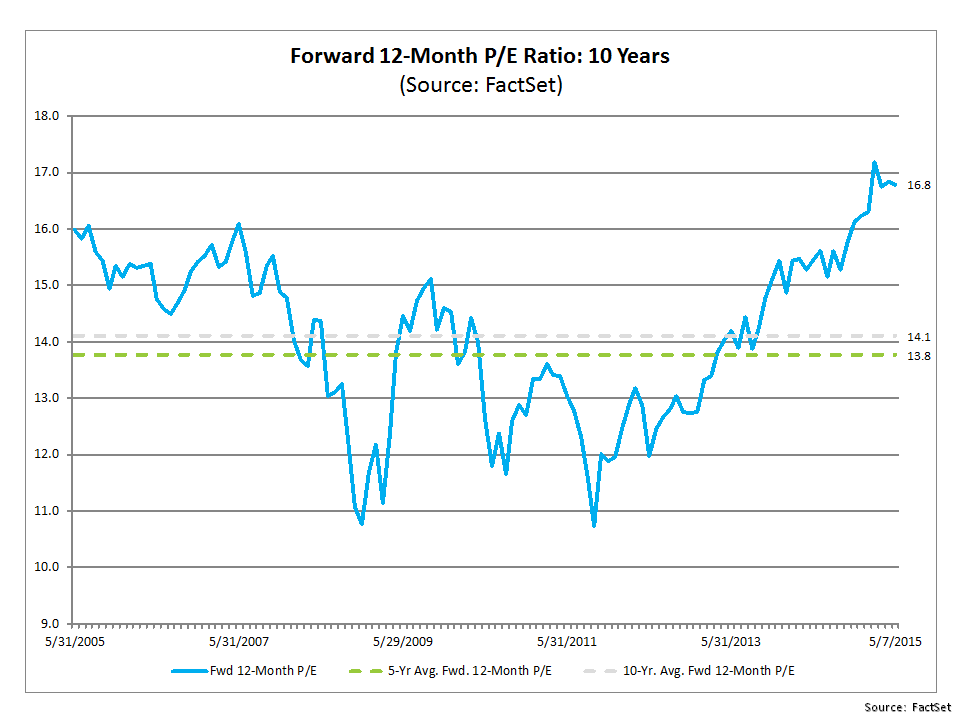

I tend to put a lot of stock in the forward PE ratio due to the importance of projected EPS over the next 12 months in this market’s sentiment. Yardeni have some interesting statistics on forward PE metrics by sector in their recent report. Factset also have an interesting report and the graph below from it shows the S&P500 trading just below a 17 multiple.

click to enlarge

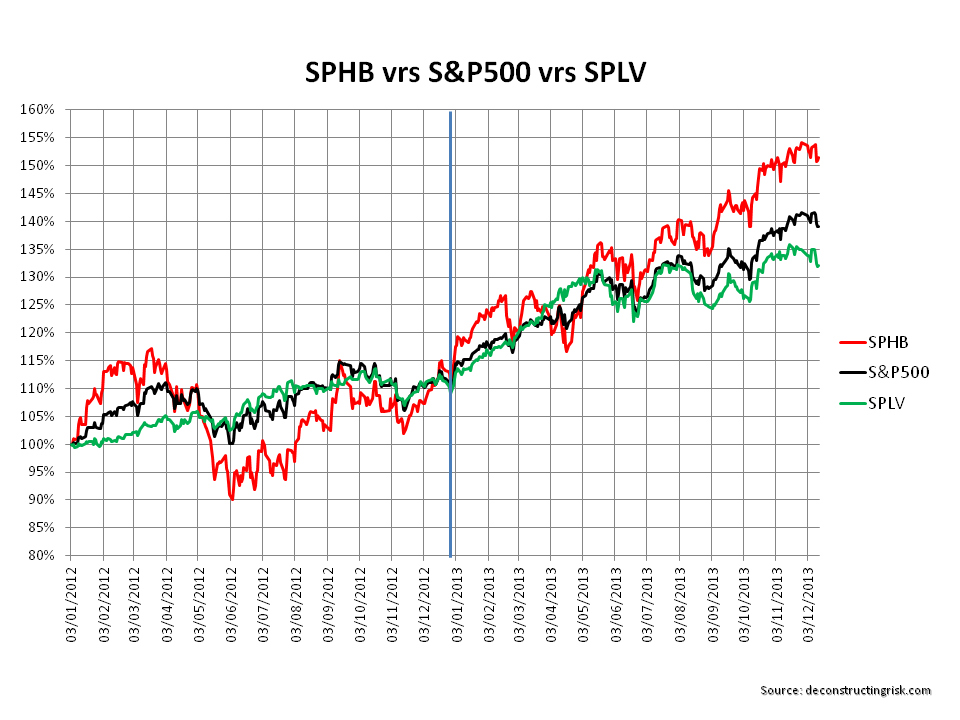

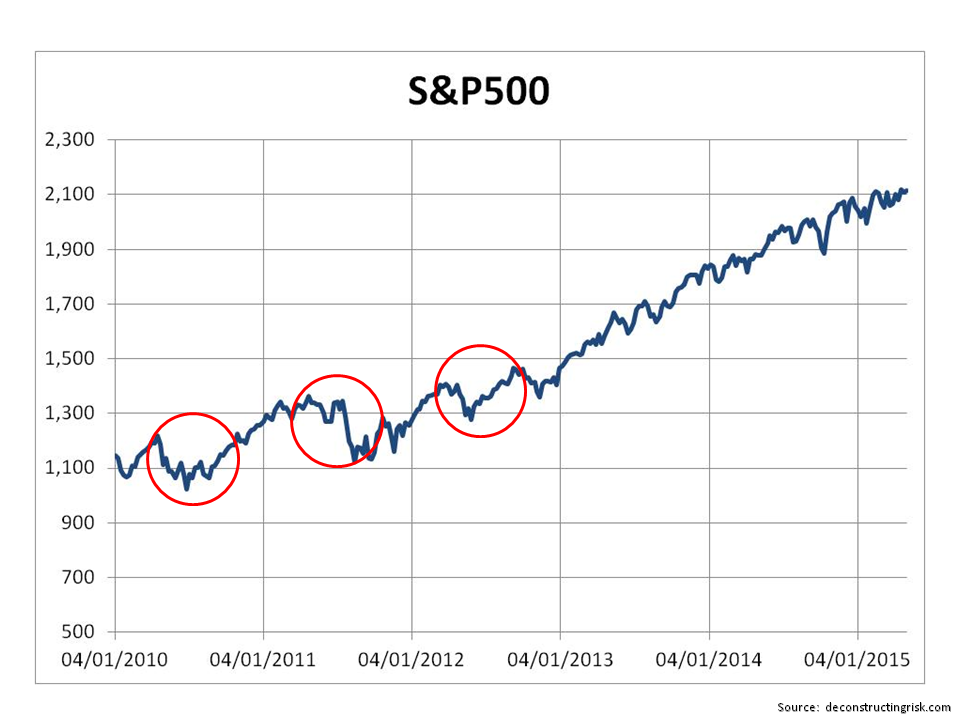

Recently I have become more cautious and the past week’s volatility has caused me to again review my portfolio with a ruthless eye on cutting those positions where my conviction against current valuation is weakest. Making investment decisions based upon what month it is can be justifiably called asinine and the graph below shows that the adage about going away in May hasn’t been a profitable move in recent years.

click to enlarge

However my bearishness is not based upon the calendar month; it’s about valuation and the nervousness I see in the market. To paraphrase a far wiser man than me, all I bring to the table is over 20 years of mistakes. Right now, I would far rather make the mistake of over-caution than passivity.